Unresolved Issues

25 January 2021

What are the continuing effects of the forces that have been driving markets for the past twelve months?

5 min read

25 Jan 2021

Inflation will be one of the most closely watched series of data this year, as everyone tries to second guess if or when central banks will tighten policy. December’s CPI data show that headline CPI remains muted at 0.6% y/y, but it’s definitely on the rise. The less volatile Core CPI also ticked up from 1.1% to 1.4%. Don’t be surprised to see a reading well over 2% by mid-year on a headline basis, although we do not expect the Bank of England to react. Meanwhile the government’s finances continue to deteriorate as it responds to Covid while receiving less tax. Borrowing was £34.1bn in December, with the cumulative deficit for the fiscal year rising to £270.8bn (vs just £58.1bn a year earlier). Even so, we do not expect a reversion to austerity any time soon.

After a few weeks of lacklustre data, there was a solid rebound last week. Series that beat expectations included PMI readings, Existing Home Sales, Weekly Jobless Claims, Housing Starts, Building Permits and the Philadelphia Fed Business Outlook survey. The distribution of the latest round of stimulus cheques should also help to shore up demand in January.

The ECB left policy unchanged at its latest meeting. There remains plenty of capacity to continue asset purchases, which are currently running at €20bn per month. There was no change to its forecast of 3.9% Eurozone GDP growth this year, which is based upon lockdowns remaining widely in place during Q1 and a gradual vaccine rollout. We continue to believe that the ECB will flex policy as required, and that policy will not be tightened for a few years yet.

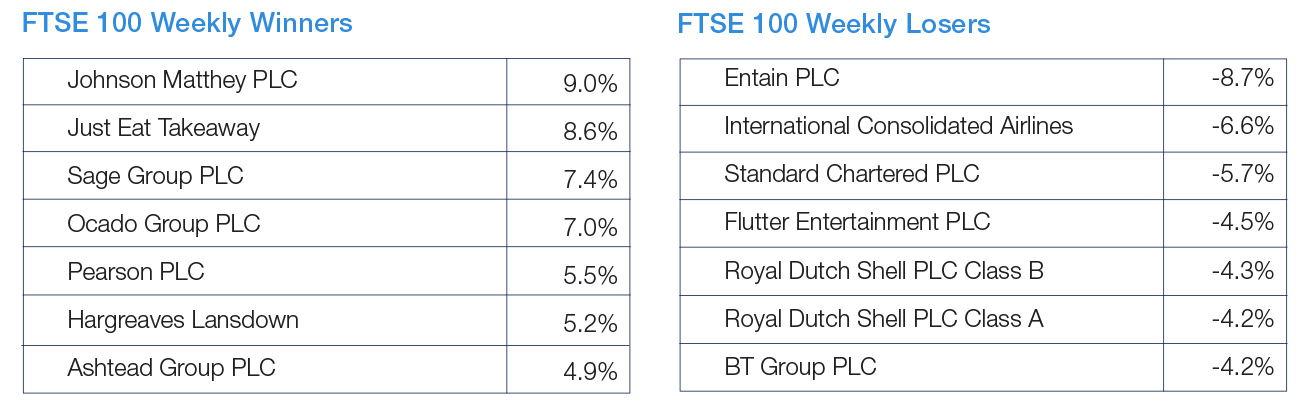

Source: FactSet

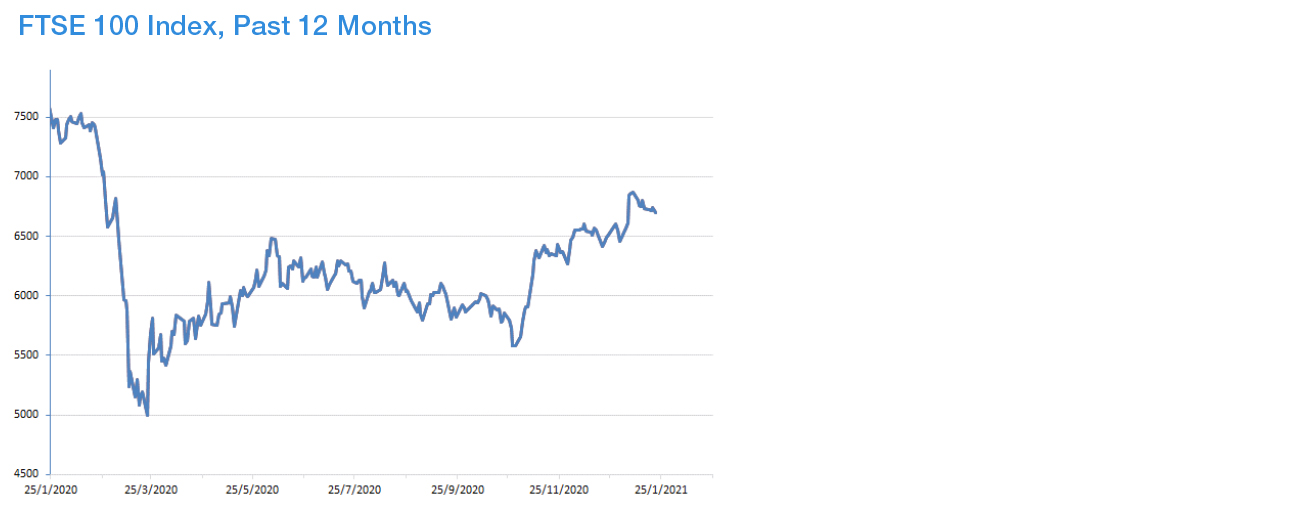

Source: FactSet