From President Cyril Ramaphosa’s State of the Nation address to the recent Mining Indaba, to the updates from listed companies, the message is clear – the ongoing load shedding in South Africa has become a serious constraint on growth and profitability for the country's corporates.

Combined with the impact of the breakdown in SA’s transport infrastructure, load shedding is undermining the country’s ability to continue its recovery from the Covid-19 lockdowns, even as interest rates rise in response to high inflation.

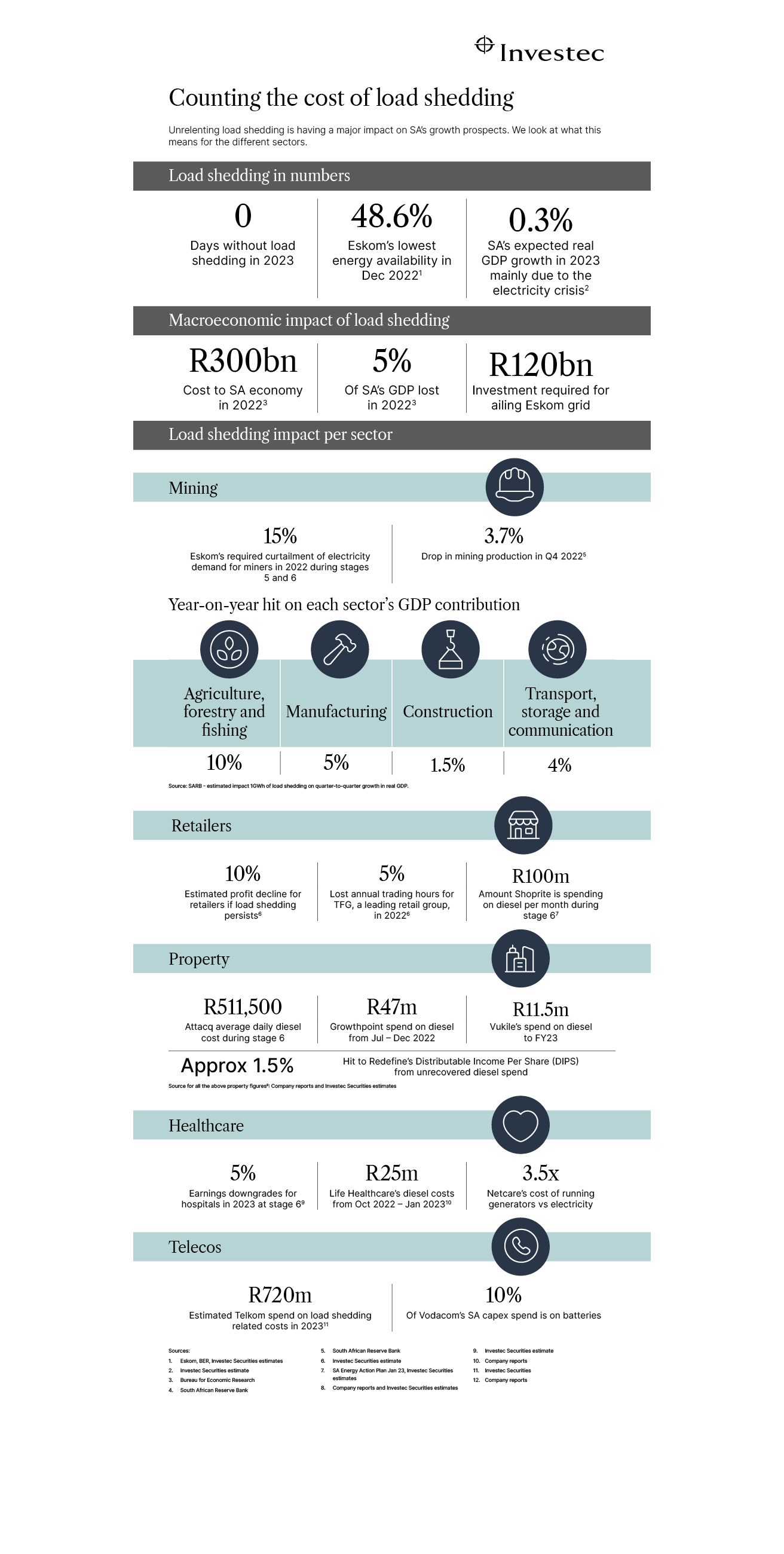

As Eskom’s energy availability factor (the difference between the maximum availability and all unavailabilities) fell to 50.4% in December, setting off the increased levels of load shedding since then (there have been no days without load shedding in 2023 so far).

But what are the real effects of load shedding on different industries, and the South African economy overall? Ayan Ghosh, investment strategist at Investec, has done some work on the topic.

The impact of loadshedding

According to the latest Reserve Bank estimates, load shedding had a negative impact of 2.1% on quarterly GDP in the third quarter of last year, with agriculture, forestry, and fishing the most impacted. Estimates for the fourth quarter have not yet been released, but the impact may well be higher, given that load shedding occurred on all but three days during the final quarter of the year.

Recent news flow has revealed some of the impacts on the economy and specific sectors, especially when stage 5 and 6 load shedding has been implemented.

Impact on the mining sector

Mining production, for example, fell by 3.7% in the fourth quarter of 2022. At the recent Mining Indaba in Cape Town, platinum sector representatives noted that they were able to manage the impact of load shedding up to level six, but would become a major issue thereafter, with the risk of shaft closures and job losses. Heavy rains in the fourth quarter and February have added to the challenges mining firms face.

According to the Minerals Council, the sector has navigated the current load shedding crisis relatively well, since miners were required by Eskom to curtail electricity demand by 15%, when Eskom implemented intermittent Stage 5 and Stage 6 load-shedding across the country late last year.

Listen to our podcast on the impact of the Eskom crisis on mining

Henk Langenhoven, Chief Economist of the Minerals Council of South Africa joins Investec's Treasury Economist and Power & Infrastructure team to discuss the impact of loadshedding on the mining sector and the wider economy.

Impact on agriculture

Meanwhile, load shedding could have an impact on SA’s food production, transport and storage. According to the Agricultural Business Chamber of SA (Agbiz), persistent load shedding has already hurt production.

Agbiz Chief Economist Wandile Sihlobo wrote in January that the consequences of load shedding are being felt in many areas:

- Field crops, fruit and vegetables that rely on irrigation. “Roughly 20% of maize, 15% of soybean, 34% of sugarcane, and nearly half of the wheat production are produced under irrigation,” noted Sihlobo.

- Red meat, poultry, piggery, wool and dairy production, all of which require continuous power for their usual activities.

- Downstream activities such as milling, bakeries, abattoirs, wine processing, packaging, and animal vaccine production, face similar challenges.

“Exporting agribusinesses, especially those with products highly sensitive to delays, such as fruits, red meat, and wine, are also worried about the port activities, which fortunately haven’t been primarily affected,” said Agbiz. “There are also food security concerns as the effect of load shedding will probably show in the volumes of products to be harvested/produced later in the coming months due to the time lag in agricultural production stages.”

Other affected sectors

Retail

Stage five and six load shedding has a significantly negative impact on the retail industry, notes Ghosh. Shoprite, for example, has been spending R100m on diesel every month during periods of Stage 6 load shedding. Ghosh says his analysis suggests that retail profits could decline by about 10% if the current load shedding patterns persist.

Property

Similarly, property companies (many of which are highly exposed to the retail sector) often face the same issues as retailers. Ghosh says that, according to Attacq (owner of the Waterfall precinct), its average diesel cost per day rises to R511,500 in the event of Stage 6 load shedding, from R170,526 per day during Stage 2 load shedding.

While solar generation is increasingly an option for shopping centres, this will take some time. For example, according to Redefine, solar generation currently makes up only about 17.8% of its energy consumption in malls.

Healthcare

Meanwhile, hospital groups also face rising costs when higher stages of load shedding are implemented. In its latest trading update, Life Healthcare said its diesel costs in the four months to the end of January increased to R25m, from R5m in the previous comparable period. Life Healthcare notes however that this is not significant in its overall cost structure.

The way ahead

These numbers are concerning and could get worse if the government, Eskom and other stakeholders are unable to improve conditions on the grid and don’t accelerate the rollout of independent power projects to alleviate the burden on Eskom.

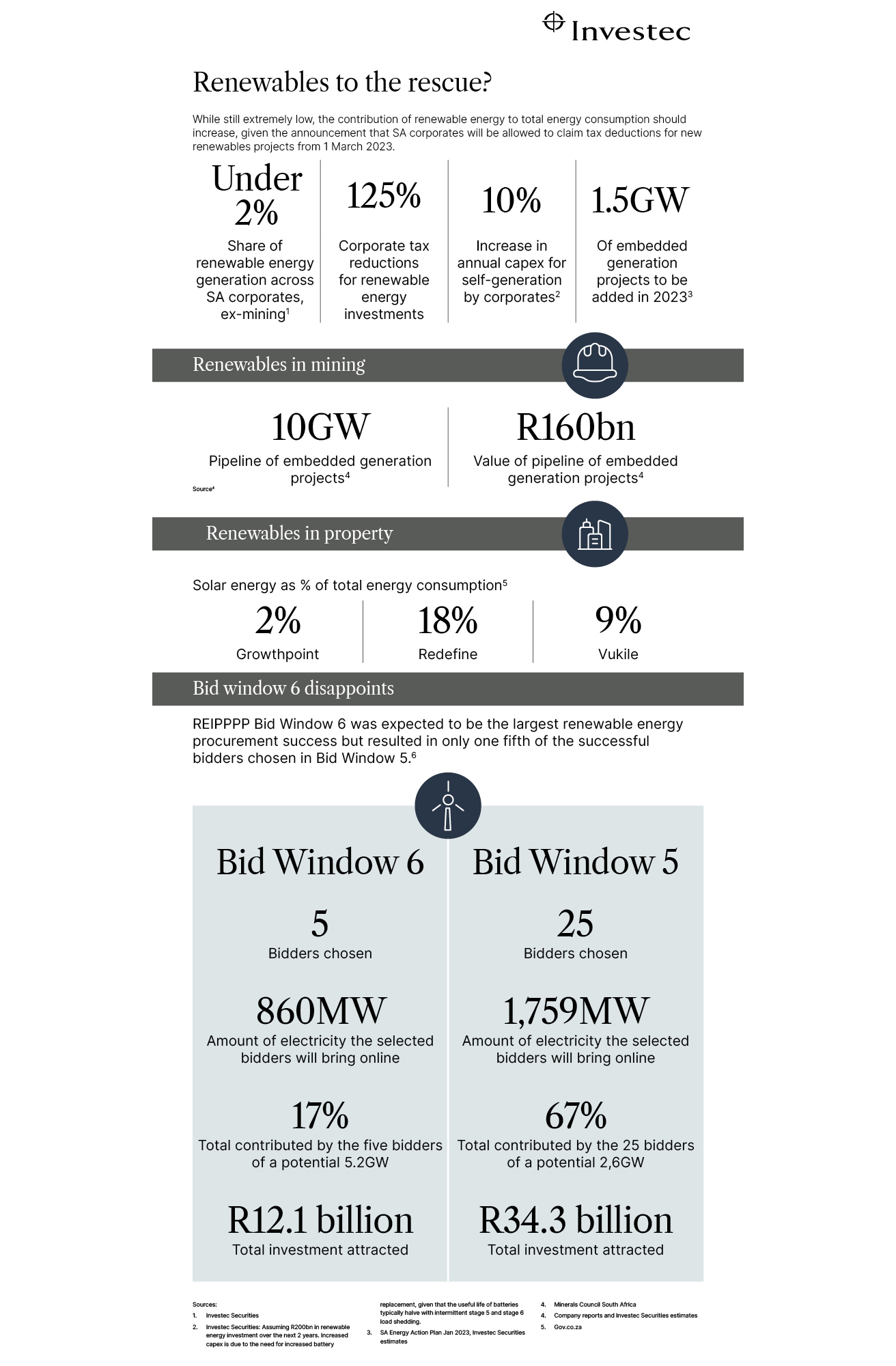

“We see an increased risk of load shedding in the medium term, following the failure of bid window 6 of the renewable energy independent power producers’ programme (REIPPP), according to media reports,” says Ghosh.

“While Bid window 6 was expected to be the largest energy procurement, only five bidders were chosen in Q4 22, producing a total 860MW, or 17% of the full 5.2GW.”

Speaking at a recent Investec webinar, Roger Baxter, head of the Minerals Council, emphasised the need to reconfigure the grid, which requires significant new investment of about R120bn. “This can only happen if government removes the transmission into a stand-alone government company,” he said.

Baxter however that there were some positives to be drawn out of the proposed interventions by President Ramaphosa to resolve the power crisis. These included:

- The interventions to lift the licensing requirement to 100MW followed by a complete withdrawal of the licensing requirement have resulted in a pipeline of mining sector embedded generation projects of 10GW, valued at about R160 billion.

- The timeframe for environmental authorisations has been reduced to 53 days for projects gazetted as Strategic Infrastructure Projects.

- The timeframe for registration with NERSA has been reduced from four months to an average of 14-19 days.

- The timeframe for grid connection has been reduced from 210 days to 105 days.

- The timeframe for land-use authorisations for energy projects has been reduced from 90 to 30 days.

Baxter also acknowledged that there were risks of increased electricity load shedding, as we approach winter. Yet, he remained hopeful that Eskom’s energy availability factor would improve, as we have typically seen during previous winters, when Eskom brought back into service additional generation units that had been under planned maintenance.

Measures such as the tax rebate for the installation of solar panels (125% for companies), announced in the Budget, will also hopefully assist South Africans to access affordable energy and reduce reliance on the grid.

Ultimately, South Africa’s infrastructure problems will require private sector investment in electricity (and rail), including through public-private partnerships (PPPs). Studies suggest that, for every 10% decline in the total fixed capital stock share owned by the government, South Africa’s growth rate could improve by 2 percentage points.

“By reducing government’s share of the total fixed capital stock to 23%, combined with other critical reforms (such as tackling crime and reducing red-tape), South Africa could engender a +5% a year GDP growth rate,” concluded Baxter.

Get Focus insights straight to your inbox

Freedom Won

Investec Corporate Leverage Finance provided a bespoke funding solution to meet Freedom Won’s robust growth needs.

Old Mutual Alternative Investments

Investec provided a fund finance facility to OMIGSA International Private Equity Fund V - an international fund of fund vehicle of OMAI.

EDF Renewables

Investec has partnered with EDF Renewables (South Africa) to reach financial close on the third of the three Koruson 1 projects.

Angolan Ministry of Finance

Investec has successfully closed a EUR34m commercial facility with the Angolan Ministry of Finance.

LCI Helicopters

Financing of one Airbus H175 helicopter and one Leonardo AW169 helicopter providing mission critical services.

IHS Holding Limited

Investec has lent USD25m to IHS, as one of the Lenders in their USD600m head office syndicated loan facility.

Browse further in