More Of The Same

10 February 2020

An air of repetition this week as two topics continue to dominate, the US Presidential election and Coronavirus.

6 min read

10 Feb 2020

Survey data continues to show evidence of a post-election “Boris Bounce”, although with the caveat that the PM’s more aggressive recent stance towards trade negotiations with the EU might not yet have been reflected. The same goes for coronavirus concerns. Still, PMI data was up across the board in January. The Manufacturing reading rose from 49.8 to 50.0, Construction from 44.4 to 48.4, and Services from 52.9 to 53.9. This left the Composite reading up at 53.3 from 52.4, the highest reading since September 2018.

PMIs were better in the US as well, but the star of the show was the Non-Farm Payroll number, with jobs growth of 225,000 against an expected 165,000, and marginal positive revisions to earlier months. The Unemployment rate did creep up from 3.5% to 3.6%, but that was because more workers have been tempted back into the market, with the Participation Rate edging up from 63.2% to 63.4%, the highest rate since 2013. Wage growth edged up too, from 2.9% to 3.1%, leaving consumers is decent health.

The much vaunted economic recovery pencilled in for 2020 was not in evidence in December, as Factory Orders fell 2.1% m/m and 8.7% y/y. No doubt the Auto industry is still struggling. It didn’t stop the country registering a huge €29.4bn Current Account surplus in December, possibly owing to lower Imports as a result of fewer components being required.

Pretty much any piece of economic data from China should be taken with a pinch of salt now until the effects of the coronavirus work their way through the system. Consolingly, Foreign Reserves remain rock solid at $3.115 trillion, a level at which they have been very (suspiciously?) stable for three years now. No sign of capital flight from China.

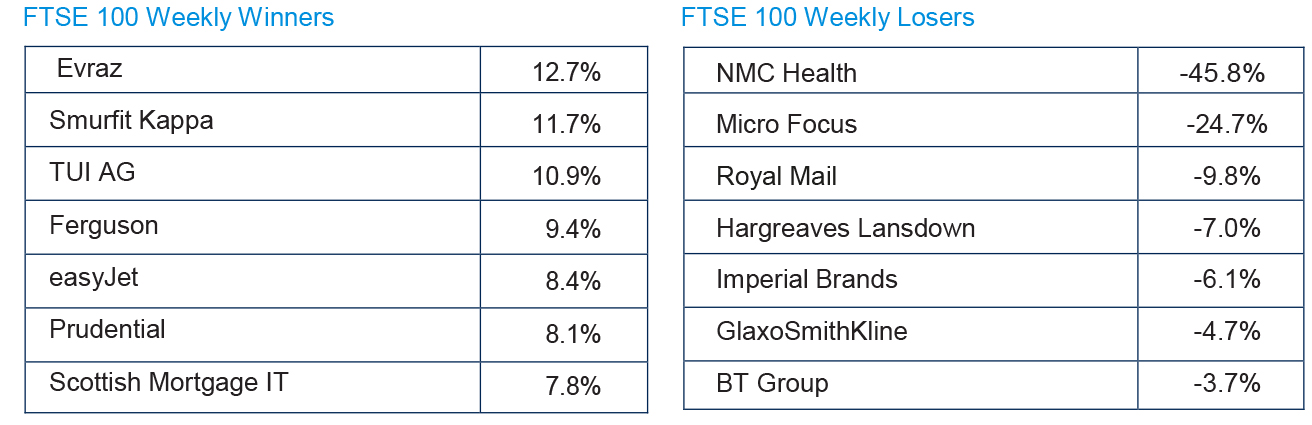

Source: FactSet

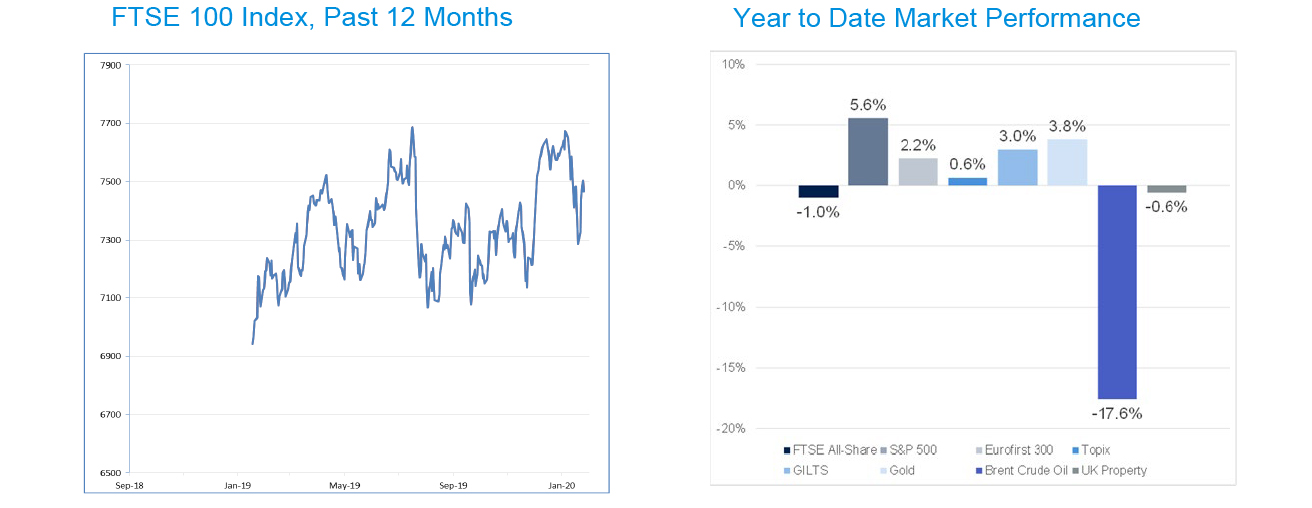

Source: FactSet