The Virtue of Patience

13 February 2023

The key development over the last couple of weeks has been a shift upwards in traders’ interest rate expectations.

4 min read

13 Feb 2023

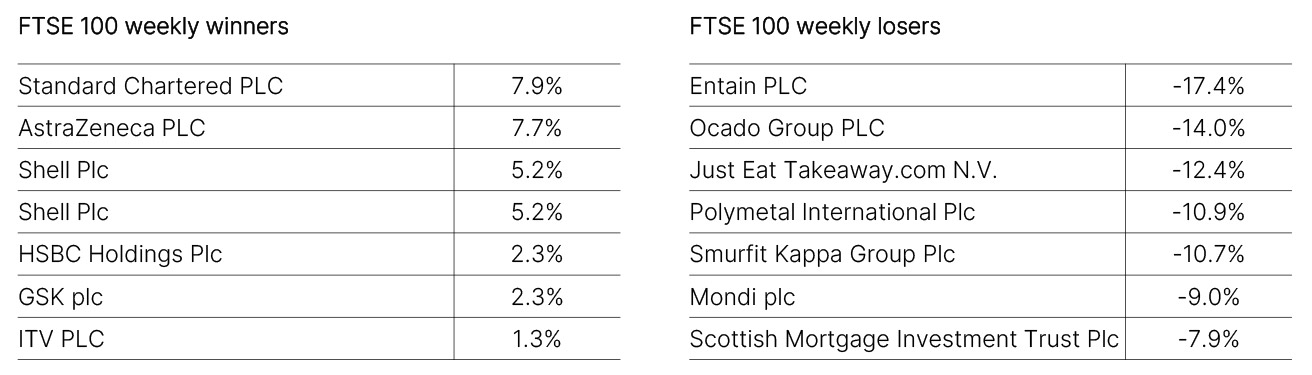

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

The UK economy contracted by 0.5% month-on-month in December 2022, weaker than consensus estimates of a 0.3% drop. Services fell by 0.8% on the month, driven mainly by declines in the health and education sectors, the former influenced by industrial action. Industrial production expanded by 0.3%, helped by a weather-driven surge in utility output. Manufacturing and Construction output was flat on the month. There was a modest upward revision to past data. This meant that GDP remained flat quarter-on-quarter, leaving the economy 0.8% smaller than its pre-pandemic levels. Household consumption eked out a 0.1% gain in real terms. Things would undoubtedly have been worse without the support of the Energy Price Guarantee. Thus the economy avoided a technical recession over the second half of the year (GDP in Q3 was revised up a shade to show a decline of 0.2% on the quarter) by a mere £77m. But there is more pressure to come, especially from the upwards repricing of maturing fixed-rate mortgages. Investec Bank forecasts UK GDP to shrink by 1% in 2023 vs 2022.

There was remarkably little economic data to move markets last week. The latest University of Michigan Sentiment Survey held no demons. There was a small uplift to current conditions while expectations worsened marginally. The standout was a jump in one-year ahead inflation expectations from 3.9% to 4.2%, but given that the five to ten-year figure stayed at 2.9%, there was limited reaction. The biggest noise came from speakers from the Federal Reserve, who, on balance, encouraged investors to price in a “higher for longer” interest rate environment.

There was equally thin gruel in Europe. Sentiment continues to recover from the trough, with the Sentix Investor Confidence Index echoing other surveys. It rose from -17.5 to -8.0 in February vs an expected -13.5. German inflation readings in January were mixed. The headline figure came in at 8.7%, better than the expected 8.9% but still above December’s 8.6%.

China’s total social financing came in at CNY5.98tn in January 2023, up sharply from CNY1.306tn in December and beating consensus expectations of CNY5.4tn. However, China’s credit impulse, the year-on-year change in new borrowing and a key driver of China’s manufacturing PMI new orders index, was little changed at a nine-month low of -3.6%, versus the recent high of +1.3% in October. China’s M1 money supply growth accelerated from 3.7% year-on-year in December to 6.7% in January, the highest level since March 2021. New loans came in at CNY4.9tn, up from CNY1.4tn in December, beating consensus expectations. This led loan growth to edge up to 11.3% year-on-year from 11.1% in December. This should support recovery. CPI inflation picked up to 2.1% year-on-year in January at the headline level, up from 1.8% in December, in line with expectations. China’s Core inflation edged up to 1% year-on-year, from 0.7% previously. PPI inflation fell further into negative territory, down from -0.7% year-on-year in December to -0.8% in January, below consensus expectations at -0.5%. There might be more upward pressure on inflation from a consumption recovery, but benign producer prices should stop it getting out of control.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.