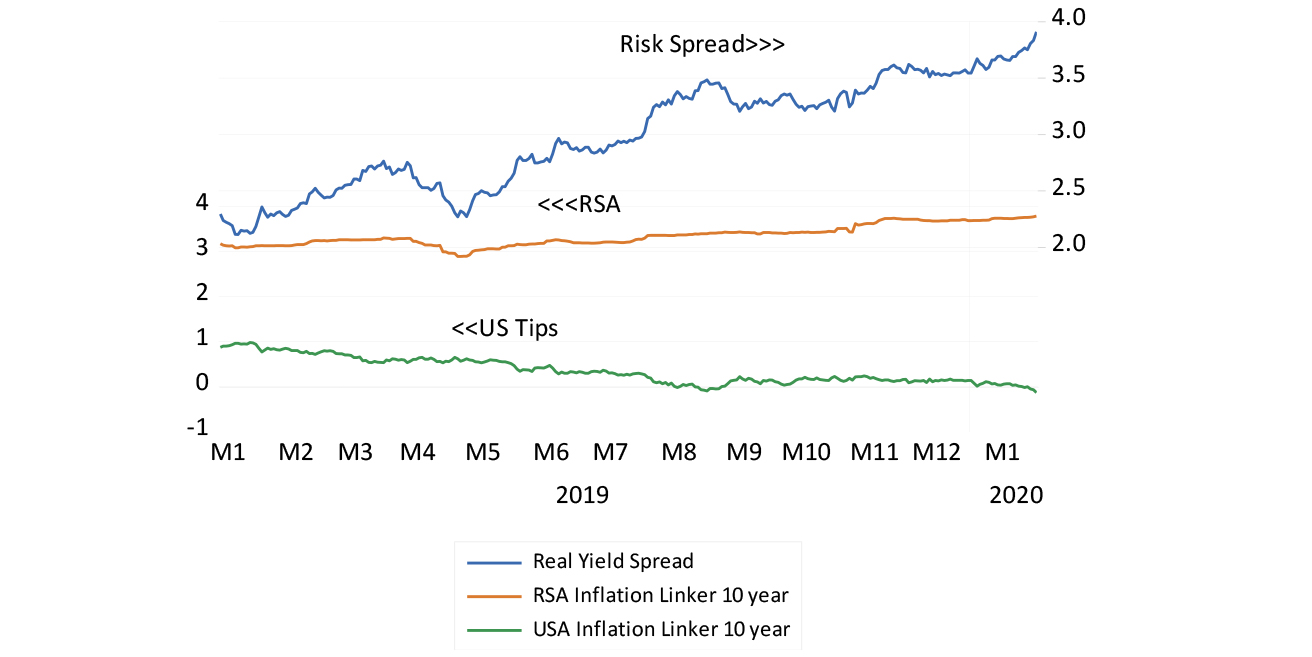

The SA government is currently offering bondholders a real 3.8% a year yield for 10-year money. This is the lowest risk investment that can be made in rands over the next 10 years, one made without the risk of inflation reducing the purchasing power of your interest income and without risk of default.

However, if you wished to invest for 10 years in a US Treasury inflation-protected security (a 10-year TIPS) you would have to pay Uncle Sam 13.3 US cents per US$100 invested for the opportunity.

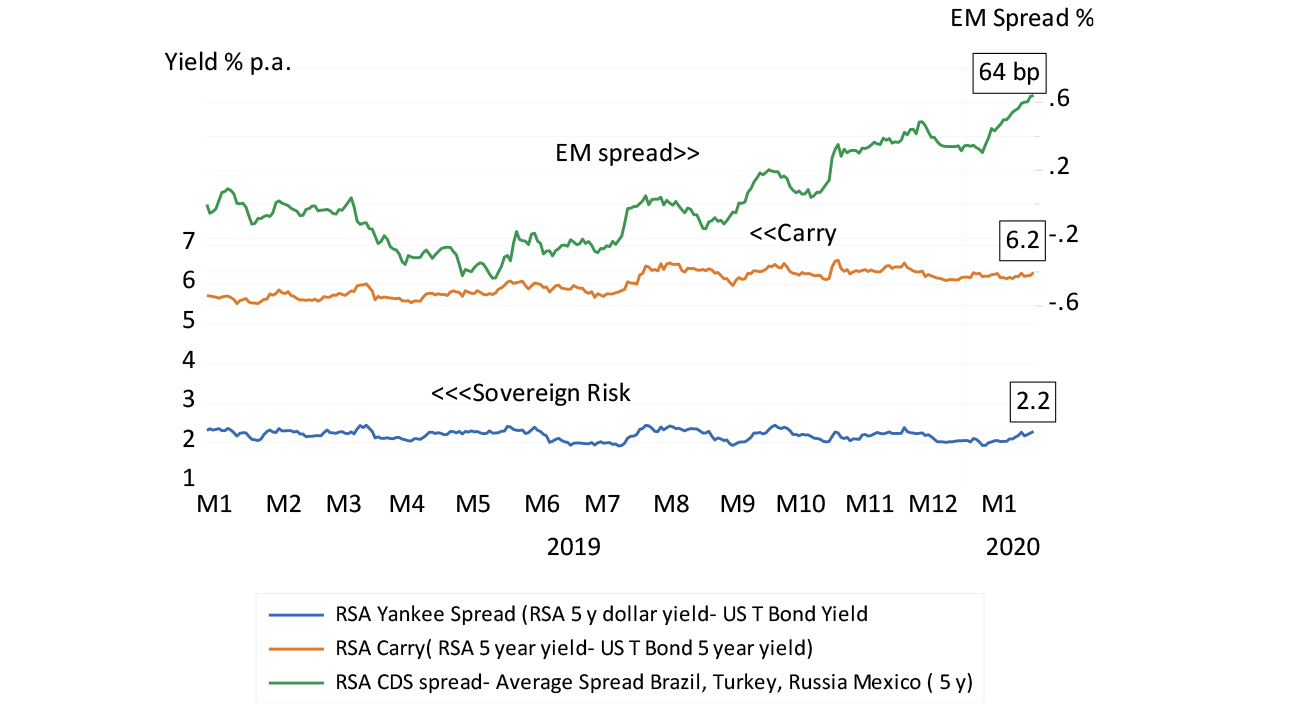

Thus investors willing to accept SA sovereign risk are currently being compensated with an extra 4% in real rand income, each year, for the next 10 years. This real risk spread was a mere 2.3% a year ago. Other possible measures of SA risk are as unflattering. When the SA government borrows US dollars for five years, it has to pay an extra 2.2% more a year than the US Treasury for five-year money, placing SA sovereign debt in the realm of junk status, where it has languished for some time. The rating compared to other emerging market borrowers has deteriorated and the rand is expected to weaken at a faster rate.

The real risk spread for SA assets

Source: Bloomberg and Investec Wealth & Investment

Measures of SA risk

Source: Bloomberg and Investec Wealth & Investment

It all makes for expensive national debt that taxpayers have to fund, as well as higher costs of capital for SA business. These higher real rates also raise the returns that SA businesses have to hurdle over to justify capital expenditure. This, even as fewer such opportunities are seen to be on offer.

The best many SA economy-facing businesses can now do for their share owners for now is to opt out of the race in ways that are not good for growth. That is to use the cash they generate to buy back shares or pay dividends rather than attempt to grow their businesses.

The 2020-21 Budget has to cover an extra R50bn to hold the fiscal line, drawn as recently as last October

The cause of this deteriorating credit rating and the higher discount rates applied to SA earnings is obvious enough – the government’s management of the fiscus. The 2020-21 Budget has to cover an extra R50bn to hold the fiscal line, drawn as recently as last October. It is the result of revenue coming in at lower-than-expected levels, as growth has slowed, as well as rapidly growing government expenditure on failed state-owned enterprises (SOEs).

A growing interest rate bill on ever more government debt is a further growing strain on the Budget.

There are however alternatives to raising taxes or borrowing more. One solution that has been suggested is to access SA pension and retirement funds. In practice, this would mean compelling retirement funds to hold more SA government debt of one kind or another, on less favourable terms than have previously been provided.

Such a measure would have one major advantage for the politicians imposing them: their full consequences will not become obvious for many years. These consequences would be in the form of lower than otherwise returns for pension funds and depleted pension payments, as well as the bill ultimately to be presented to taxpayers for underfunded defined benefits owed to public sector employees (largely incalculable today).

A better approach would be to swap most of the debts and interest payments of SOEs for equity. The one major potential upside of this approach is that it could mean the effective transfer of ownership and rights of ownership from the government to the private sector. This would bring greater efficiency and the avoidance of further losses for SA taxpayers and consumers of essential services. Such a step would bring down real interest rates and encourage private sector investment.

It would moreover indicate something much more fundamental to investors in SA. That is, when accompanied by credible controls on the size of the government payroll, it would signal something all-important for investors – that is the primary purpose of the SA government is not to provide a growing flow of real benefits for those employed by the government. This is the essential question that the Budget, we must just hope, will answer in the affirmative.

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Get Focus insights straight to your inbox

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

Browse further in