The suitability of your current investments is often an afterthought when you or your family members are living and working abroad, that is when you or your family cease your South African tax residency. But it can have a major impact on the value of your investment.

For example, a popular vehicle for investing is through an endowment policy (colloquially known as a “wrapper”). But, as we discuss below, this may not be the most tax efficient investment if you or your family are non-SA tax residents.

Benefits of an endowment policy for SA tax residents

If you are an SA tax resident and your marginal income tax rate is higher than 30%, an endowment policy can be beneficial to you, because the insurance company is liable for the South African tax during the investment term, at a rate of 30% on income and an effective rate of 12% on capital gains. You as the policyholder (or the beneficiary if paid out on death of the life assured) will therefore receive the proceeds from the policy net of tax and fees and free of tax compliance in South Africa.

Another benefit is that the pay-out to the named beneficiaries on death of the life assured is outside the deceased administration process (i.e. it pays out directly to the beneficiaries and does not form part of the estate winding up process). This makes an endowment policy, in some circumstances, a nice liquidity tool for your beneficiaries on death.

As an SA resident, you should note that the policy and/or proceeds paid out from the policy on maturity will still form part of your estate from an estate duty perspective, unless your spouse is nominated.

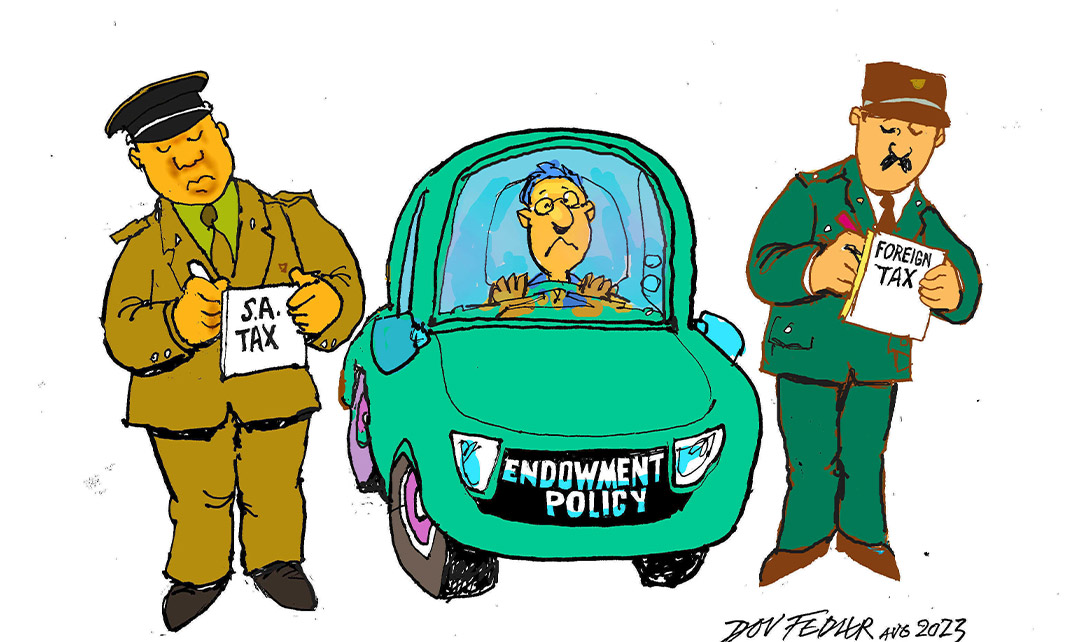

What happens if the policyholder or beneficiary is a non-SA tax resident?

It’s here where things get complex. In general, regardless of whether the policyholder or beneficiary is an SA tax resident or not, the insurance company will be subject to tax in South Africa.

However, in addition to the aforementioned tax payable by the insurance company, the non-SA tax resident policyholder or beneficiary may also be liable for tax in the new country of residence. For example, the US, UK, Portugal and Australia will (in some way and/or under certain circumstances) tax the policyholder.

This may lead to double taxation because of the mismatch in taxpayers. In other words, the insurance company will be liable for tax in South Africa and the non-resident policyholder or beneficiary may be liable for tax in the new country of residence.

Conclusion

Each country has its own rules and legislation, when dealing with the tax consequences of endowment policies/wrappers. Therefore, it is critical that specific in country tax advice is sought. Furthermore, it is always important to consider the suitability of an investment from a tax efficiency perspective before you or your family cease to be an SA tax resident.

Receive Focus insights straight to your inbox

Disclaimer

Although information has been obtained from sources believed to be reliable, Investec Wealth & Investment International (Pty) Ltd or its affiliates and/or subsidiaries (collectively “W&I”) does not warrant its completeness or accuracy. Opinions and estimates represent W&I’s view at the time of going to print and are subject to change without notice. Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issue without taking financial, banking, investment or other professional advice. W&I and/or its employees may hold a position in any securities or financial instruments mentioned herein. The information contained in this document does not constitute an offer or solicitation of investment, financial or banking services by W&I . W&I accepts no liability for any loss or damage of whatsoever nature including, but not limited to, loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss howsoever arising whether in negligence or for breach of contract or other duty as a result of use of the or reliance on the information contained in this document, whether authorised or not. W&I does not make representation that the information provided is appropriate for use in all jurisdictions or by all investors or other potential clients who are therefore responsible for compliance with their applicable local laws and regulations. This document may not be reproduced in whole or in part or copies circulated without the prior written consent of W&I.

Investec Wealth & Investment International (Pty) Ltd, registration number 1972/008905/07. A member of the JSE Equity, Equity Derivatives, Currency Derivatives, Bond Derivatives and Interest Rate Derivatives Markets. An authorised financial services provider, license number 15886. A registered credit provider, registration number NCRCP262.

Investec products you may be interested in

Offshore investments

Global Investment Strategy Group

Portfolio Management

Offshore investments

Global Investment Strategy Group

Portfolio Management

Browse further in