Welcome To VUCA

17 May 2021

Volatility, Uncertainty, Complexity and Ambiguity - a description of the current investing world.

5 min read

17 May 2021

GDP rose 2.1% in March, better than expected. The full first quarter, then, ended with activity down 1.5% on the final quarter of last year, thanks to the third lockdown. Gradual reopening promises a much better second quarter. For the full year, Investec Bank forecasts growth of 7.5%, with 8%+ not being out of the question. Meanwhile, no pause in the housing markets, with the RICS survey house price balance printing at +75 in April, a four decade high. This reflects low availability of suitable houses as well as the Stamp Duty holiday. These imbalances are set to drive prices for a while yet, but a slowdown in the rate of agreed sales, which is currently still very high, appears on the cards as tax incentives fade.

The key number was the April Consumer Price Index, where the headline reading came in at +4.2% y/y, vs an expected +3.6%, and 2.6% in March. Even Core CPI was very strong at +3%. Yes, a spike was expected, but not this big. No doubt strong demand is meeting some supply bottlenecks… but for how long? The Fed continues to call this spike “transitory”, but others are not so sure. The University of Michigan’s monthly survey of consumers saw the one year ahead expectations jump from 3.4% to 4.6%, and the 5-10 year expectation jump from 2.7% to 3.1%. Inflation expectations have not yet become “unanchored”, but the Fed must be getting concerned.

The latest monthly data paint a mixed picture of the economy in April. Unemployment fell to its lowest level since November 2019 at 5.1%, retail sales missed expectations (+17.7% vs f/c +24.9%), just +0.3% m/m. Industrial production was +9.8% y/y, vs +14.1% in March. This softer data release prompts further concerns of a drop in economic momentum. Gradual policy tightening by the Chinese authorities means that none of this is entirely unexpected, and annual GDP growth for 2021 is still expected to start with an eight, with Investec Bank on 8.8%.

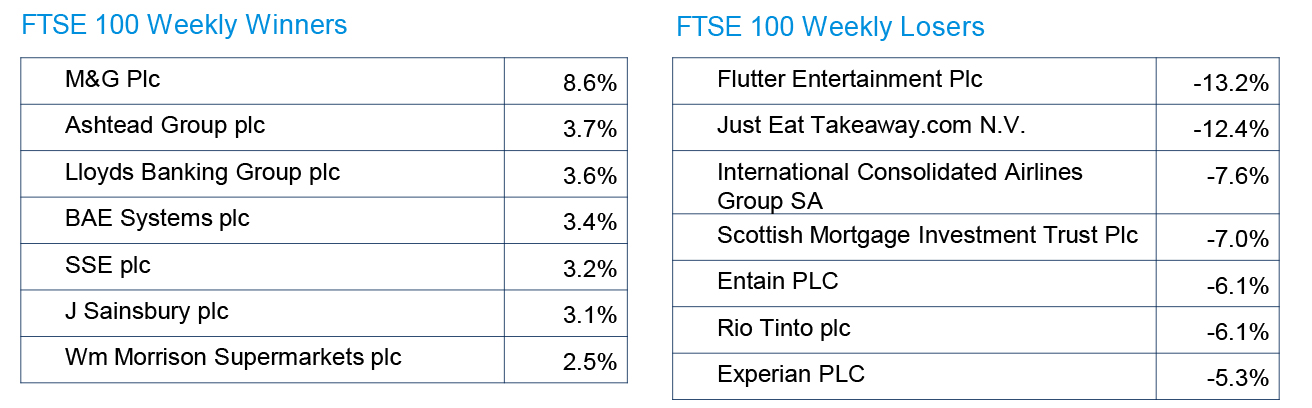

Source: FactSet

Source: FactSet