Last week South Africans benefitted from a powerful demonstration of our integration into global capital markets. On Tuesday, the yield-to-maturity on the key 10-year US Treasury fell from 4.63% to 4.44%. By the end of the day, the 10-year RSA bond yield had declined by a similar number of basis points, from 11.66% to 11.45%. The yield on a dollar-denominated, five-year RSA bond fell from 7.52% to 7.19%, leaving the yield spread with the US Treasury, an objective measure of SA sovereign risk, slightly compressed at 2.76%. The US dollar weakened across the board. And with higher bond values the share markets almost everywhere responded agreeably for investors and pension plans. The JSE gained nearly 2% on the Tuesday (5% in US dollars) and again by a further near 2% on the Wednesday.

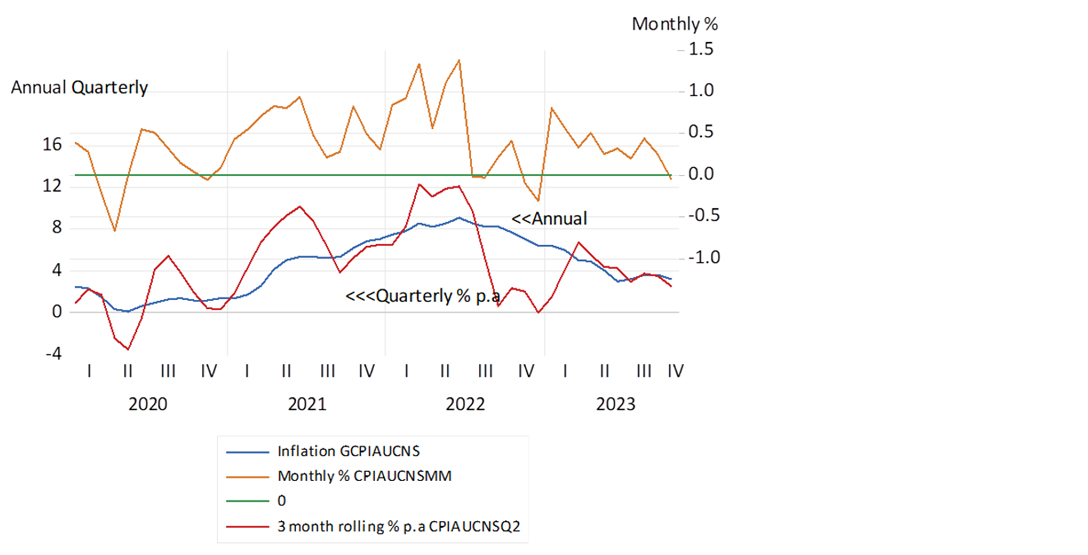

All of this on the news that inflation in the US had fallen by a little more than had been expected. The chances of further increases in short-term interest rates therefore fell away, as they have in South Africa. And long rates moved in sympathy. Should the US economy slow down sharply, as slowing retail spending suggested they would in a print released on Thursday, declines in US short rates will follow in short order, adding to US dollar weakness and rand strength. Or at least as investors, if not yet the Fed, thinks.

US Inflation: annual, quarterly and monthly

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment, 16 November 2023

Some may say this is much ado about relatively little – a mere blip in the inflation data. If you could predict nominal US GDP and interest rates over the next 10 years, you would be able to predict share and bond values with a high degree of accuracy.

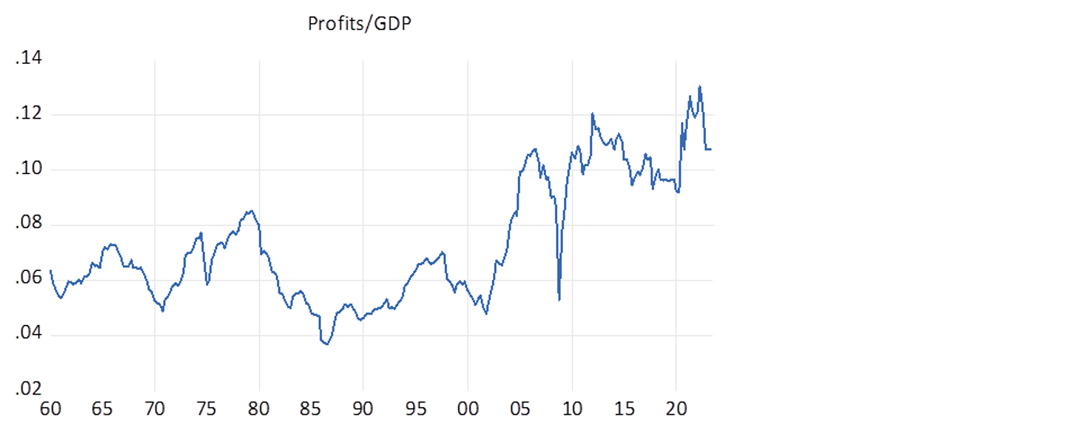

Perhaps the most intriguing feature of recent trends in US GDP has been the growing share of corporate profits after taxes in GDP. The ratio of these profits to GDP has nearly doubled since the early 1990s. A profit ratio that investors must hope managers, with the aid of R&D, in which they invest so heavily, can defend to add to share values.

Another question about the long-run value of US corporations and their rivals elsewhere will be about the cost of capital by which their expected profits will be discounted. A puzzle that has arisen is: why have long-term interest rates in the US increased as much as they have this year? It is not inflation expectations that have driven up yields. They have remained well-contained despite higher rates of inflation. Quantitative tightening – the sale by the Fed and other central banks of vast amounts of government bonds bought after the Global Financial Crisis and during Covid-19, is surely part of the explanation.

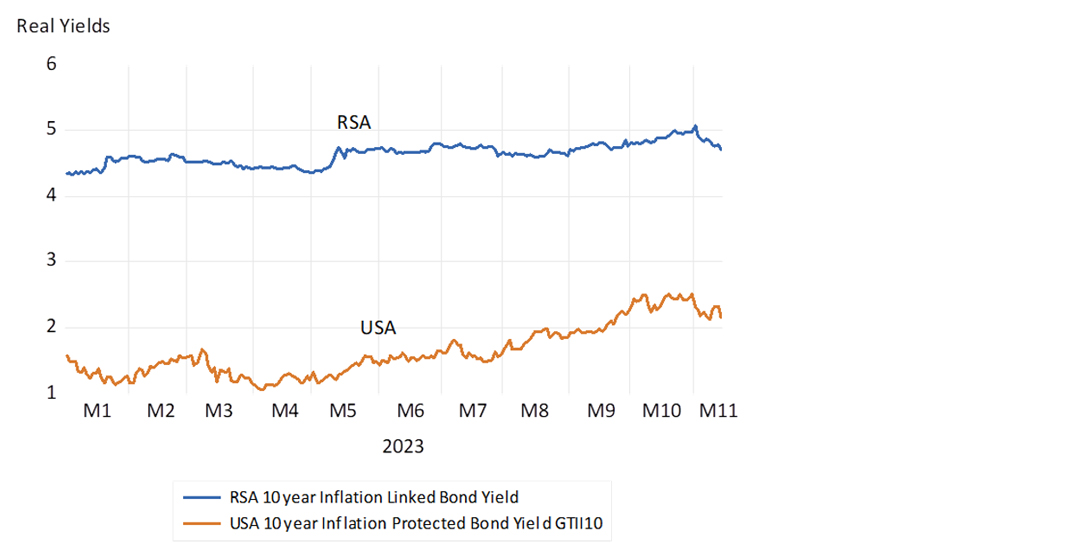

But it is not only vanilla bond yields that have risen this year. Real yields (inflation protected) have risen dramatically this year, from near zero earlier in 2023 to their current over 2%. Capital has become not only more productive of profits in the US, but it has also become more expensive in a real sense, to counter productivity and profit gains when valuing companies. Will it remain so? That is the trillion-dollar question.

US share of after-tax corporate profits in GDP

Source: Federal Reserve Bank of St Louis, Investec Wealth & Investment, 16 November 2023

The gap between real interest rates in SA, where a low-risk 10-year inflation linker offers over 4% – making for very expensive capital for SA corporations – has narrowed sharply. Surprisingly perhaps, real interest rates in SA have not followed global trends, making for at least relatively lower costs of capital for SA-based corporations. This is good news, which we can hope will lead to more investment.

10-year inflation-protected real bond yields in SA and the US

Source: Bloomberg and Investec Wealth & Investment, 16 November 2023

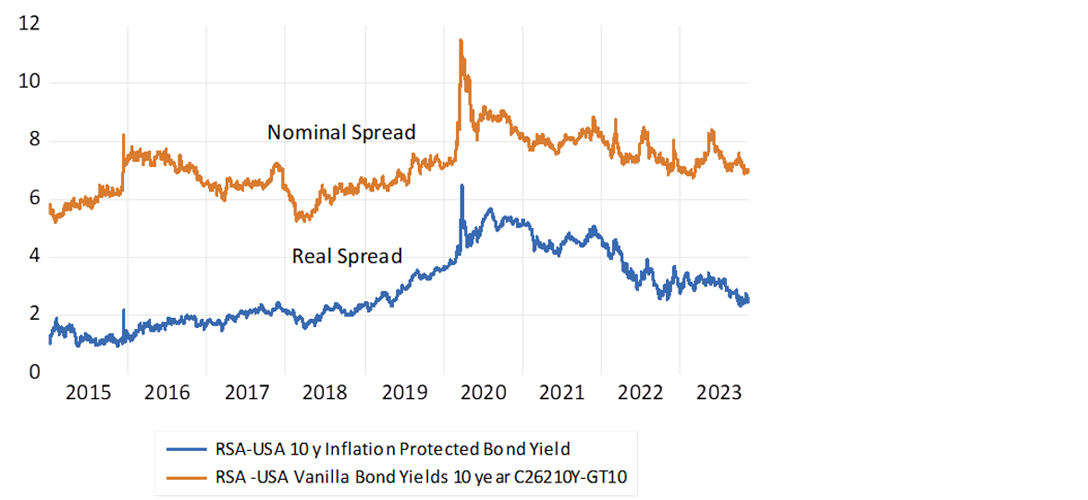

Risk spreads – RSA minus US 10-year bond yields

Source: Bloomberg and Investec Wealth & Investment, 16 November 2023

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Browse further in