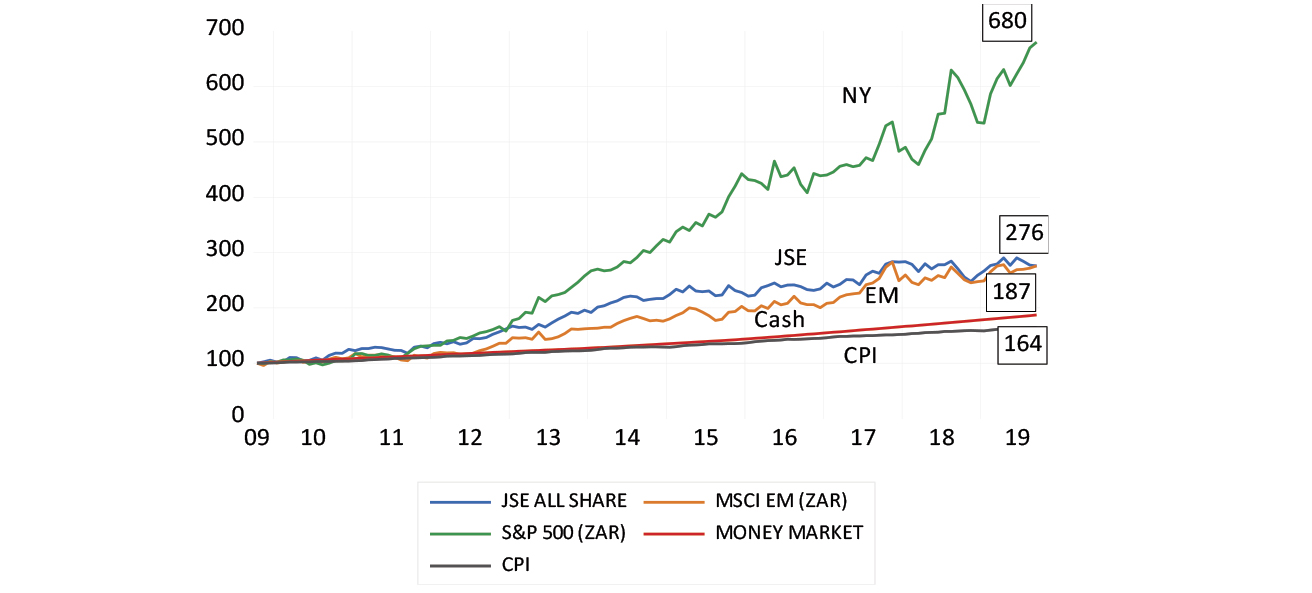

It’s been 10 years since the Global Financial Crisis. If you had invested R100 in October 2009 in the 500 companies that make up the leading equity index in the world (the S&P 500 Index), your investment would (as at the end of October 2019) be worth R680 on a total return basis (including dividends reinvested in the index). Returns over the period averaged over 18% a year in rands and 13.4% in US dollars.

Most other leading equity markets have not performed as well. For example, R100 invested in the JSE All Share Index or in the MSCI Emerging Market Index (EM), again with dividends reinvested, would now be worth about R276. This is equivalent to an average annual return of about 12% from the JSE and the EM benchmark over the 10 years.

To put this in context, an investment in the SA bond market 10 years ago would have guaranteed the rand investor 9% a year for 10 years. Equity market returns of 12% a year, therefore, did not fully compensate investors for taking on equity market risk over those 10 years – assuming a required equity market risk premium of 4% a year.

The strong outperformance of the S&P 500 began in 2013 and has continued since. This reflects very different fundamentals from those of the JSE and other markets. The S&P 500 delivered growth in index earnings per share in US dollars of 11.7% a year over the last 10 years. By contrast, the JSE delivered growth in index dollar earnings per share of only 1.46% a year and 5.5% in rands, over the same period, barely ahead of inflation.

Figure 1: S&P, JSE, EM and money market index values (2009=100)

Source: Bloomberg Investec Wealth and Investec Wealth & Investment

Back in September 2009, US Treasuries offered a guaranteed 3.4% a year for 10 years, a good yield by the standards of today. This meant that, at that especially fraught time, investors would have required an average return of about 7.5% a year to justify a full weight in equities, assuming the same required extra equity risk premium of 4% a year. The returns that were realised on the S&P, therefore, exceeded required returns by a substantial 6% a year.

Time has proved that the risks of financial failure in the US had been greatly exaggerated. The lower entry price for bearing equity risk 10 years ago, reflected by the index values of the time, proved unusually attractive.

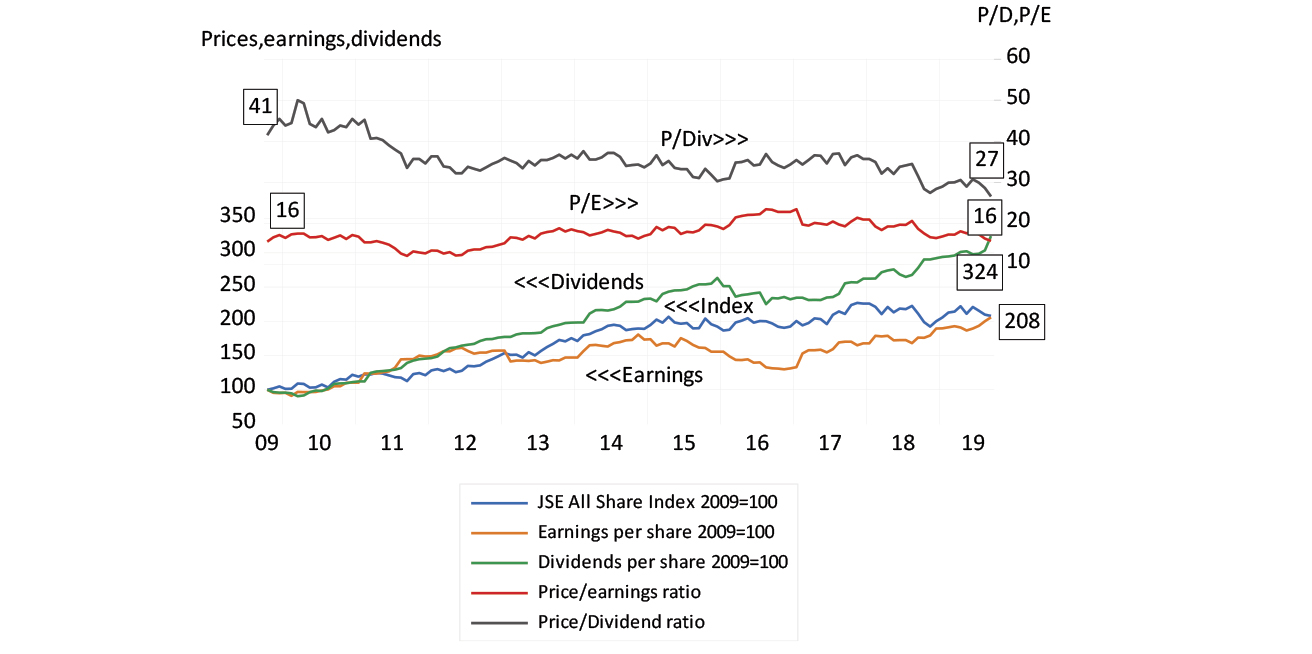

Dividends per JSE index share, by contrast, have grown from the equivalent of R100 in 2009 to R324 in September 2019, while earnings per share have no more than doubled. The ratio of the JSE Index to its dividends was 41 times in 2009; it is now, in 2019, only 27 times. In other words, the JSE All Share Index dividend yield is up from a 2.4% average in 2009 to 3.7% now.

In short, JSE-listed companies have decided to pay out more cash in the form of dividends. To a lesser extent, they have also been using the cash generated through their operations to buy back their shares in the marketplace, rather than to undertake capex, increase working capital, hire more workers or build inventory and work in progress.

What these reactions reveal is a lack of value-adding investment opportunities for JSE-listed companies. The willingness to pay out more in dividends, rather than to invest the cash (probably unprofitably) in their enterprises, reveals a degree of discipline in the use of shareholder capital. But it also reveals the constraints on their ability to grow their businesses in SA.

JSE earnings per share and their value have matched each other very closely. The ratio of the index to its trailing earnings per share was 16 times in 2009 – and is the same 16 times today.

By contrast to the rising trend in dividend payments and the reduction in the price to dividend ratio (increase in the dividend yield) for the JSE, JSE earnings per share and their value have matched each other very closely. The ratio of the index to its trailing earnings per share was 16 times in 2009 – and is the same 16 times today. There has been no derating or rerating for JSE reported earnings. Actual dividend payments are less highly appreciated than they were (see below).

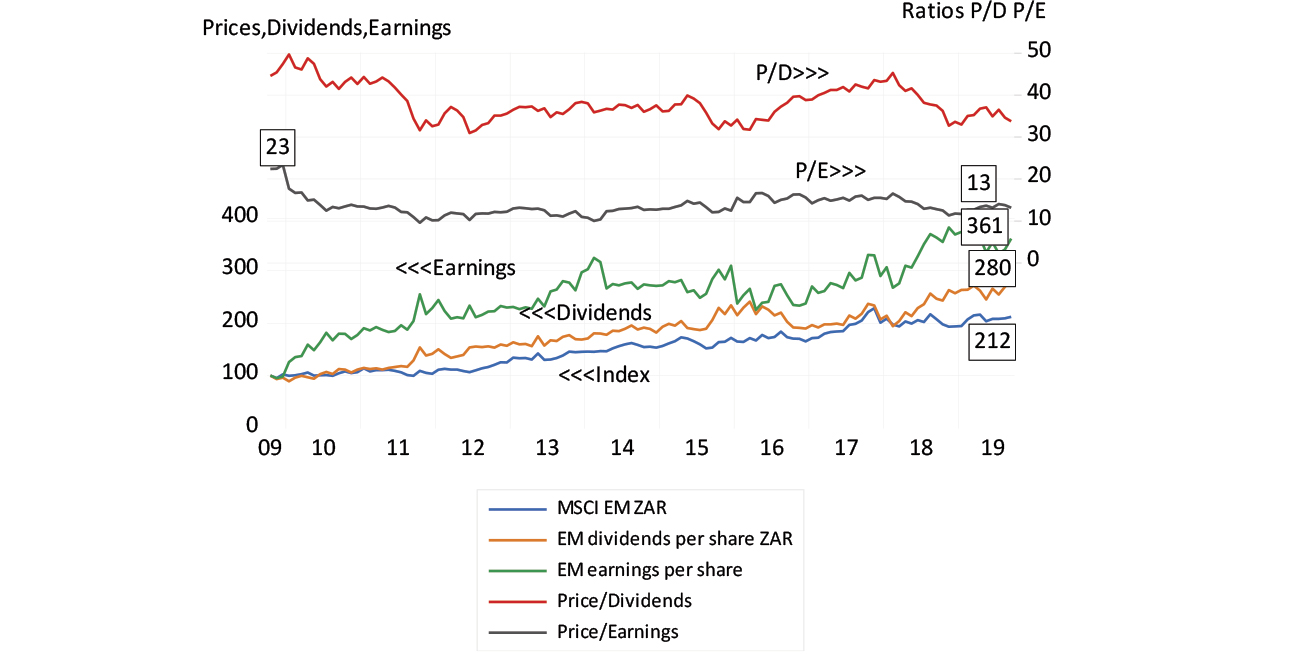

Also, by contrast, emerging market index earnings have grown faster than dividends. Index earnings have grown by 3.6 times since 2009 and Index dividends by 2.6 times. However, both price-to-dividend and price-to-earnings ratios have declined. The EM index now trades at only 13 times, trailing earnings compared to a much more optimistic 23 times in 2009. EM companies have on average clearly derated over the past 10 years.

Figure 2: The JSE All Share Index (2009-2019) – values, earnings, and dividends, as well as price-to-earnings and price-to-dividend ratios

Source: Bloomberg Investec Wealth and Investec Wealth & Investment

Figure 3: The MSCI Emerging Market Index (2009-2019) – values, earnings and dividends, as well as price-to-earnings and price-to-dividend ratios

Source: Bloomberg Investec Wealth and Investec Wealth & Investment

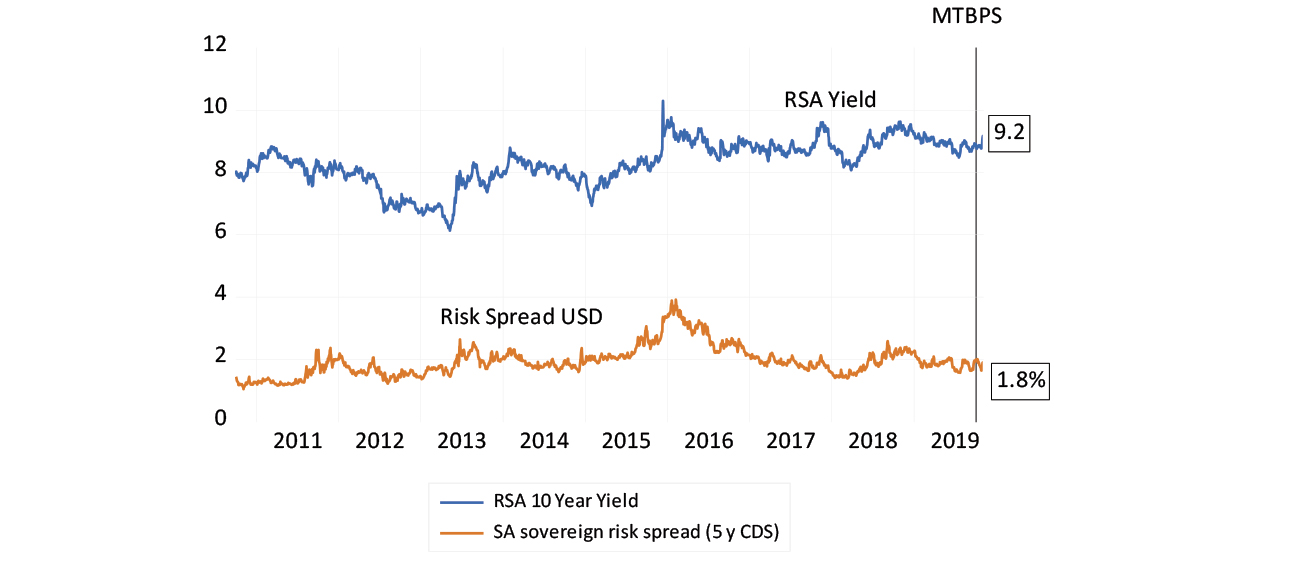

The equivalent required risk-adjusted return of the highly diversified S&P 500 Index today is a mere 5.8% a year on average. With long RSA bond yields now offering close to 9% a year, the required risk-adjusted return from the average company listed on the JSE is now at least 13% a year.

It has become increasingly difficult for an SA-based company to add value for shareholders by earning returns on its capital expenditure of over 14% a year, given slow growth and low inflation. SA business has responded accordingly, by saving and investing less and paying out dividends at a much faster rate.

This is not good news for business or the economy. JSE-listed companies would be much more valuable if they could justify investing proportionately more and paying out less, as US companies have done.

South African companies need encouragement from faster growth in their revenues and earnings and lower interest rates. Lower short-term interest rates are in the power of the Reserve Bank and if they were to be reduced it would help stimulate extra spending by households.

Lower inflation expectations (and consequently lower interest rates) means a growing belief that SA will not fall into a debt trap and resort to printing money to escape it.

SA business and the local share market also need the encouragement of lower required long-term returns. In other words, lower expectations of longer-term inflation would bring down long-term interest rates. Lower inflation expectations (and consequently lower interest rates) means a growing belief that SA will not fall into a debt trap and resort to printing money to escape it – a move that would be highly inflationary.

So far, and after the Medium Term Budget Policy Statement of October 2019, not obviously so good. The jury remains very much out and the cost of capital is still highly elevated.

Figure 4: RSA long-term interest rates and sovereign risk spread

Source: Bloomberg Investec Wealth and Investec Wealth & Investment

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Investec products you may be interested in

Wealth Management

Portfolio Management

Offshore Investments

Wealth Management

Portfolio Management

Offshore Investments

Browse further in