Market and economic highlights:

- The SARB hiked interest rates by 50bps, in line with expectations. The currency response was surprising, with the rand depreciating against all major currencies. The weakness of the currency leads to upside risk to inflation forecasts in the near term and the SARB has increased its inflation estimate for 2023 to 6.2%, still above the central bank target range of between 3% and 6%. However, with producer price inflation easing (8.6% versus a previous 10.6%), the inflation outlook improved marginally.

- US debt-ceiling talks culminated in a bipartisan agreement in Congress, avoiding a potential first-ever default of the “risk-free” asset of financial markets. US government debt yields have fallen, although remain elevated as the Fed continues to push a hawkish message.

- UK inflation surprises on the upside. Inflation is receding across most of the globe and the UK is no exception. However, inflation is receding much more slowly than expected. April inflation came out at 8.7% vs the consensus forecast of 8.2%. Core inflation picked up to 6.8%, well above the prior reading at 6.2% and the consensus forecast of 6.2%.

- Earnings season came to an end in the US with a strong cohort of upside surprises, although they were down year-on-year. We analyse the earnings season below but note the following notable takeaways: operating margins are declining across the board from a year ago, except for communications services, which speaks to the weakening profitability outlook for corporates, particularly in the context of falling personal consumption expenditure and the increasing risk of recession.

Thematic view: Margins, PCE and recessions

In March we highlighted a few key themes about the previous earnings season. To recap:

- We explored how operating margins had been falling across all industries except energy, real estate and utilities.

- The operating margin percentiles were also falling from where they had been in the six previous months, when multiple industries were at peak operating margins.

- From a valuation perspective, the sectors that stood out were information technology (IT) and financials. This is based on their respective operating margins and 12-month forward price/earnings ratios (P/Es) relative to history, going back to Q1 2013. Cyclically high margins should come with cyclically low P/Es and that is broadly the case in the US. The most notable exceptions are IT (high multiple and high margins) and financials (low margins, low P/E).

So what themes stood out this time? Here are a few key points:

- Energy sector operating margins are now declining, primarily driven by falling energy commodity prices;

- Financials and discretionary retail sector operating margin contraction has become more pronounced due to an increasingly deteriorating macroeconomic environment in the US;

- Falling operating margins are closely linked to the performance of the S&P 500;

- Falling operating margins are also closely linked to personal consumption expenditure, which has, of late, been falling in the US. The after-effects of high-interest rates in the US are negative for the direction of personal consumption expenditure, which is thus a negative for stock market performance in the near term.

- Structurally higher operating margins should be met with structurally lower forward P/Es, but this is not the case for the S&P 500 and the Nikkei. The S&P 500 and the Nikkei screen as expensive when looking at 12-month forward P/Es and operating margins. The opposite is true for the JSE All Share, which screens cheap from a valuation perspective.

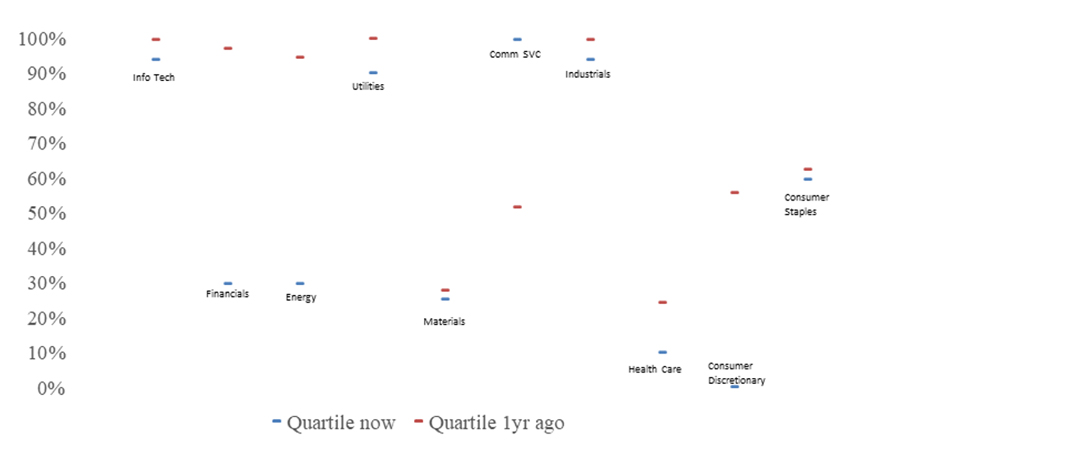

Sectoral operating margin trends

The chart below illustrates the percentile at which the various industries are in terms of operating margins relative to one year ago. The first important point is that operating margin contraction has been broad-based across sectors with the only exception being the communications services sector. The most significant contractions in operating margins have been in the financials, consumer discretionary and energy sectors. It is important to note that both energy and financials were at near-peak operating margins one year ago.

Operating margins trends on the S&P 500

Date sampled: 31 May 2023

Source: Bloomberg, Investec Wealth & Investment

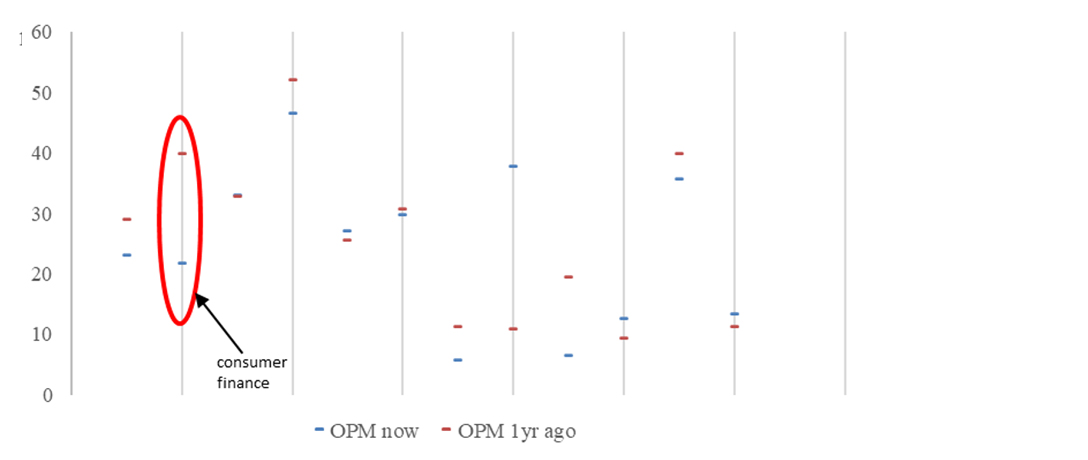

Financials: As a result of a combination of higher interest rates and the halting of monetary stimulus, financials have come under pressure. Within the financial sector, one of the most pronounced contractions in operating margins was in the consumer finance sub-sector, which declined around 45% last year. We highlight this sector specifically as a gauge/barometer of expectations of consumer financial conditions in the US. The steep contraction should be a cause for concern given that the primary driver could relate to higher credit-default provisions as a result of expectant increased consumer distress levels given the deteriorating country-specific and global macroeconomic outlooks.

S&P 500 Financials sub-sector OPM trends

Date sampled: 2 June 2023

Source: Investec Wealth & Investment, Bloomberg

Energy: Declining energy margins are the result of falling energy prices globally, which would impact pricing on the revenue line. The energy sector, and the underlying companies, are very sensitive to the price of Brent crude as shown below. Brent crude has fallen 40% over the last 12 months. The blockbuster performance seen in 2022 has normalised, and is trending towards historical averages, where energy profit margins were generally below the index average.

Macroeconomic views

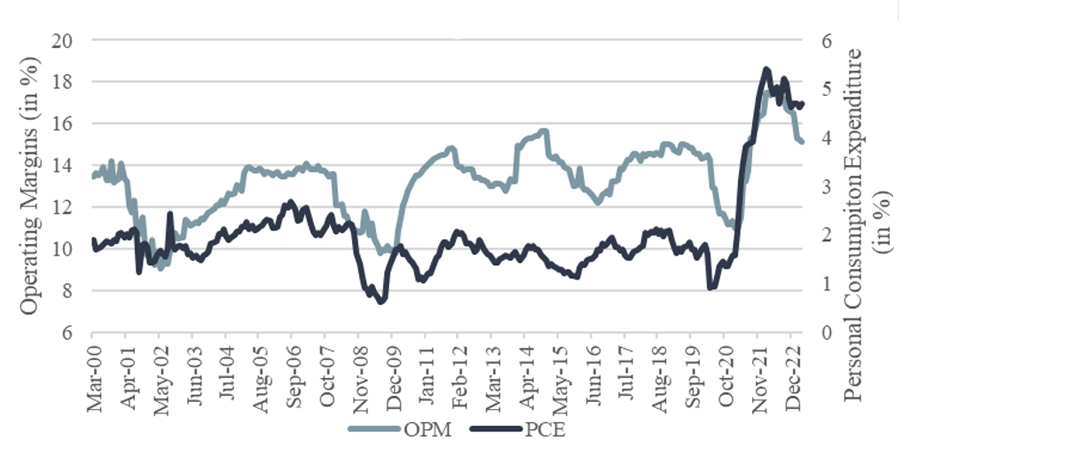

The chart below shows the relationship between US personal consumption expenditure (PCE) and operating margins of the S&P 500, which tend to move in the same direction. Similarly, there is a strong relationship between US PCE and the Federal funds rate. A rising Federal funds rate tends to negatively impact PCE due to the impact of higher interest rates on US consumer spending power. Therefore, with US interest rates at peak levels and market expectations of the US Fed only starting to cut rates from November onwards, this is a negative for PCE and therefore a negative for operating margin trends in the near term. Therefore, the degree of operating leverage in firms in the US would expectedly come under pressure because of the arising risks from falling PCE.

US Personal Consumption Expenditure vs S&P 500 Operating Margins

Date sampled: 1 June 2023

Source: Investec Wealth & Investment, Bloomberg

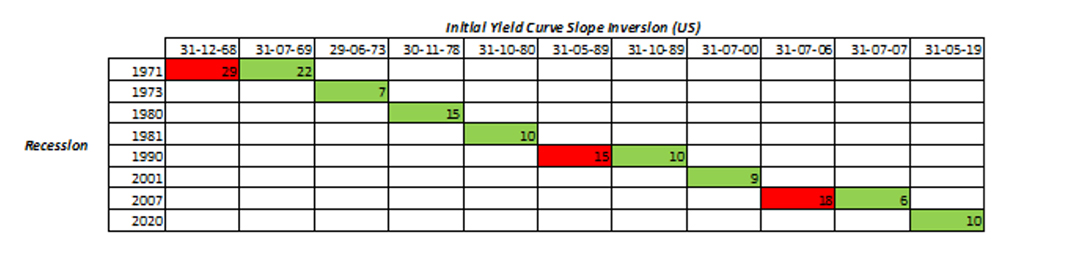

Based on previous work, there is an increasing risk of recession in the US. Broad market consensus is for a shallow recession. Several indicators are pointing towards a recession, notably:

- Yield curve inversion, which initially inverted in October (eight months ago). Typically, the yield curve inverts 11 months ahead of a recession.

Recession to Yield Curve Slope Inversion (US)

Date sampled: 4 May 2023

Source: Investec Wealth & Investment, Bloomberg

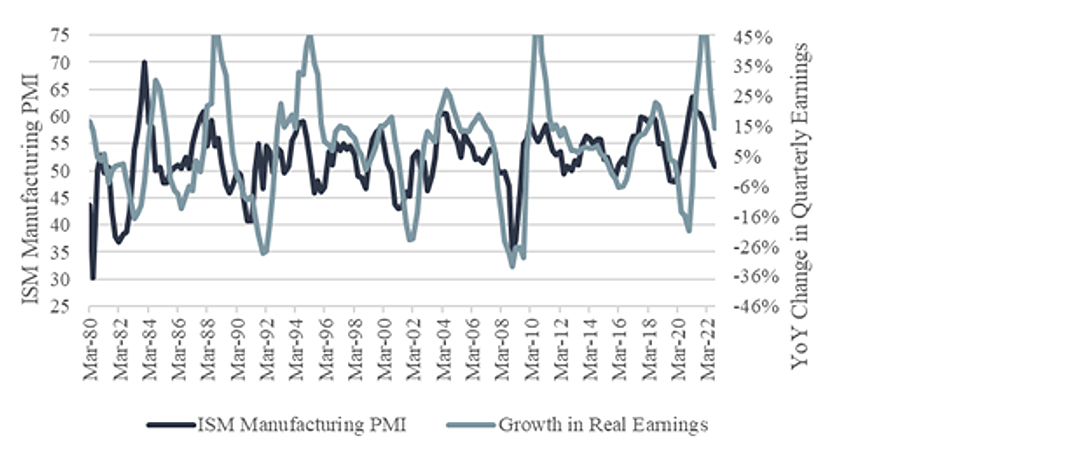

- Negative US ISM PMI data are also a strong indicator of an impending recession. Typically, US ISM PMI turns negative six months ahead of a recession, and it has been seven months now. US ISM PMI is also positively correlated with earnings, thus earnings should come under pressure.

ISM Manufacturing PMI vs Earnings

Date sampled: 6 June 2023

Source: Investec Wealth & Investment, Bloomberg

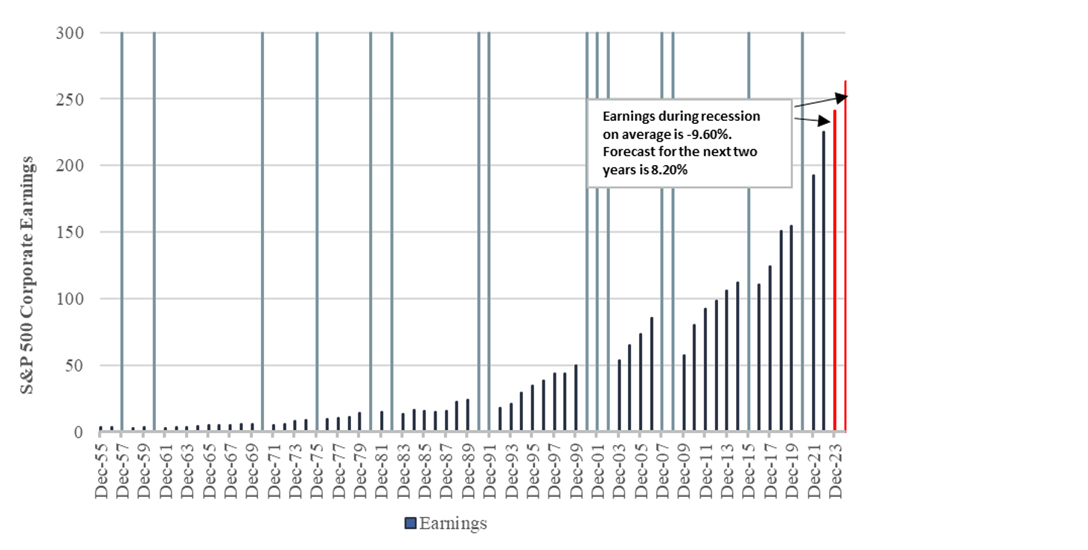

Given the macroeconomic risks, the threat of a recession in the US, falling personal consumption expenditure, operating margin compression and the subsequent impact on the performance of the S&P 500 overall, there is a material risk of earnings downgrades over the next year. We highlight that earnings growth expectations in the US remain elevated, at an average of 8.2% over the next two years, despite operating margin pressure and the threat of recession.

Earnings during recessions

Date sampled: 31 May 2023

Source: Investec Wealth & Investment, Bloomberg

Recessions and sectoral performance

The table below shows sectoral performance during recessions. We also highlight the sectors that are most and least at risk in terms of performance on a three-month, six-month and 12-month basis. On a six-to-12-month time horizon, there tends to be greater safety in consumer staples and health care sectors.

Across all time horizons there is pronounced risk in the financials and information technology sectors, whereas the pronounced risk on a 12-month basis is in utilities and telecommunications (telcos).

Telecommunications operating margins have not yet started to contract, but utilities have had the most pronounced margin contraction over the last six months.

Sectoral performance after actual onset of a recession

Date sampled: 31 May 2023

Source: Investec Wealth & Investment, Bloomberg

Given macroeconomic conditions and the defensive nature of consumer staples and health care, they screen cheap with a combination of low operating margins and historic upside performance during recessions.

Telcos screen expensive due to relative historical performance during recessions and what we have been seeing in the sector’s margin dynamics over the last year.

Financials and information technology screen as risk sectoral allocations given their relative performance during recessions and present operating margin dynamics.

Global valuation view

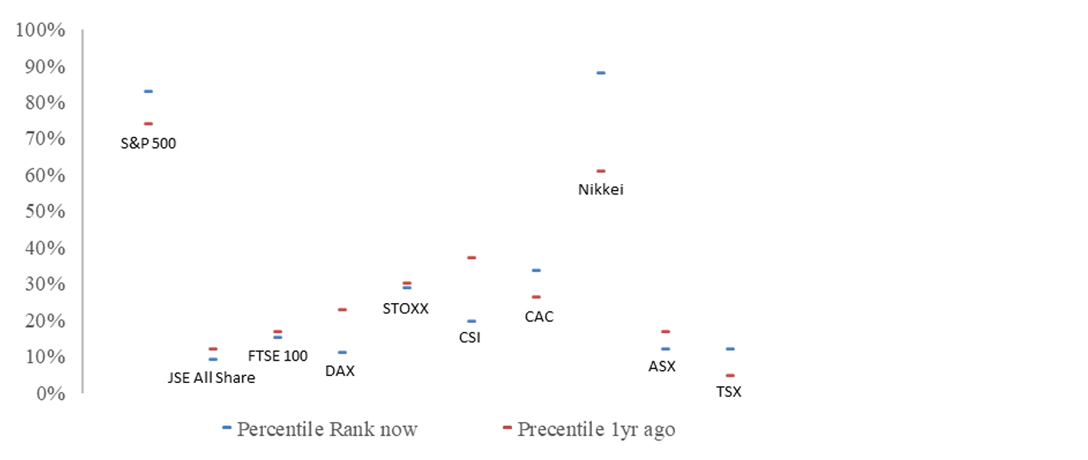

Broad-based forward P/E contraction can be seen across the major global indices.

12-month forward P/E's by country (percentile trend)

Date sampled: 1 June 2023

Source: Investec Wealth & Investment, Bloomberg

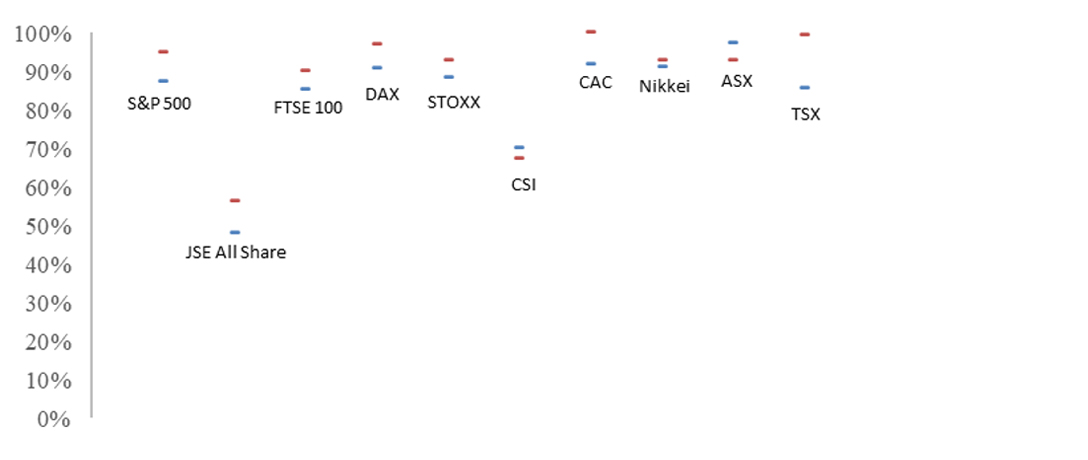

There has similarly been a broad-based operating margin contraction across major global indices.

Operating margins by Country (percentile trends)

Date sampled: 1 June 2023

Source: Investec Wealth & Investment, Bloomberg

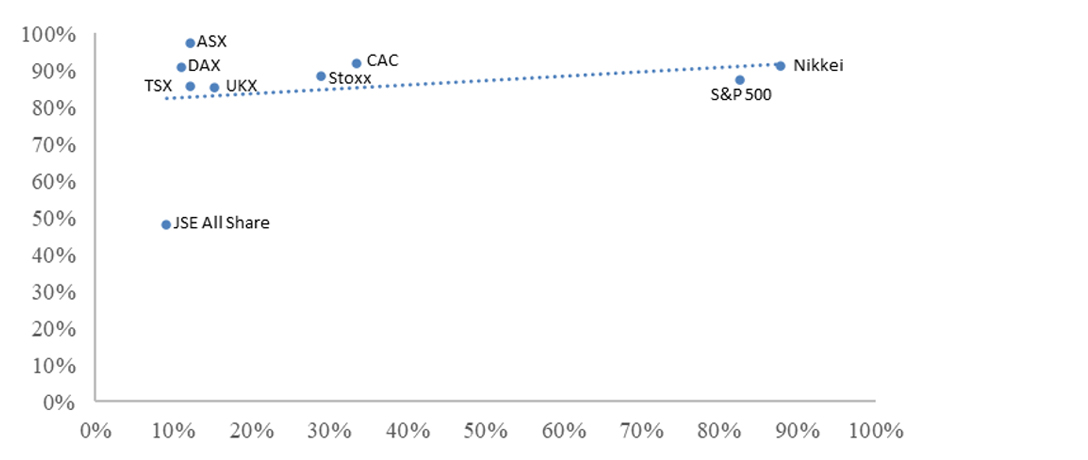

Structurally higher operating margins should be met with structurally lower forward P/Es, which is not the case for the S&P 500 and the Nikkei. The S&P 500 and the Nikkei screen as expensive when looking at 12-month forward P/Es and operating margins. The opposite is true for the JSE All Share, which screens cheap from a valuation perspective.

Percentile Ranks by country

Date sampled: 1 June 2023

Source: Investec Wealth & Investment, Bloomberg

Get Focus insights straight to your inbox

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and

families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give

you access to the world’s leading companies and fund managers.

Browse further in