Wall St vs Main St

13 July 2020

Why is there such a disconnect between what is going on in financial markets and the headlines about the real economy?

5 min read

13 Jul 2020

What little data there was last week continued to point towards recovery, even if activity levels are well below previous peaks. The Markit/CIPS Construction PMI data outstripped the forecast of 46 and jumped straight to 55.3 (from 28.9). The caveat, as ever, is that these series are going to look very odd given the extent of the downturn we have seen. Over 50 will not exactly represent boom times for a while. House Prices, as measured by the RICS survey, are not booming either, but their survey balance recovered from -32% to -15%. Highlight of the week was Chancellor Rishi Sunak’s latest handouts, although it must be remembered that this is driven by necessity, not generosity.

Americans have developed a new savings habit. Outstanding Consumer Credit fell again in June, this time by $18.3bn, although that was far short of the $70.2bn reduction in May. A return to increased credit might signal the return to more normal times. However, another 1.31m filed for unemployment benefits last week, even if, on balance, the number of Continuing Claims fell from 18.8m to 18.1m. There must be a revolving door at the Job Centre.

A quiet data week here too, but May’s 17.8% jump in Retail Sales bettered the expected 15%. Although with moves as big as this it is impossible to expect forecasts to be accurate.

M2 Money Supply is growing by 11.1% y/y, the highest figure since 2016 when the last big stimulus was being applied to the economy. Local investors, encouraged by the government, have been piling into the stock market in anticipation of accelerating growth.

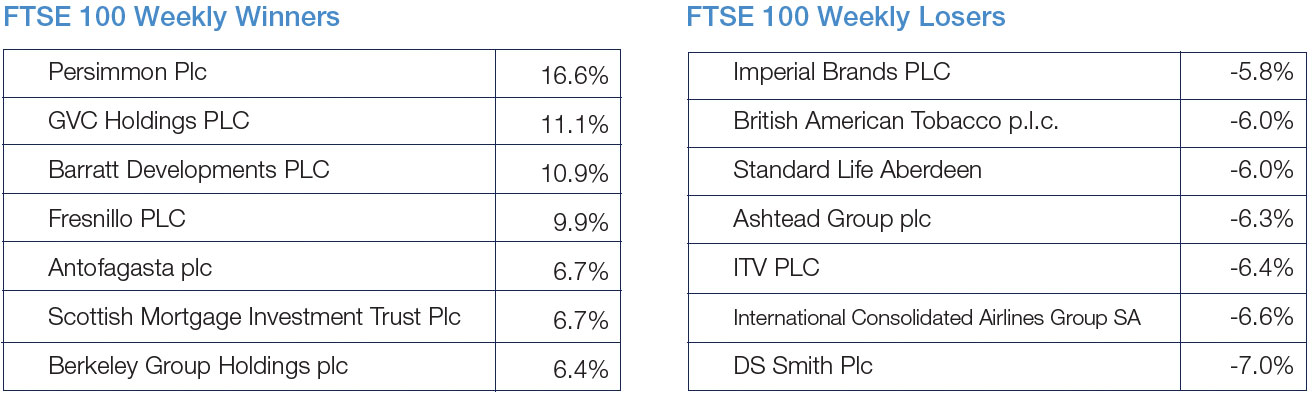

Source: FactSet

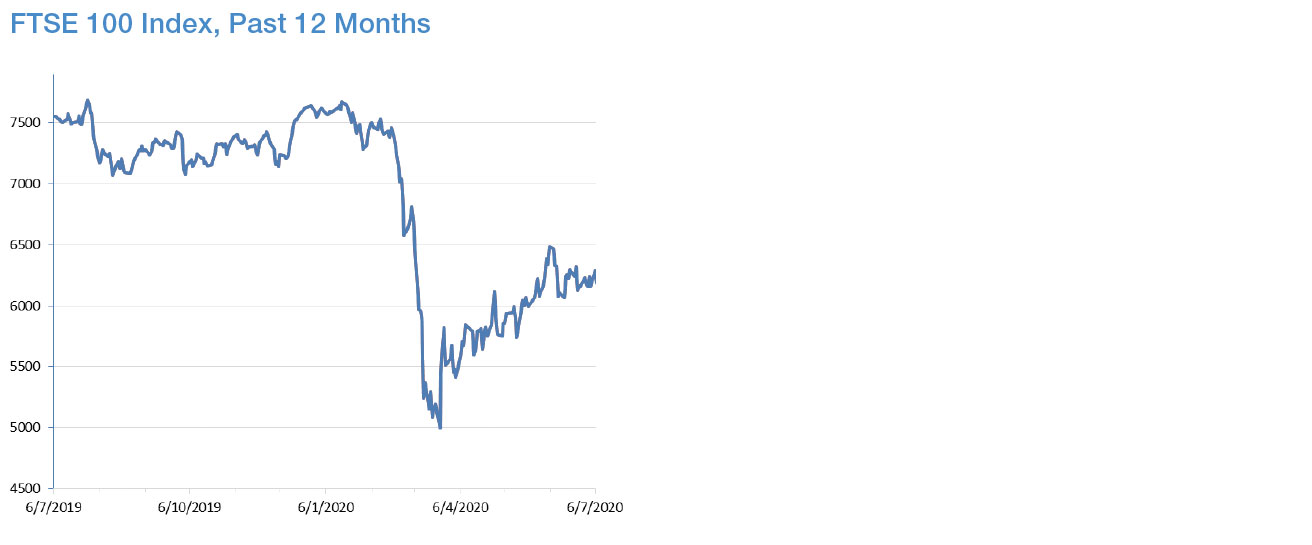

Source: FactSet