The Best Laid Plans…

24 February 2020

A simple entrance to 2020, led by easing trade tensions, has certainly been derailed. Where do the latest virus outbreaks leave us?

5 min read

24 Feb 2020

Headline inflation shot up from 1.3% to 1.8% in January, although the “core” rate of 1.6% vs 1.4% was more benign. Key driver was household gas and electricity pricing, with last year’s price cap reductions falling out of the calculation. Clothing and Footwear prices also bounced back. There were also signs of some recovery in consumer sentiment seen in the reversal of December’s fall in Retail Sales, with the monthly figure jumping from -0.8% to +1.6%. Nothing here to suggest any policy shift from the Bank of England.

Worrying PMI data. The Composite activity index fall from 53.3 to 49.6, driven by a large drop in the hitherto resilient Services measure from 53.4 to 49.4. New Orders saw the first drop since 2009. There was some surprise that Manufacturing (50.8 vs 51.5) held up as well as it did in the face of COVID-19 supply chain concerns. Probably worse to come on this measure. At least Housing data continues to hold up well, with positive readings for both Housing Starts and Building Permits, possibly the result of a warmer-than-average winter.

Flash Eurozone PMIs showed a continued recovery at 51.6 vs 51.3 last month. This was the fastest growth in 6 months. However across the Eurozone suppliers reported that delays for inputs were the most widespread since December 2018 - in many cases blaming supply chain issues on the coronavirus outbreak. The PMI recovery could be a false dawn.

There remains a dearth of data from China, and even when we get it the distortions of both the Chinese New Year and then the coronavirus will make it somewhat meaningless. Car Sales in China were running at just 8% of the level a year ago in the first two weeks of February. Cinema box office sales are virtually invisible on a chart. There are some anecdotal signs that the worst has passed, but much uncertainty persists.

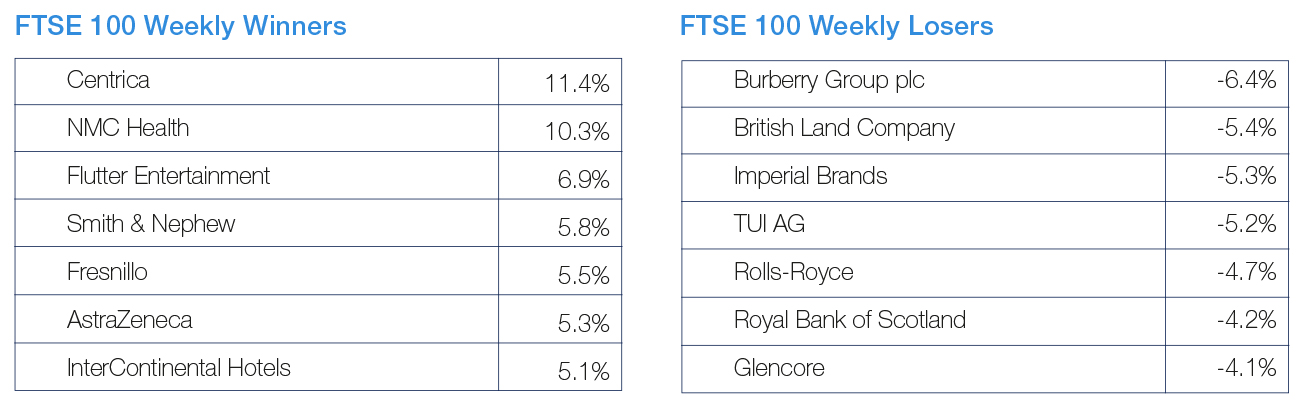

Source: FactSet

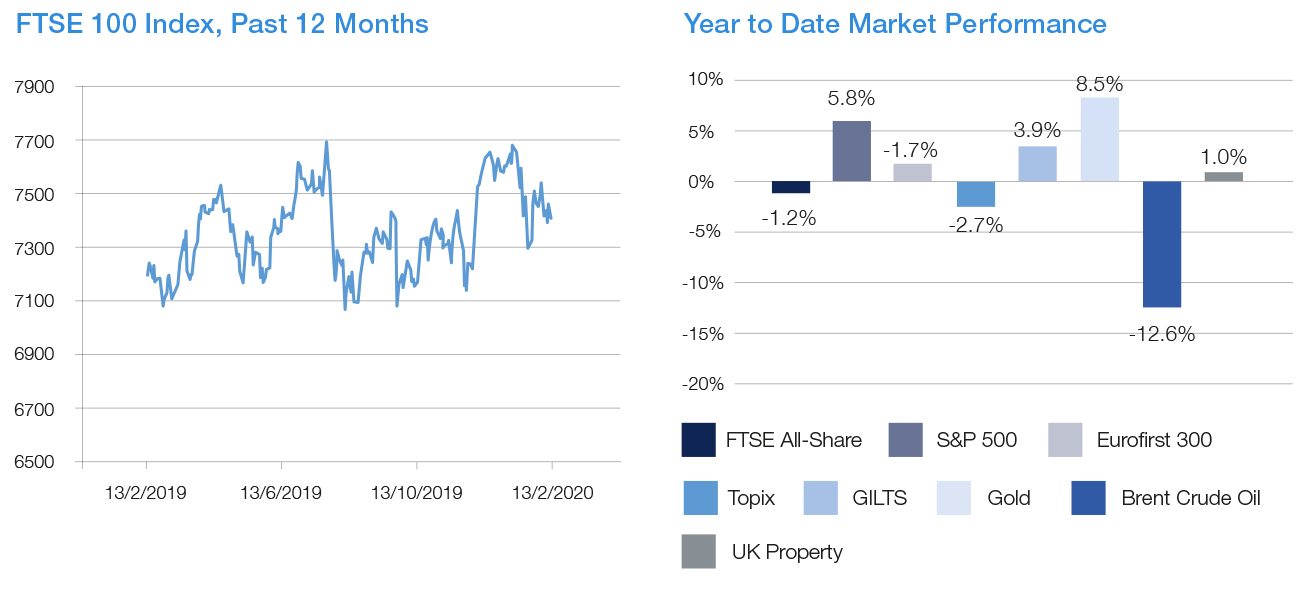

Source: FactSet