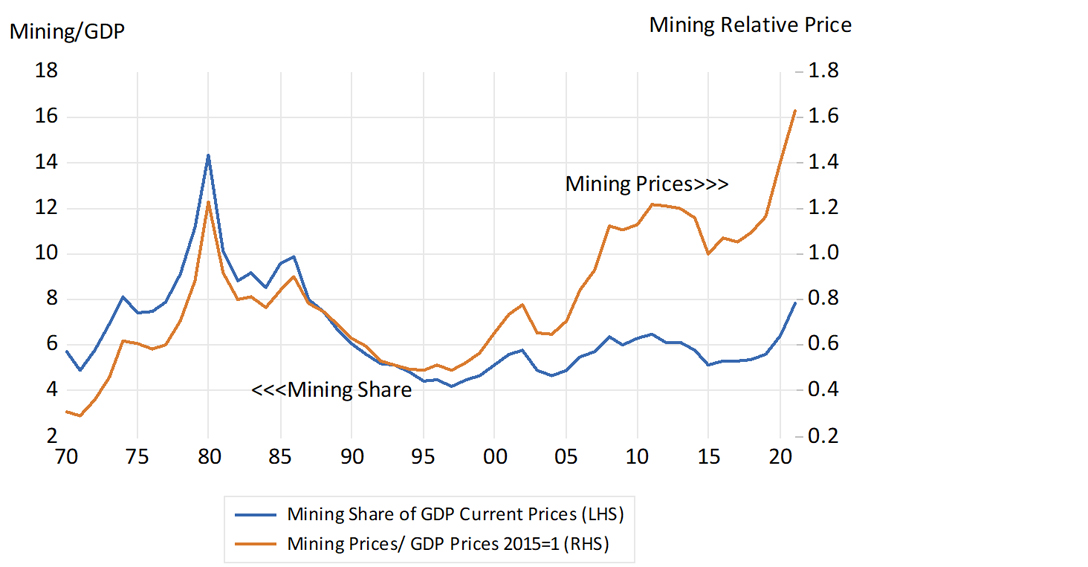

The surge in inflation worldwide has been helpful for South Africa. Higher prices for our mostly metal and mineral exports have boosted the profits of our miners and the taxes and royalties collected from them. In real terms, represented by the ratio of the prices of the mining sector (the mining deflator to prices in general, represented by the GDP deflator) these price trends have never been more helpful to the sector.

The price-to-cost ratio in the mining sector is now even more favourable than it was in 1980, when the gold price rose from US$35 to US$800 an ounce and when gold mining was by far the largest contributor to total mining revenues and output. Real mining prices rose by 60% between 2015 and 2021. They have improved by three times since 1996. These real prices and profits have a highly predictable influence on mining output and the share of mining in GDP. The current share of mining output in GDP has doubled from 4% in the late 1990s to 8% now. There could and should be much more mining revenue, output and employment to come.

Mining’s share of GDP and real mining prices (2015 = 1)

Source: SA Reserve Bank and Investec Wealth & Investment, 3/3/2022

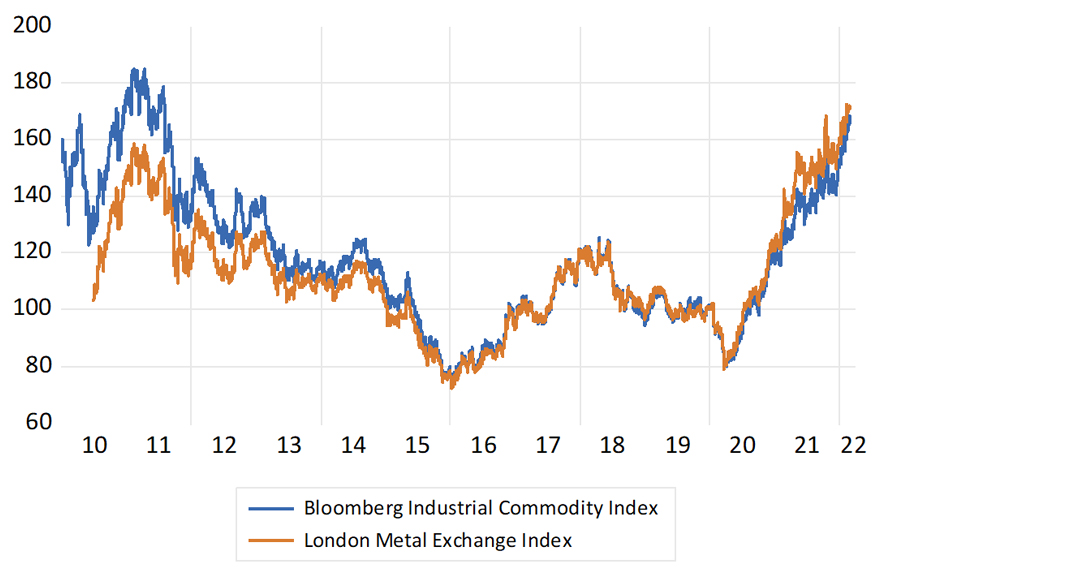

The prices of commodities used in industry are more than 60% higher than they were before Covid-19 and have increased by about a further 8% this year. They are now back to where they were in 2010 when Chinese stimulus, post the Global Financial Crisis, had a favourable influence on demand for metals and their value, a force that faded away as supplies responded. There are more profits and tax revenues to come as a result of the continued advance of industrial metal prices since last year, sadly further stimulated by Russia’s war on Ukraine. They are also being encouraged over the long run by a more disciplined global mining sector, investing heavily in cleaning up rather than producing more.

Industrial commodity and metal prices (January 2020 = 100)

Source: Bloomberg and Investec Wealth & Investment, 3/3/2022

The revenues and profits realised by the local mining sector have helped to add about R200 billion or a meaningful extra 15% to the original estimate of national Budget revenues of R1.35 trillion in 2021-02. The extra revenue helped reduce government borrowing in that Budget year by about R136bn. More important is that tax revenues for the 2022-23 fiscal year have been revised higher by a further R141bn, of which a further R77bn is earmarked to reduce the government’s borrowing requirement. These revenue estimates may again prove too low, which would be further good news, especially if it leads to growth-stimulating lower tax rates, rather than more spending. The prospect of permanently higher metal prices has already had important effects on the value of the rand and the JSE, both of which have largely escaped the influence of a stronger US dollar and weaker global equity markets.

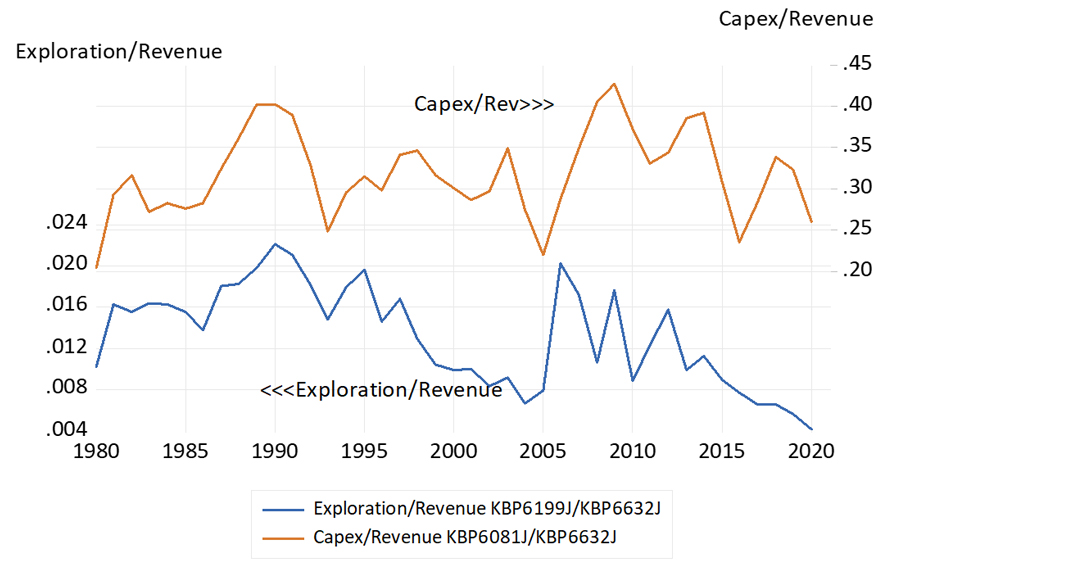

The disappointing news from the local mining front is how little is being added to capex and even less to exploration budgets. The capex-to-revenue ratio is running at a below-average level, while the exploration spend has all but vanished.

Capital and exploration activity in SA mining – ratios to mining revenues

Source: SA Reserve Bank and Investec Wealth & Investment, 3/3/2022

The objective of policy and the hope for the economy should be to turn about these unpromising trends. The most promising opportunities lie in the exploration and development of gas and oil. Important recent discoveries have been made off the Southern Coast. Even more significant, oil and gas have been discovered on the maritime boundary of Namibia and South Africa. The Venus 1 discovery made by Total is the largest ever discovery of gas and oil in Africa. This follows the significant Graf 1 find of Shell in the same area. Block 1, in South African waters, is a further opportunity. The Kudu gas prospect can still be realised.

The opportunity for Europe to replace Russian gas and oil with South African resources – closer to Europe than Siberia – should be promoted actively.

A further point relates to the infrastructure that supports the minerals sector. Exxaro, one of South Africa’s leading mining firms, recently noted that the shortcomings of Transnet – getting coal to the ports to its customers abroad – cost it some 4 million tonnes in coal production last year, or 10% of total production. This is a meaningful opportunity cost to all stakeholders, including shareholders and the fiscus in the form of foregone taxes on profits. Exxaro’s experience is unlikely to be unique.

What is needed is a mining and exploration agenda for growth, that is, an internationally competitive set of regulations and an enabling environment that encourages the miners and drillers to get on with bringing valuable resources to the surface. They need to be introduced without the distractions and diversions that often complicate and delay development. Achieve growth and the transformation of the opportunity set for all South Africans will follow. Carpe diem.

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Browse further in