Sometimes you hit the jackpot holding onto shares in what becomes a hugely successful company. Taking an early profit will not make you broke but can be wealth-destroying. Yet buying and holding forever may make your much-enhanced wealth highly concentrated. Diversifying your risk, and selling down the huge outperformers to hold a mix of shares and other assets makes wise, risk-reducing, sense.

Owners of start-up businesses that have made them fabulously wealthy also have to make choices about how best to deploy their wealth. They could diversify their wealth by redeploying dividends and other income received from the original enterprise. By investing in a portfolio of other assets, in a variety of jurisdictions, they reduce their risk. Alternatively, they could adapt the company they control to acquire a well-diversified group of unrelated businesses they continue to exercise management control over.

This is what the Rupert family has done well. They have diversified their wealth away from cigarettes in South Africa by establishing investment holding companies that invest in unrelated businesses in South Africa and abroad that they maintain their holdings in and maintain management control of. And most impressively, by managing the exceptional growth of Richemont (CFR) a stand-alone Swiss-based luxury goods company.

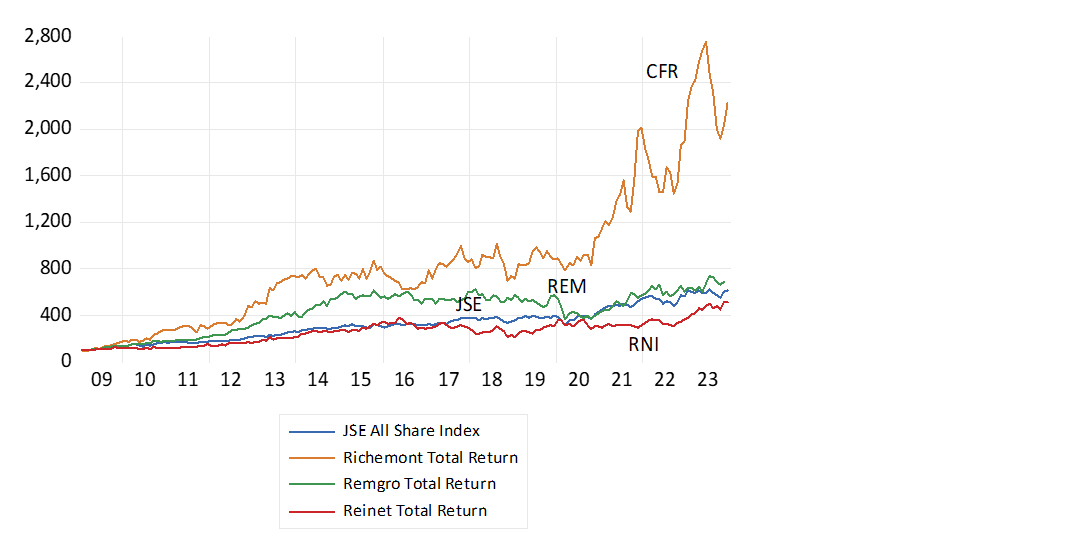

Richemont in 2007 fully divested itself from exposure to tobacco and became a specialised luxury goods company. R100 invested in the stock in 2009 with dividends reinvested had grown to R2200 by late 2023. This is equivalent to an average rate of return of 21%, helped by a marked acceleration in its share price after the Covid-19 pandemic. Investing R100 in the JSE All Share Index, also reinvesting the dividends received, would have grown to only R605 over the same period, at an average 12% a year return.

The performance of Richemont in US dollars is also very impressive. US$100 invested in the company in 2009 would have grown to US$1239 by late 2023. Investing the same US$100 in the S&P 500 Index would now be worth approximately US$773. Johan Rupert is justified in proudly pointing this out to South African fund managers who have not availed themselves of the opportunity.

Fund managers however have been justifiably critical of the performance of two other JSE-listed vehicles used to diversify the Rupert family wealth. Remgro has performed in line with the JSE since 2009 with significantly more volatility while Reinet has delivered below JSE averages, also with more volatility.

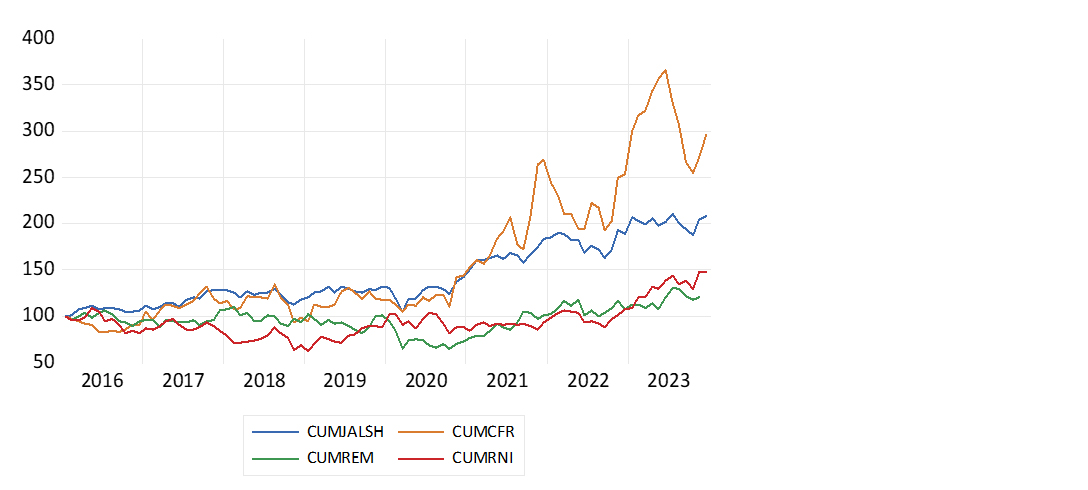

Moreover, the share market performance of the Rupert-managed companies has been much less impressive if we start the comparisons later. Remgro and Reinet have returned only an average of 1.67% and 5.4% a year respectively since 2016 and Richemont has delivered average returns of 14% a year since then, helped by a post-pandemic surge. The JSE All Share index has returned an average 8.4% return since January 2016.

Remgro and Reinet have thus served no useful purpose to loyal outside shareholders in recent years and even Richemont looks less impressive when compared with its peers, particularly LVMH. As we all should know, you are only as good as your last performance.

JSE All Share (JSE), Richemont (CFR) Remgro (REM) Reinet (RNI), cumulative returns (2009=100)

Source: Iress and Investec Wealth & Investment, 12/01/2024

JSE All Share (JSE), Richemont (CFR) Remgro (REM) Reinet (RNI), cumulative returns (2016=100)

Source: Iress and Investec Wealth & Investment, 12/01/2024

The difference between book and market value and their implications

Because the reported book or net asset values (NAV) of Remgro and Reinet are higher by a large margin than their share market values, Remgro and Reinet would seemingly be worth more to these outside shareholders if these companies were wound up and the assets, including the shares held in listed and unlisted subsidiaries, distributed (unbundled) to shareholders who pay management fees for the opportunity.

Yet such a presumption needs qualification. The value uplift, eliminating the difference between reported value and market value, and so eliminating the discount attached to the assets held by the holding company on their shareholder’s behalf, would be true of the listed shares held by Remgro and Reinet. Whether the unlisted assets held by the holding companies would also fetch their reported NAV is however not at all obvious. They might be too generously valued by the directors in their financial statements. In that case, the NAV would be artificially high, making for a larger and exaggerated difference in market value and a larger discount. Markets may simply not believe management’s valuations.

The market value of Remgro has been dragged down by a lacklustre investment programme achieving returns far below the cost of capital. Much Remgro capital was wasted in 2016 expanding one of its major subsidiary companies, Mediclinic, making a GBP600 million investment in a Dubai-based hospital group. Remgro’s recent decision to delist its Mediclinic investment, to take what has been a very expensive asset private, out of the direct sight of the market, cannot be market value adding. The value assigned to Mediclinic on the books of Remgro by its directors is now unlikely to be closely market-related. And if generously valued by the directors, it will add to NAV – but not market value – and raise the discount. It is the opposite of unbundling.

Were the investment programmes of Remgro or Reinet to be regarded as more promising, their market values would increase. Making Remgro or Reinet better businesses, and better asset allocators, as Rupert intends, would be market value-adding and in the interest of all shareholders. He “just” needs to convince investors that he can make better investment decisions and execute the plans that will enhance their internal rates of return. Measuring internal rates of return on extra capital invested by the Rupert-controlled companies will be the focus of outside investors and managers and should be the only basis upon which managers are rewarded.

The current market value of any holding company would also rise in anticipation of unbundling exercises, which is an exercise in the partial liquidation of holding company assets. The market value of the holding companies would decline with any actual unbundling that would also simultaneously reduce NAV and market value. But the direction of the discount itself, after an unbundling, the difference between NAV and market value, would depend upon the ongoing actions expected of the holding companies. Including expectations of further unbundling exercises or share buybacks and the quality of its investment agenda as continuously assessed.

A share buyback, another way to return assets, in this case cash, to shareholders, might also add market value to a holding company while reducing NAV. It could make sense not because the share appears cheap. The share price and market value should be presumed to be efficiently market-determined, if the shares are well traded, and are as likely to go up or down. Buybacks make value-adding sense if the holding company is unable to find the cost of capital-beating investments or acquisitions with its surplus cash. Such disciplined action would likely be appreciated and add market value and narrow the discount to NAV.

For a closely controlled holding company, attracting public money has its advantages. In addition to the additional fee income that comes with a larger, better diversified balance sheet it improves the ability to do hopefully larger wealth-adding deals. It also has its downside. That is having to accept the harsh, but what should always be recognized as the objective, judgment of the marketplace, about future performance. A judgment about prospects, not past performance, is best reflected in share prices. Adding NAV – as estimated in the books of a company – that realise below the opportunity-cost-of-capital returns, may prove an expensive exercise that reduces market value and widens the discount. This is especially true for investment managers who have every opportunity to construct well-diversified portfolios on their own.

*This article was written in collaboration with David Holland, co-founder of Fractal Value Advisors

Receive Focus insights straight to your inbox

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Offshore investments

Global Investment Strategy Group

Portfolio Management

Offshore investments

Global Investment Strategy Group

Portfolio Management

Browse further in