Immune Systems

09 March 2020

The S&P Index could soon fall 20%, faster than the current record which could have some predicting crashes like the end of the roaring twenties.

5 min read

09 Mar 2020

In this section we normally review some of the most important economic data from the previous week. However, in current circumstances, it seems pointless to stick to the usual regime. Most data that is coming out now will not reflect the developing economic environment. We have seen some indications of stress from China, which is where the coronavirus outbreak started. The Caixin Composite PMI Index plummeted from 51.9 to 27.5, but it’s hard to know exactly what that means for eventual GDP growth. A reading of 27.5 is, as statisticians might say, “out of sample”. Exports from China also collapsed in February – not surprising with very little moving in the country.

The Caixin Composite PMI Index plummeted from 51.9 to 27.5.

We have also seen hints of trouble in some of the European surveys, mainly alluding to lengthening supply chains (in terms of days to delivery). But no real sign of demand problems reported yet. That won’t last. Meanwhile in the US the latest Payroll data, with 273,000 new jobs added in February, pointed to what was a very resilient economy. At least that might provide some sort of cushion against the coming downdraft. Much better to be facing COVID-19 related constraints from a position of relative strength.

Hard economic data is lagging by its nature, and so the next weeks will be difficult ones in which to gauge real activity. Purchasing Manager Indiceswill be helpful to some degree, but more for direction than magnitude, one feels. The questions they ask tend to be blunt; eg: “ are you selling more or fewer widgets than last month?” Companies are compelled by law to disclose material differences between expectation and reality. We can expect a rash of corporate trading updates that will possibly provide better information in the short term.

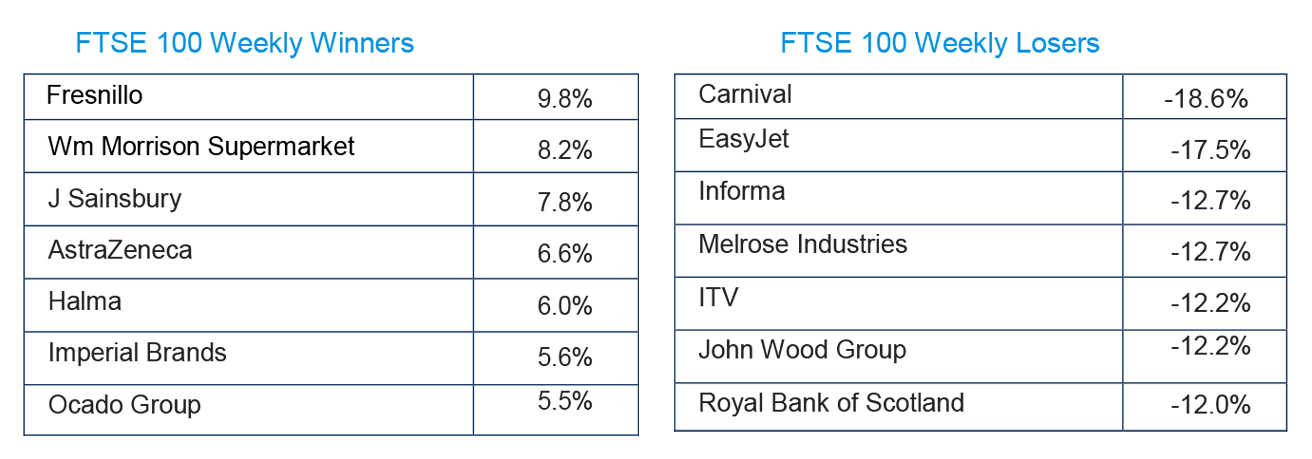

Source: FactSet

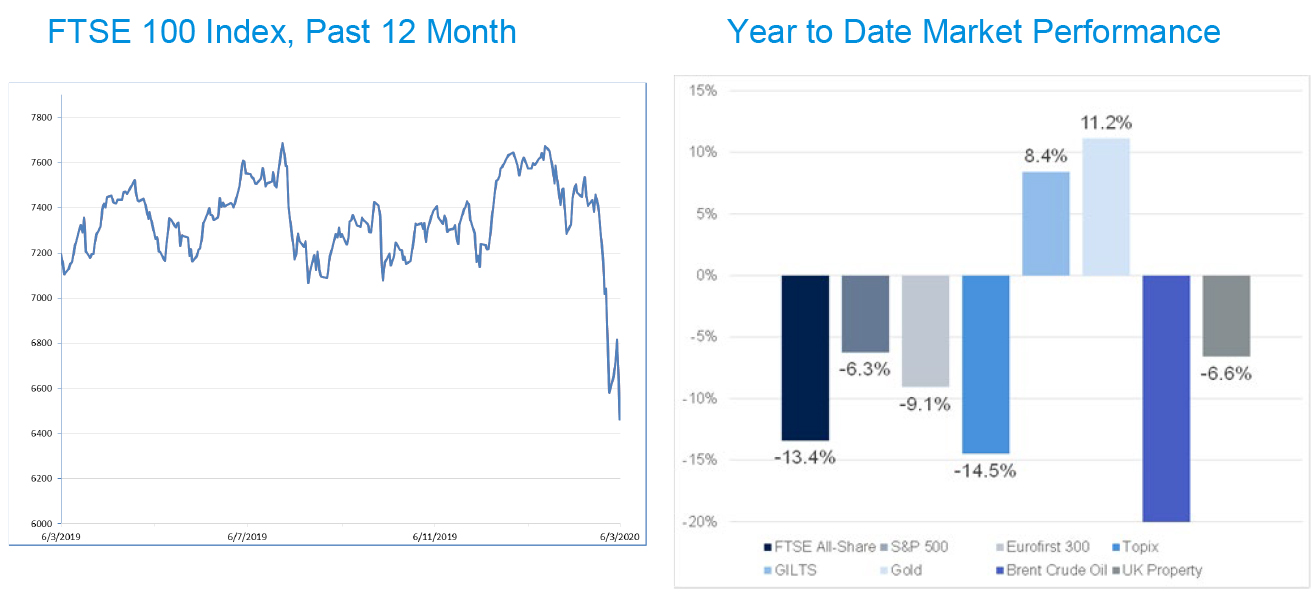

Source: FactSet