Starbucks has a prominent notice. Responsibly cashless. It might have read better (or more honestly) as profitably cashless. Avoiding the costs and dangers of handling and transporting cash and the associated bank charges – including the likelihood of cash not making it to the till in the first instance – is surely in the owner’s interest and justifiably so. This is on the proviso that the sales lost would not be significant as affluent and tech-savvy customers tender their smartphones to pay. Others may have a different view. For example, the owner-manager of a small stand-alone enterprise in control of what goes in or out of the cash register may come to a different view. For them cash is still king.

Starbucks and other cash refusers are probably within its rights to refuse legal tender. Only the notes and coins issued by the Reserve Bank qualify as legal tender in SA – money that cannot be refused in proposed settlement of a debt. However, it presumably can be rejected when offered in exchange for a good or service. SARS would probably prefer a cashless society for obvious income monitoring purposes. The Reserve Bank might, were it a private business, have mixed feelings about reducing the demand for a most valuable monopoly. It pays no interest on the notes it issues and earns interest on the assets that the note liabilities help fund. In 2004, the note issue funded 40% of the assets on the Reserve Bank’s balance sheet. That share is now down to 15%. It was 20% before Covid.

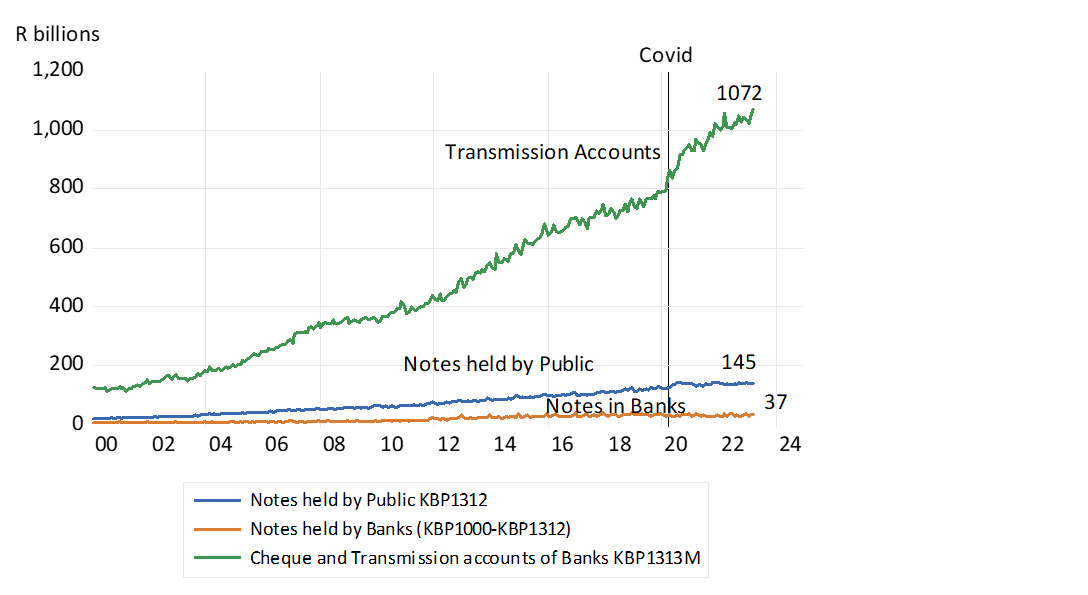

The above demonstrates how notes have lost ground to the digital equivalent – a transfer made and received via a banking account, a trend that becomes conspicuous after the Covid lockdowns. Since then, the transmission and cheque accounts at SA banks have grown strongly, from R790bn in early 2020 to nearly R1.1 trillion today, or by about a quarter. By contrast, the notes issued by the Reserve Bank since have increased only marginally – by R20bn – with most of the extra cash issued being held by the public. The banks have managed to reduce their holdings of non-interest bearing cash in their vaults and ATMs. Replacing notes with digits has been a cost-saving response. A central bank replacing paper notes with a digital alternative could be an alternative. But it would threaten the deposit base of the banks and their survival prospects.

Money supply trends

Source: SA Reserve Bank and Investec Wealth & Investment, 19 July 2023

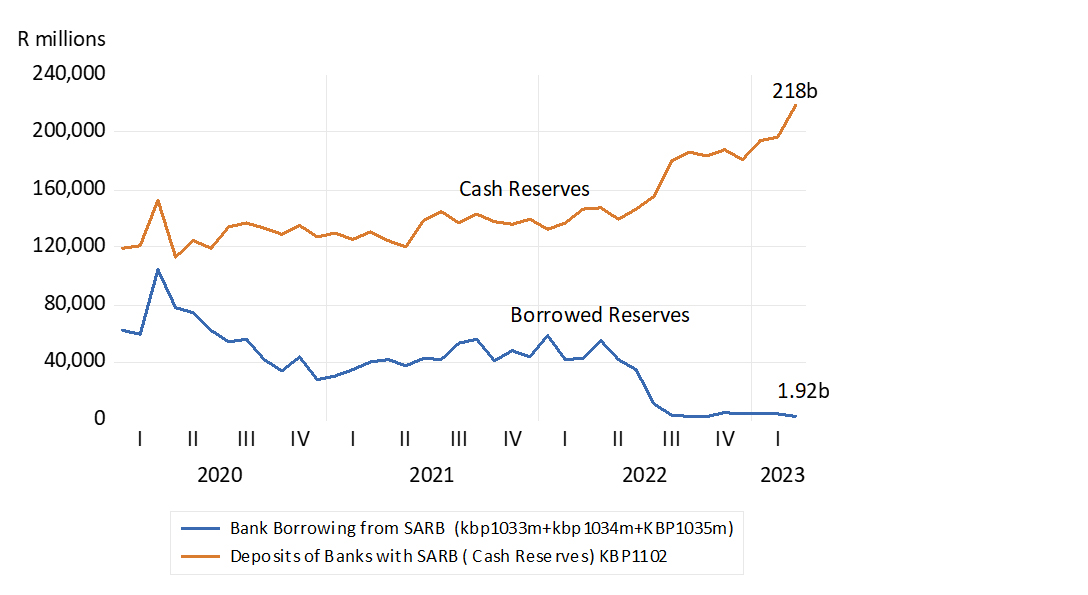

The banks however dramatically increased their demands for an alternative form of cash, namely deposits with the Reserve Bank. They now earn interest on these deposits. What used to be significant interest charged to the banks when they consistently borrowed cash from the Reserve Bank (to satisfy the cash reserve requirements that it sets), at the Repo rate, has now become interest to be earned on deposits held with the Reserve Bank. These deposits have grown by R100bn since 2020 while cash borrowed from the Reserve Bank has fallen away almost completely from an earlier average of about R50bn a month.

SA banks – demand for and supply of cash reserves since Covid-19

Source: SA Reserve Bank and Investec Wealth & Investment, 19 July 2023

The Reserve Bank, following the Fed, regards the interest it pays on these deposits as fit for the purpose of preventing banks from converting excess cash into additional lending, which would lead to increased supplies of money in the form of additional bank deposits. It takes a willing bank lender and a willing bank borrower to power up the supply of cash supplied to the banking system by a central bank and turn them into extra deposits. The testing time for central banks in a banking world full of cash will come when increased demands for bank credit accompany the improved ability and willingness of the banks to turn excess cash into extra bank lending. Then interest rate settings may not control the demand by banks for cash reserves to sufficiently restrain the conversion of excess cash into additional bank lending, which in turn will lead to extra and possibly excess supplies of money. This should then lead to extra spending as money is exchanged for goods, services and other assets that will force prices higher. Clearly this is no longer a problem for South Africa or the US where the supply of money is in sharp retreat.

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Browse further in