South Africa is facing a range of simultaneous economic challenges. In particular, Eskom and Transnet remain constraints on South Africa’s growth outlook. Listed companies continue to flag how power rationing and logistics constraints impact both their top line (revenues) and bottom line (net profit), highlighting how these challenges impact production and thus volumes as well as operating costs. In the current inflationary environment, these are net negatives as producers continue to attempt to push rising costs onto the consumer. In this thematic article, we unpack the relative impact that improvements to these structural constraints could have on a selected pool of economic variables including exports, GDP growth, employment and household final consumption expenditure – as well as the overall implications for equity markets.

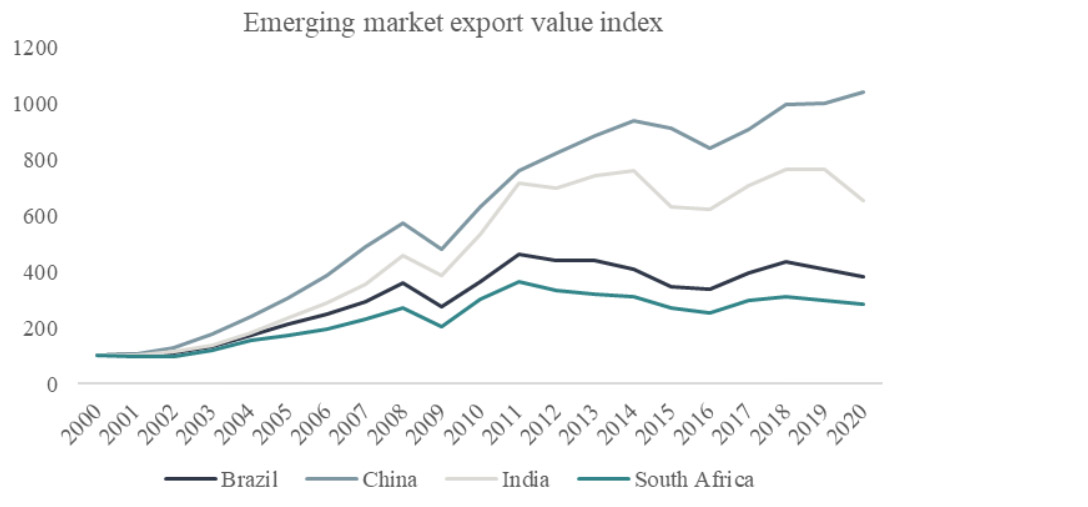

Our first illustration of the relative performance of South Africa export volumes, given its structural problems, relative to emerging market peers, as represented by Brazil, China and India (Chart 1 below). South Africa has underperformed its emerging market peers since 2000, and the slow pace of export volume growth capacitation has been particularly pronounced since 2011. Brazil, the next laggard in the series, is nevertheless outperforming South Africa by about 20%.

Chart 1: Emerging markets export volume growth

Date sampled: 28-Mar-23

Source: Investec Wealth & Investment, World Bank

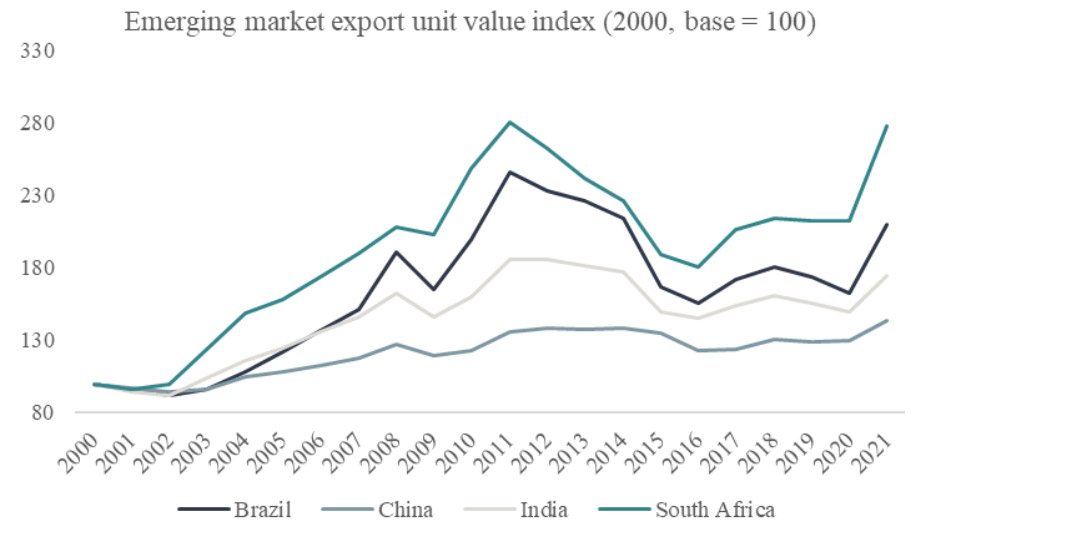

Perhaps the most disappointing aspect of our poor export volume growth is captured in chart 2 below. South Africa has outperformed emerging market peers in terms of export unit value growth, that is, the pricing of our export basket has been favourable in comparison with emerging market peers. That indicates that our export commodity basket, or the mix of goods that we export, has benefited from price appreciation relative to other emerging markets. This basket has consistently outperformed emerging market peers since the year 2000. The key point is that, when we unpack export revenues for South Africa, which is a function of price multiplied by volume, South Africa ticks the correct boxes when it comes to price (a function of the export basket) but doesn’t when it comes to volume.

Chart 2: Emerging market export values growth

Date smpled: 28-Mar-23

Source: Investec Wealth & Investment, World Bank

Our inhouse view is that the US dollar will depreciate this year. At the same time, Bloomberg consensus estimates global GDP growth of between 2% and 3% for 2023. We modelled this scenario and what its relative impact is likely to be on South African export basket prices. The results indicate that, in this scenario, our export prices would appreciate by between 14% and 25%. All other variables being constant, this would be a net positive for South Africa, and in particular for our exporters (agriculture and mining) and nominal GDP. Nominal GDP is important for South Africa’s fiscal outlook since it affects both tax revenues and the debt-to-GDP trajectory.

Chart 3: South Africa export pricing scenarios

Date: 28-Mar-23

Source: Investec Wealth & Investment, World Bank, Bloomberg

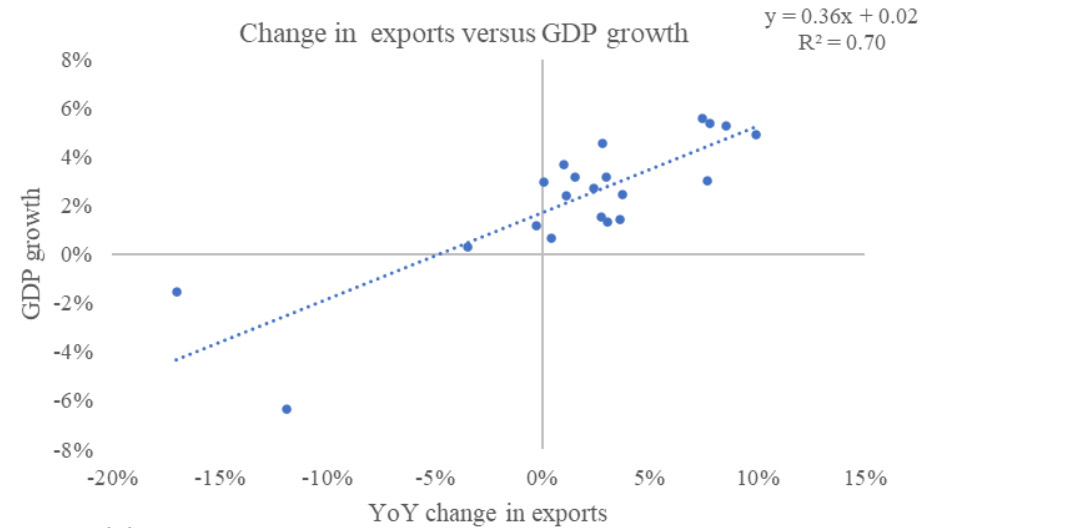

What about export volumes? We next looked at what the relative impact would be if our exports performed more or less in line with Brazil (i.e. SA exports up 20%) on GDP growth, employment and household final consumption expenditure.

The first point is that export volume growth is positively correlated with GDP growth. Chart 4 below shows that higher export volume growth is, as expected, positively correlated with higher GDP growth. If South Africa had performed more or less in line with Brazil, we would expect GDP growth to be about 7% higher. This is materially above the current GDP growth trajectory for South Africa, which points to expectations of between 0% and 2% growth over each of the next two years. An improvement in the situation when it comes to our structural problems, which are currently impediments to export growth, would have a substantial positive impact on GDP growth.

Chart 4: Exports and GDP growth

Date sampled: 28-Mar-23

Source: Investec Wealth & Investment, World Bank

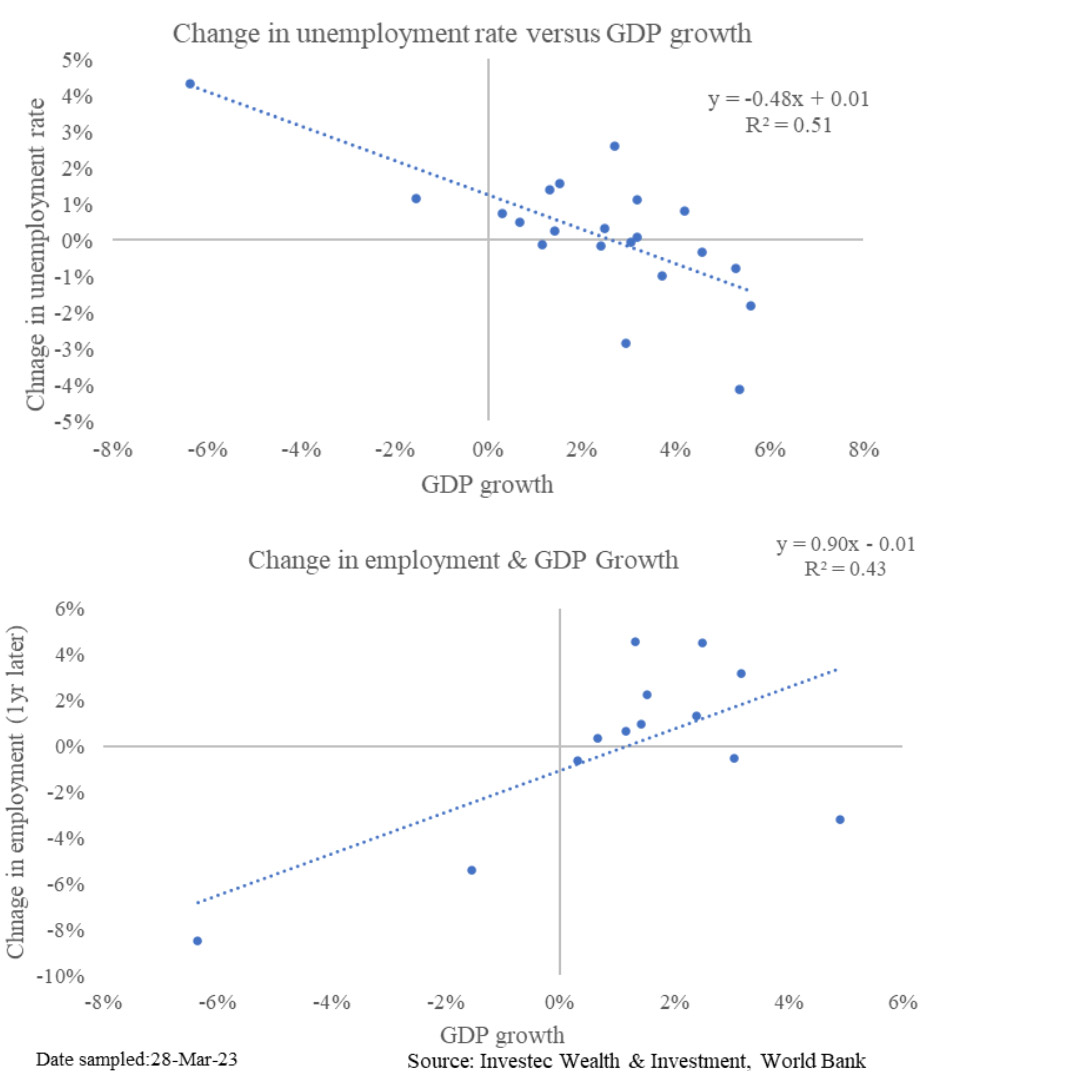

The second point that charts 5 and 6 below show is that GDP growth is correlated with improved employment outcomes one year later. It similarly shows that the only meaningful level of GDP growth that has an impact on unemployment alleviation is GDP growth when it is above 2%. We have already illustrated that a 20% boost to export volumes would result in GDP being 7% higher, materially above what is required for improved employment. According to StatsSA, the unemployment rate for South Africa was 32.7% in the fourth quarter of last year. If we were to fix our structural problems over the next two years, it would lead to an extra 7% growth over the period, or 3.5% extra each year and we would expect the unemployment rate to fall by around 3%. In this environment, total employment would rise by around 3% too. An improvement in GDP would have a material impact on employment in South Africa, but only if GDP growth is above 2%. Improving our export volumes would therefore positively impact employment dynamics in South Africa. .

Charts 5 and 6: GDP growth and employment

Date sampled: 28-Mar-23

Source: Investec Wealth & Investment, World Bank

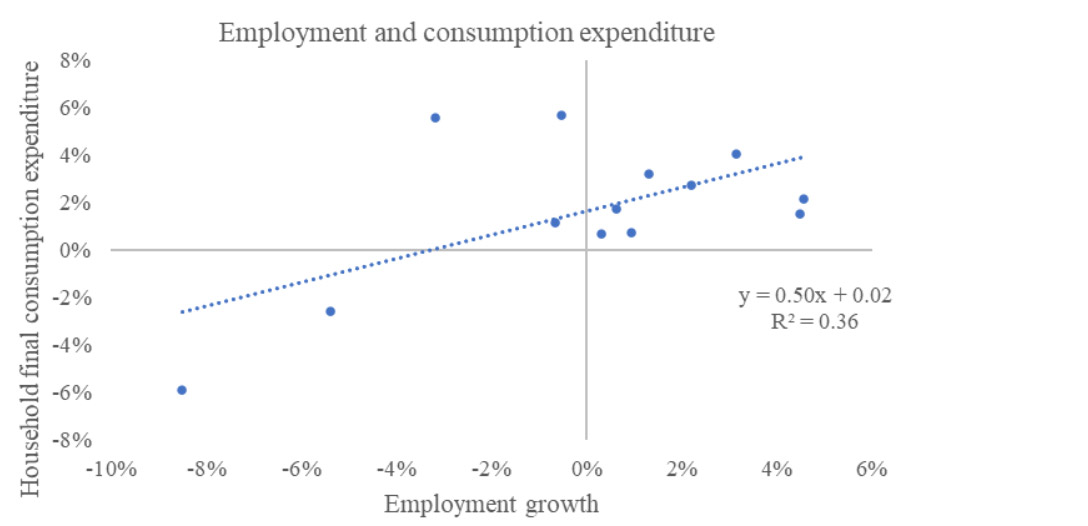

Our final point, illustrated by Chart 7 below, shows the relative impact of improved employment on household final consumption expenditure. Employment growth of around 3% is associated with household final consumption expenditure growth of around 3% too. This is an important point, given the relative impact of improved consumption expenditure on equity markets broadly. The consumer and consumption are central to economic activity, as well as for broad-based equity market performance; and for investors, consumption trends are important from an asset allocation perspective. Improved consumption expenditure is a net positive for company-specific performance (from a demand perspective) and thus equity market performance.

Chart 7: Employment and consumption expenditure

Date sampled: 28-Mar-23

Source: Investec Wealth & Investment, World Bank

So what would this hypothetical scenario mean for equity markets? The phrase “a rising tide lifts all boats” comes to mind. Like social grants, more money in the form of higher consumption expenditure from the pockets of consumers, is a net positive for companies across many sectors, in particular SA Inc stocks like retailers (expenditure) and banks (deposits, credit extension, collections). Improved earnings, earnings quality and earnings outlooks for SA Inc bode well for the JSE All Share when it comes to broad-based potential reratings. Our net exporting industries will also benefit from an improvement in our export capacity, namely agriculture and mining. South Africa currently screens as cheap when compared to other equity markets from a valuation perspective. Our base case catalyst for this hypothetical uplift is improved performance by Eskom and Transnet. Energy security is a central pillar of economic activity, and logistics is central to the movement and flow of goods and services. The knock-on effect of an improvement in the performance of Eskom and Transnet would be a net positive for a wide array of economic variables and metrics.

In summary, improved exports will result in a material improvement in GDP growth, which in turn will lead to better employment outcomes and ultimately higher household final consumption expenditure. This is a net positive for equities as incomes and thus demand is enhanced, positively impacting earnings.

Get Focus insights straight to your inbox

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Browse further in