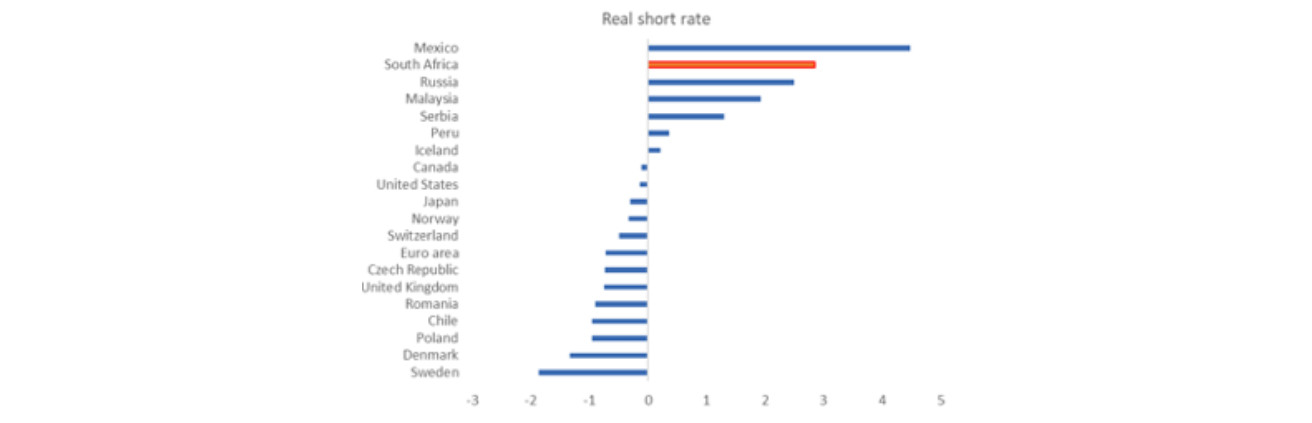

South Africa is near the top of the global league – when it comes to the rewards for holding money, that is. You can earn about 3% after inflation on your cash, with only Mexico having higher real short-term interest rates.

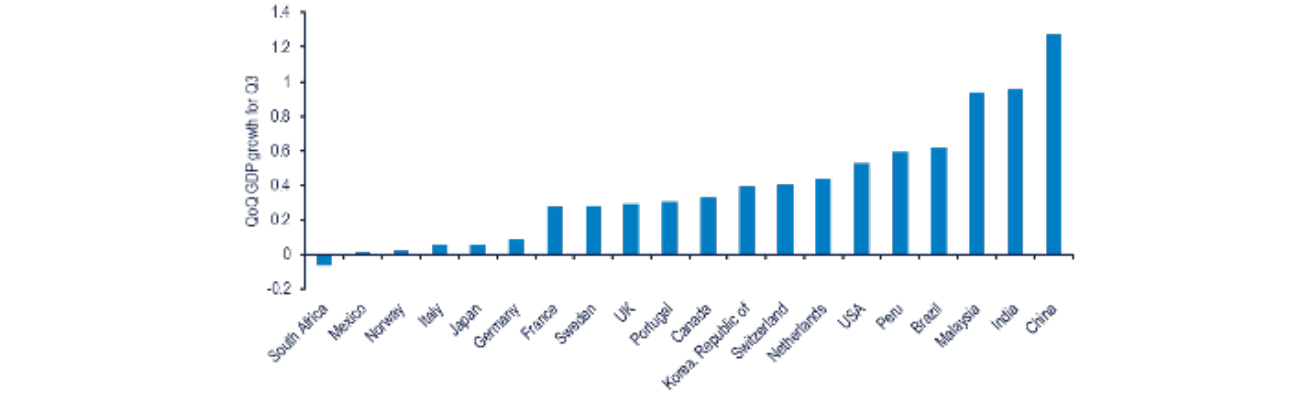

However South Africa is close to the bottom of the global growth league (see below). This is no co-incidence, but the result of destructive fiscal and monetary policies.

Figure 1: Third quarter GDP growth

Source: Thomson Reuters and Investec Wealth and Investment

Figure 2: Short-term rates less inflation

Source: BIS and Investec Wealth and Investment

Such an unnatural state of economic affairs, namely still very expensive money combined with highly depressed economic activity, has clearly not been at all good for SA business. The average real return on invested capital (cash in/cash out) has declined sharply, by about a quarter since 2012. Companies have responded by producing less, investing less, employing fewer workers and paying out more of the cash they generate in dividends.

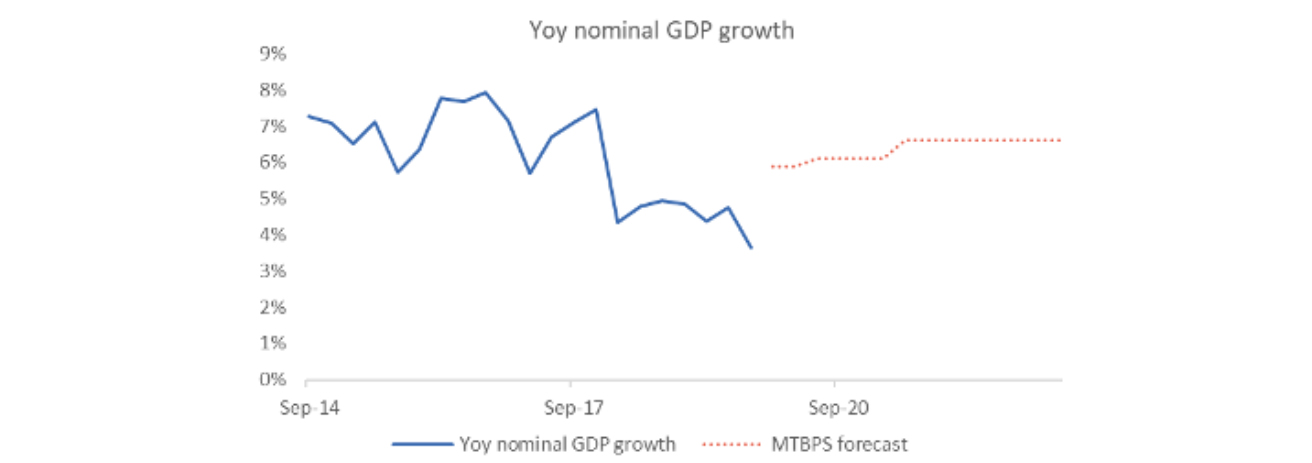

GDP at current prices is now growing at its slowest rate since the pre-inflationary 1960s, at about 4% a year. This combination of low GDP and inflation below 4% (yet with high interest rates) automatically raises the ratio of national debt to GDP. And it makes it much harder to collect taxes (the collection rates are well explained by these nominal growth rates). Of further interest is that the actual growth in GDP is falling well below the forecasts provided in the Budget Survey (see figures below).

This leads to an economically lethal combination of low inflation and high borrowing costs (for the government and others).

Figure 3: Nominal GDP growth

Source: Investec Wealth and Investment and Thomson Reuters

Figure 4: Nominal GDP growth vs forecast

Source: Investec Wealth and Investment and Treasury

Only actions by the government that clearly indicate it is heading away from a debt trap (ie printing money and so much more inflation in due course) can permanently reduce expectations of higher inflation and thus bring down long-term interest rates. Debt management is a task for the government, not the Reserve Bank.

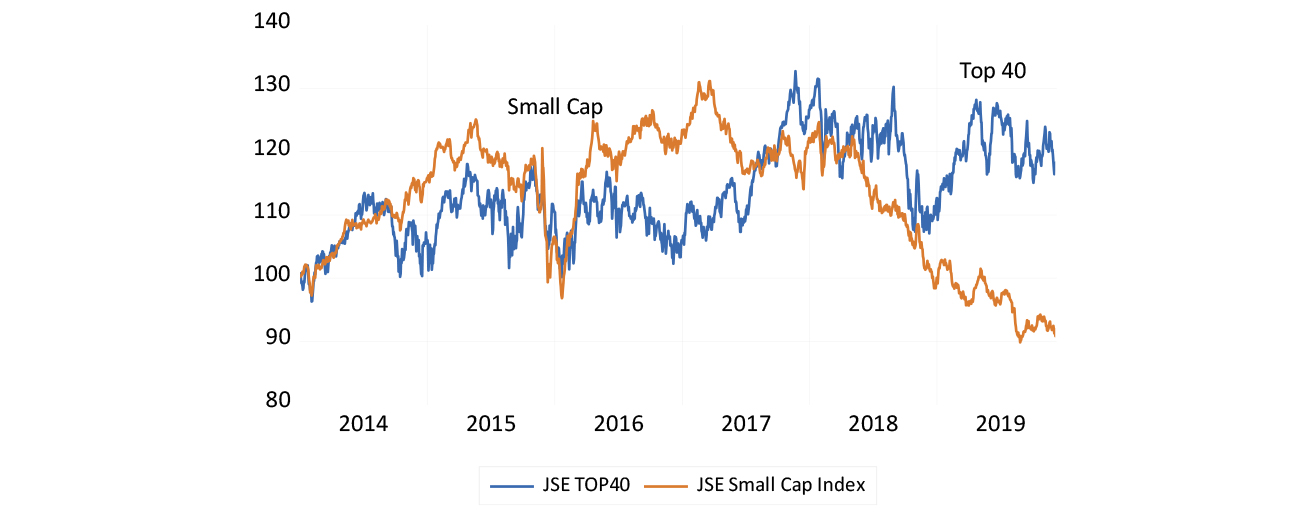

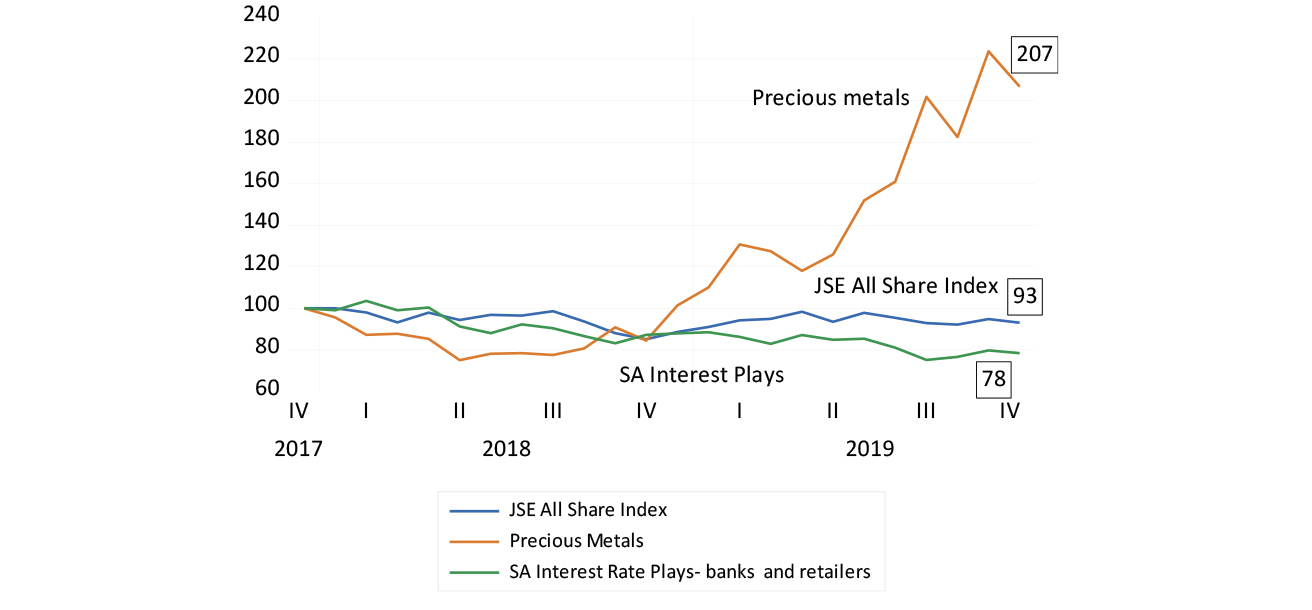

The investors in those companies that depend on the health of the domestic economy have not been spared the economic damage. The value of these South African economy-facing interest rate plays (banks, retailers and investment trusts for example) have declined significantly and have lagged well behind the JSE All Share Index. The JSE small cap index has lost 40% of its value since late 2016. Since January 2017, the JSE All Share Index is down by 7%. However an equally weighted index of SA economy plays is down by 22%.

Figure 5: Top 40 and Small Cap indices (2014 = 100)

Source: Bloomberg, Investec Wealth and Investment

Figure 6: JSE All Share Index, Precious Metal Index and SA Plays (equally weighted, 2017 = 100)

Source: Bloomberg, Investec Wealth and Investment

It’s against this worrying backdrop that I offer my New Year wish list for South African business to be able to transform its prospects and with it the prospects of all who depend on the domestic economy. It is after all business which is the most important contributor to the economic prospects of all South Africans.

My first wish is that those in government and its agencies should recognise that without a thriving business sector the economy is doomed to permanent stagnation. They should therefore show more respect for the opinions of business and the policy recommendations they make. Most important, they should interfere less in the freedoms of business to act as business sees fit.

The opportunities that economic growth provides are a powerful spur to upward mobility – of which poor South Africans are so sorely lacking.

Economic growth is transformational and inclusive. Stagnation is just that: nothing much happens, especially for the poor who are stuck in a state of deprivation from which it is difficult to escape. The opportunities that economic growth provides are a powerful spur to upward mobility – of which poor South Africans are so sorely lacking.

My second wish is that government turns over all wastefully managed SOEs to private control (there are no crown jewels) and in this way improve performance and generate cash and additional taxes with which to reduce national debt. Any sense from government that this might happen would bring long-term interest rates sharply lower and immediately reduce the returns required of SA business and in turn lead to more investment.

A third wish (linked to the second) for business success in 2020 is that government cuts its spending and raises revenues from privatisation, rather than raises tax rates next year. There is no scope for raising tax revenues unless there is faster growth. Higher tax rates will depress economic growth and growth in revenues from taxation still further. The wish is therefore that Treasury knows that only cutting government spending can avert the debt trap and has the authority to act accordingly.

Finally, a wish for monetary policy. South African business would benefit from lower short-term interest rates (notably mortgage rates) under Reserve Bank control. Lower interest expenses would help stimulate the spending of households, which could help get business going. It is my wish for business that the Reserve Bank will do what is most obvious and natural for it to do: to act decisively and urgently when both inflation and growth are pointing sharply lower.

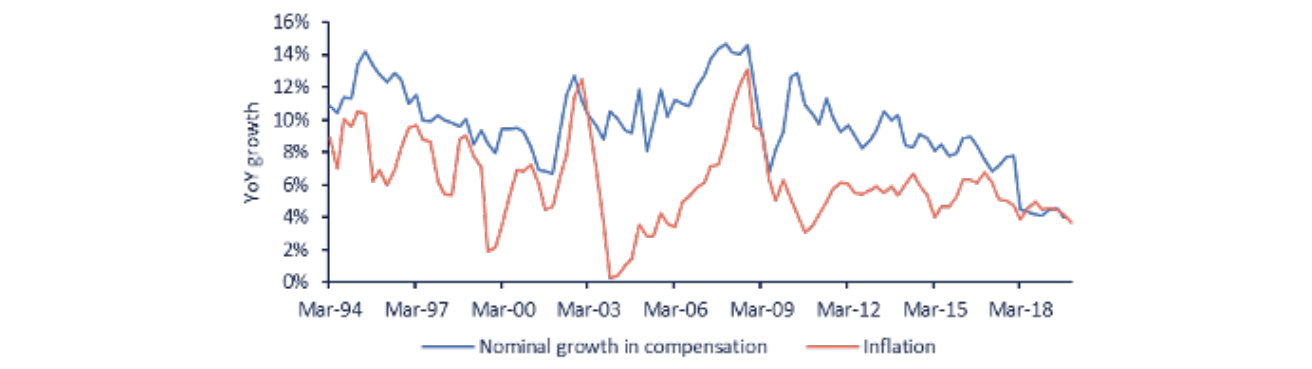

Figure 7: Nominal wage growth

Source: Thomson Reuters, Investec Wealth and Investment

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Investec products you may be interested in

Wealth Management

Offshore Investments

Investments

Wealth Management

Offshore Investments

Investments

Browse further in