Fear and Greed

02 March 2020

Markets last week went from one extreme to another, as equities bounce back in response to ‘whatever it takes’ policy promises.

5 min read

02 Mar 2020

The trouble with most economic data now is that it is not timely, and fails to capture the COVID-19 effect. Thus February Consumer Confidence (-7 vs -9) and January Mortgage Approvals (70.9k vs 67.9k) both reflect the heady days of optimism following the election. Even the latest Markit PMI Manufacturing reading (51.7 vs 51.9) hardly wobbled. Let’s see what the next few weeks bring.

A similar story here, with, for example, Housing data, continuing to show a robust market. One feature was the still very low level of inflation, just 1.63% as measured by the Core PCE. The market is now pricing in two quarter point interest rate cuts before the summer in response to the virus.

The latest Manufacturing PMI reading ticked up from 49.1 to 49.2. Hardly a boom, but another sign that growth trends were definitely turning for the better before the outbreak, which is a source of much-needed comfort.

We saw the first real sign of the economic damage inflicted by COVID-19 in the PMI data released over the weekend, with the Services number plummeting (and for once the word is appropriate!) from 54.1 to 29.6. Manufacturing also dropped from 51.1 to 40.3. Hardly surprising, all things considered, and suggesting close to zero growth in China in the first quarter.

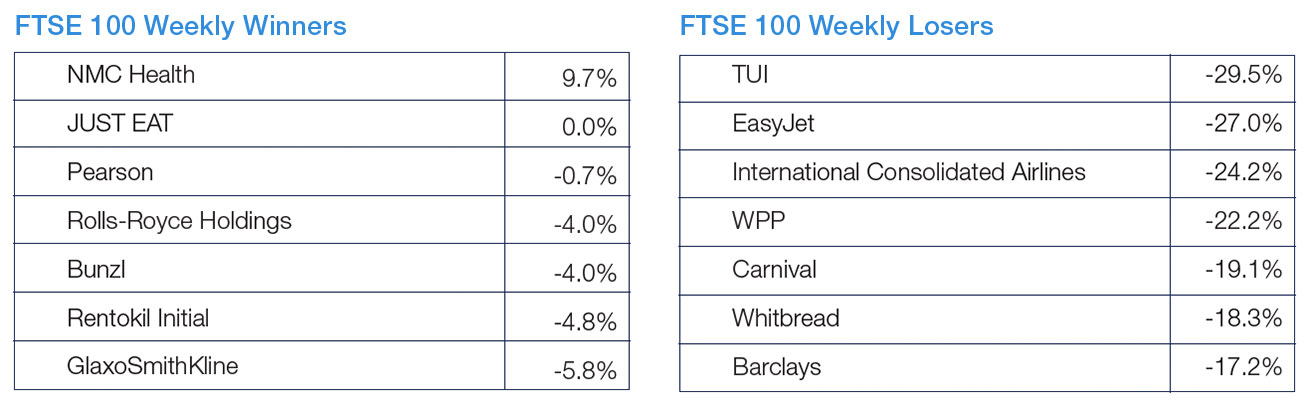

Source: FactSet

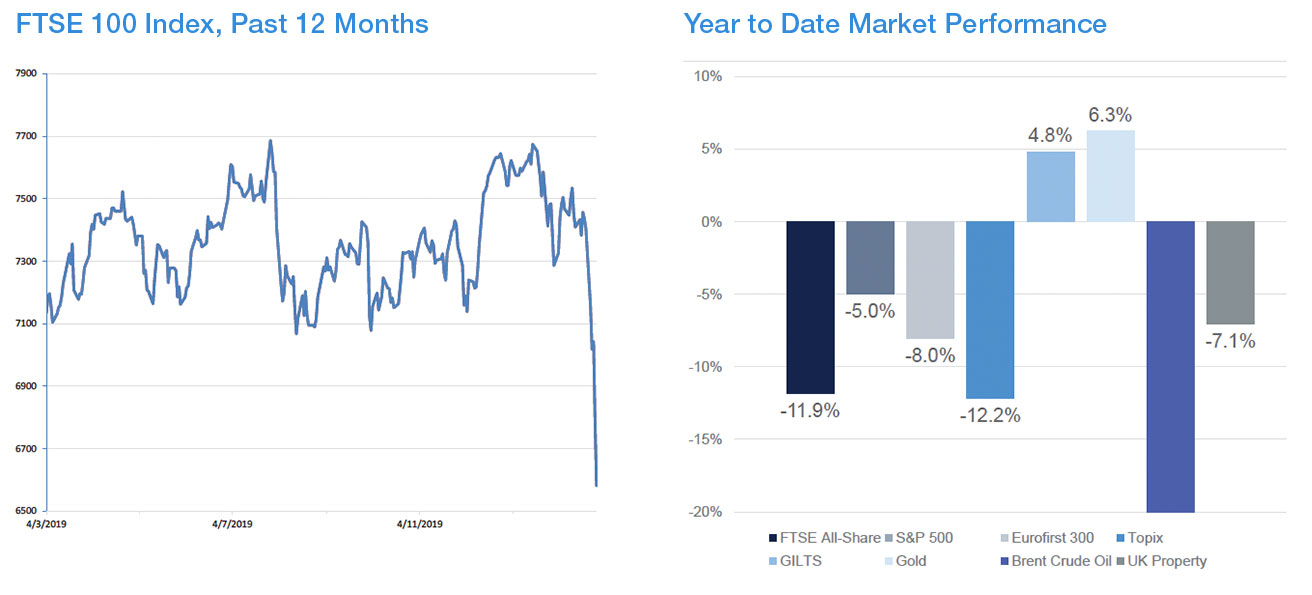

Source: FactSet