23 Jan 2016

Why South Africa needs to ‘save itself’

Most of us are aware of the sad state of our national savings in South Africa (SA), which has been in a state of steady decline over the last two decades. However, the important role that savings plays in the country’s sustained economic growth has not always been appreciated.

Receive Focus insights straight to your inbox

To understand the role that savings plays, one first has to understand what we are trying to achieve from an economic growth perspective. Elevated economic growth, ranging between 5% and 5.5% gross domestic product (GDP) growth, has been a theme in SA’s policy proposals for the last two decades, including the most recent National Development Plan outlining SA’s long-term socio-economic development roadmap to 2013.

To date, SA has fallen consistently short of these targets. Looking outwards, SA’s international competitiveness has also declined. If we consider per capita income growth adjusted for purchasing power, SA’s income growth rate lags behind other emerging markets such as the BRICs and the more-recently flagged MINTs. Another indicator of lagging competitiveness is SA’s share of the world export market, which shows a steady structural decline over the last 40 years.

The next important principle in understanding the role savings plays in achieving these targets is the relationship between savings and investment and the importance of an investment-led economy.

According to leading economists, the greatest constraint to SA’s economic growth and employment creation is the economy’s low investment rate. Economic research clearly shows that, in the long run, economic growth of advanced and emerging economies is largely determined by investment spending.

Some of the other constraints to inclusive economic growth include low skills levels, poor quality of education, high levels of industrial concentration and low levels of product market competition.

Looking at the current composition of SA’s GDP, it is clear that our growth to date has been led by consumption and government spending rather than sustained investment growth. In the last two decades, nine-tenths of SA’s average GDP growth of 3.1% has been a result of growth in consumption spending and growth in government spending, and only around one-tenth can be attributed to growth in investment spending and growth in export demand.

Understanding the importance of investment spending to fuel sustainable economic growth, leads one to the next question. How is this investment funded? Economic theory dictates that there is only one way in which investment can be funded, namely saving. This can be either domestic saving or savings by foreigners.

Research conducted by the Commission of Growth and Development in the 2008 study titled The Growth Report: Strategies for Sustained Growth and Inclusive Development, which examined the experiences of 13 ‘economic miracles’ found that:

“There is no case of a sustained, high investment path not backed up by high domestic savings”.

The Commission found that the overall investment rate equal to 25% of GDP or higher was required to achieve and sustain high growth. The Commission also found that foreign portfolio capital flows can support economic growth but if it is higher than 1% of GDP, it corresponds with stalled economic growth.

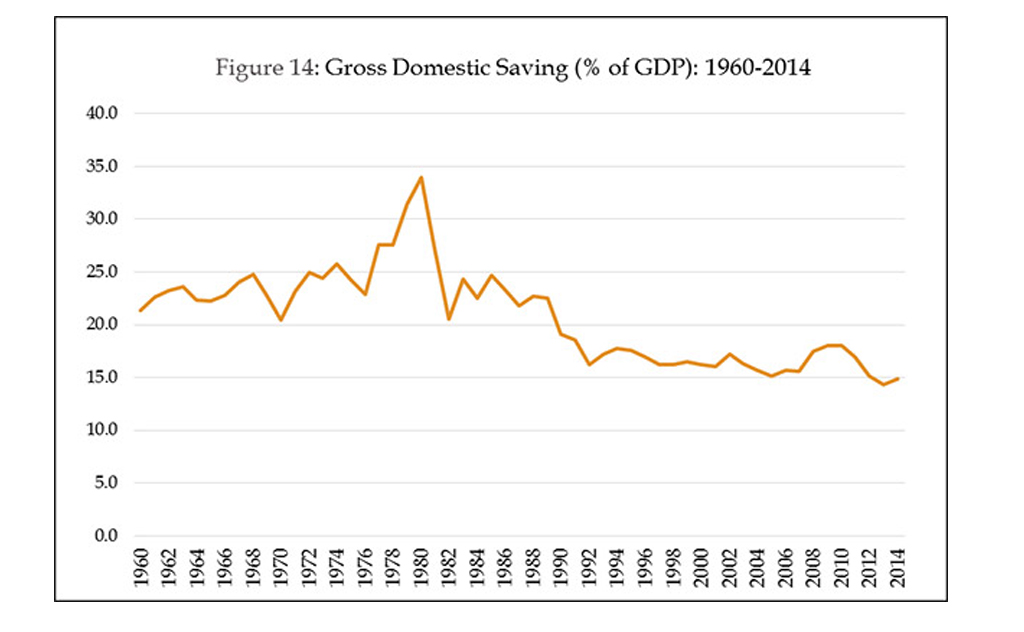

This points to the need for SA to fuel investment growth with domestic savings. As intimated above, and upon closer inspection, SA’s domestic savings rates have declined steadily over the last 50 years from an average of 24% of GDP between 1960 and 1990 to 16.5% from 1991 to 2014.

Source: Thulani Madinginye (2015); data derived from South African Reserve Bank (2015)

SA’s investment rate for the last decade of 19.4% has resulted in a savings-investment gap of 3.4% over the period, which has manifested itself by way of an ongoing current account deficit.

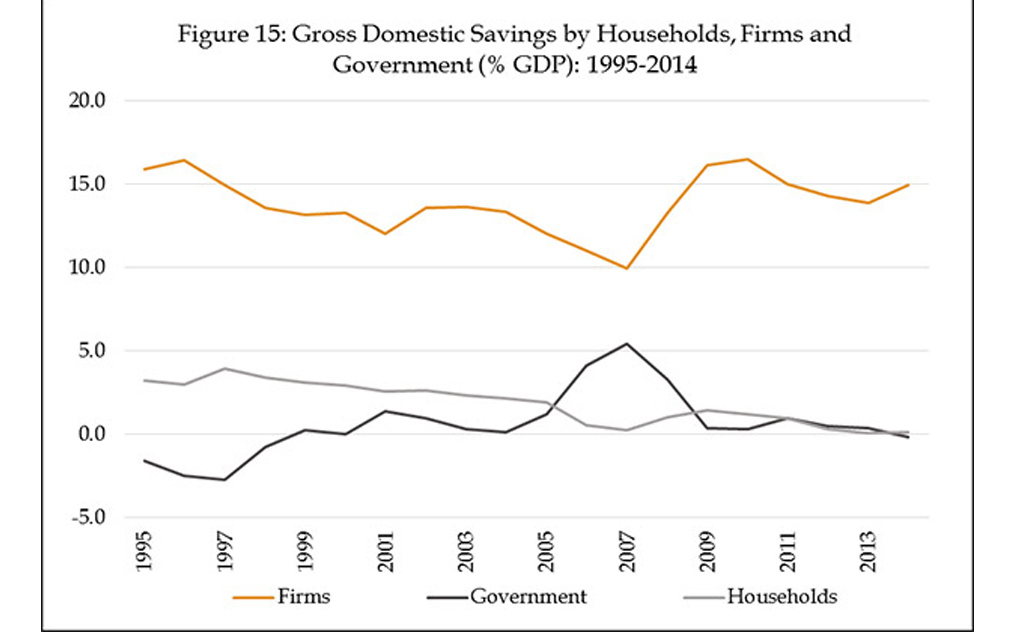

Further, in looking at the components of saving, namely household savings, corporate savings, and government savings, it is apparent that corporates are the only significant contributors to the national savings, with government and households in negative territory or showing negligible contributions.

Source: Adrian Saville, Citadel and GIBS (2015); data derived from South African Reserve Bank (2015)

Although investment and savings have proven pivotal to achieving economic growth, it has received little attention to date, with most of the focus tending towards socio-economic challenges.

Research conducted by the Gordon Institute of Business Science and Investec indicates that the low domestic savings rate needs to be almost doubled from current levels of 16.3% (average over the last two decades) to 28.3% to achieve the investment rate that is required to fuel SA’s ambition of elevated and inclusive economic growth.

In addition, in the World Bank’s recent Economic Update for South Africa titled Jobs and South Africa’s changing demographics, further credibility is given to the pivotal role savings plays as the findings conclude that:

“By creating a virtuous circle of job-intensive growth, improved productivity and educational attainment, and higher savings, growth could accelerate to 5.4% a year and per capita incomes could double by 2030…”

Most of the attention the savings topic has received has been at a micro level, focused on incentives to encourage household and goal-based savings, and the research has mostly consisted of opinion polls and surveys that have tried to identify savings trends.

It is clear that the topic requires further scrutiny, particularly to understand the real facts behind the consistent structural decline of our national savings rate over the last two decades and how we can influence the environmental factors to make a positive change in this regard.

The desperate state of our national savings demands greater focus if we want to achieve the ambitious GDP growth goals set out by the NDP. The IMF recently lowered its forecast of SA’s GDP growth to 1.3%, with Investec’s projections of 1.7% GDP growth and 2% fixed investment growth for 2016.

About the author

Patrick Lawlor

Editor

Patrick writes and edits content for Investec Wealth & Investment, and Corporate and Institutional Banking, including editing the Daily View, Monthly View, and One Magazine - an online publication for Investec's Wealth clients. Patrick was a financial journalist for many years for publications such as Financial Mail, Finweek, and Business Report. He holds a BA and a PDM (Bus.Admin.) both from Wits University.

Get the most out of your hard-earned cash

Cash investments for business

Corporate Cash Manager

Savings accounts for individuals

Cash investments for business

Corporate Cash Manager

Savings accounts for individuals

More articles in