Hope for economic sunshine, a risk of an Indian monsoon

While global economic prospects remain resilient amid the rollout of Covid-19 vaccines and falling infection rates, new variants have reminded the world of the threat they pose to the recovery. We have trimmed our growth estimates for China and Japan in our latest Global Economic Overview, but have raised our forecasts for the UK, Europe and the pound.

Despite the recent decline in daily infections, the biggest risk to the global recovery remains the evolution of the Covid-19 pandemic. The rapid spread of the B.1.617 lineage, first detected in India, illustrates the threat that new variants of Covid can pose and how vital an extensive global vaccination campaign is to tackle the virus. Reflecting on these concerns, we have opted to maintain our global economic growth forecast at 6.2% in 2021, with slight downgrades to China and Japan offset by upgrades to the UK and the Eurozone. For 2022, we have uplifted our forecast by 0.1 percentage point to 4.8%.

Ongoing progress on vaccinations, at least for now, leaves gross domestic product (GDP) on track for strong growth in 2021; our forecast of 6.9% is unchanged. Instead, the attention of financial markets has centred on inflation, spooked by a 39-year high in monthly price growth on the core Consumer Price Index (CPI) measure. Beyond some temporary supply and demand mismatches causing immediate bottlenecks, we doubt the labour market will be strong enough for some time to come to generate sustained price pressures. In any case, the Federal Reserve will also have to determine and communicate how long and how much of an inflation overshoot relative to its target it is willing to tolerate under its new policy strategy.

Vaccinations got off to a slow start in the euro area, but the situation hasimproved through the course of this year, contributing to lower infectionrates and consequently the gradual lifting of social restrictions. That bodes well for the economy, with several indicators pointing to a pick-up in activity. Our forecasts envisage the second quarter marking the start of a sustainable recovery, with our 2021 GDP forecast at 4.5% and 4.9% in 2022. A key question for the European Central Bank (ECB) at its June meeting will be over the pace of asset purchases. We suspect that policymakers will not extend the stepped-up purchase pace, reverting to the levels seen in January and February. However, the phasing out of the ECB’s pandemic emergency purchase programme (PEPP) purchases may instead be a topic pushed by the inflation hawks.

The UK economy continues to show signs of resilience - GDP rose by 2.1%on the month in March. About 0.5 percentage points of this reflected the reopening of schools. Further Covid relaxations in April and May are set to give output an additional boost. We have nudged our 2021 GDP forecast up to 7.7% but maintain that growth could easily exceed 8%, especially bearing in mind our estimate that “excess” household savings reached £135 billion in March. Still, the B.1.617.2 strain of the coronavirus does seem to pose some threat to the reopening of the economy. However, the latest expert thinking suggests that its additional transmissibility (relative to the B.1.1.7 variant) is not as great as feared. With the Scottish National Party failing to get an overall majority at the recent Assembly elections, we have raised our end-year cable forecast to $1.44 from $1.40. We still see the first Bank of England (BOE) interest-rate increase occurring in mid-2023.

Global

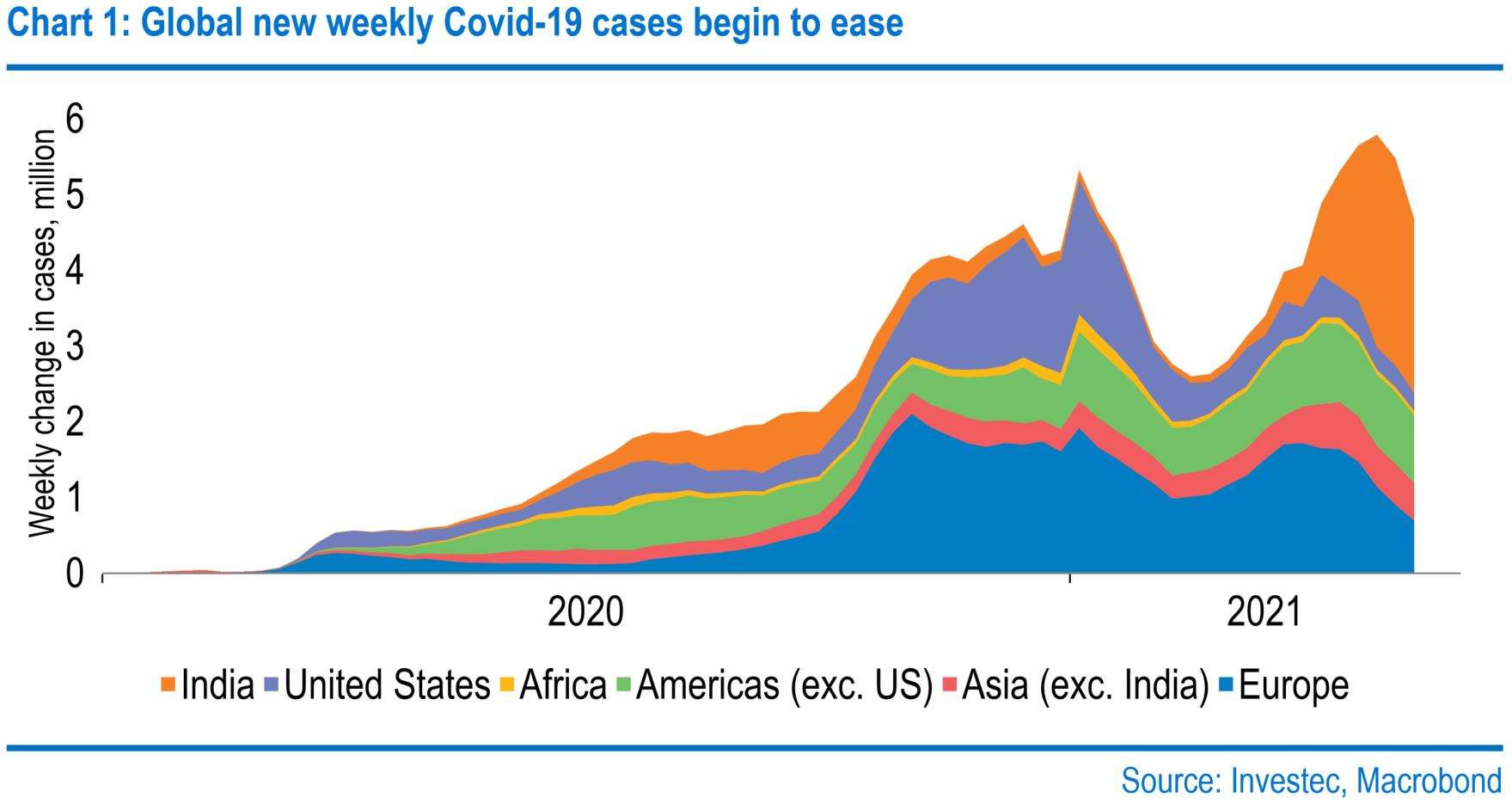

Global new cases of Covid-19 have ticked down recently as social restrictions and the deployment of vaccination programmes have limited the spread of infections in prior hotspots such as continental Europe. There are also early signs that India, currently the largest contributor to the daily case count, has reached the peak of their second wave. Daily infections are beginning to trend downwards, albeit from a very high level. Despite this encouraging direction of travel, the situation is extremely fluid and significant risks remain. As a result, we have held our 2021 global growth forecast steady at 6.2%, nudging 2022 up by 0.1 percentage point to 4.8%.

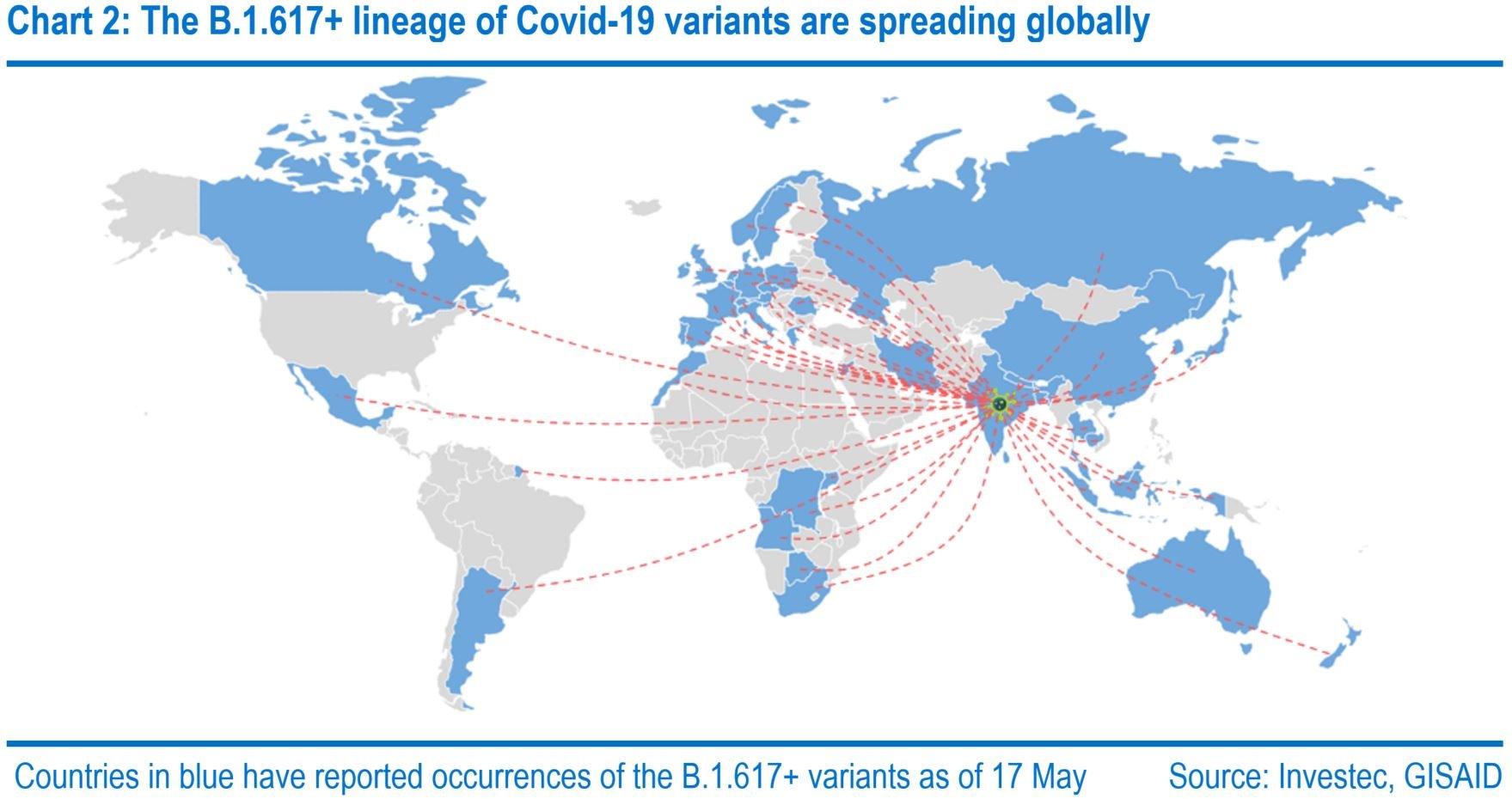

One of the key risks to the global recovery is the danger of potential new strains of the virus presenting themselves across the globe. The World Health Organization is monitoring this risk, compiling a list of “variants of concern”, to which B.1.617.2 was recently added after the sharp increase in Covid-19 cases in India was attributed to it. Vaccines appear to be effective against this new variant at this early stage, preventing serious illness in those studied. However, there is a high chance that it is more transmissible, posing a threat to healthcare systems across the globe. This is particularly concerning given the already extensive spread of the B.1.617 lineage, identified in at least 50 nations across the world.

Whilst Covid has remained a market concern, the last month has seen interest turn to inflation, with market measures of inflation expectations edging higher. Rising inflation prospects are also being borne out in economic data. Surveys such as the Purchasing Manager Indices (PMI) have recorded sharp price rises, the April Global PMI recording a record high in output prices. Meanwhile, national statistics have recorded a rise in inflation too. In April, US CPI hit 4.2%, the UK 1.5% and 1.6% in the Eurozone. Broadly inflation is expected to rise this year as it recovers from its pandemic induced weakness in 2020. However, the key question is whether this rise is a temporary phenomenon or something more persistent. Our view and the one which the major central banks share is that it is the former.

This view is based on several factors linked to the pandemic:

1. Mismatches in demand and supply are evident in indicators such as the PMIs’ backlogs of uncompleted orders measure. This has been caused by the surge in demand thanks to the reopening of economies, but supply being more constrained, consequently pushing up prices.

2. Base effects are also set to push annual rates of inflation higher.

3. The sharp rise in commodity prices will also push inflation higher this year.

However, given the makeup of these factors, we would expect these upward influences to dissipate as supply catches up and the distortions from base effects and higher commodity prices fade away.

For markets, the focus is on the risk that the rises are more sustained. A point we would make here is that persistently higher inflation is rarely seen without sustained higher wage growth. Given that the pandemic has created a significant degree of spare capacity in the labour market, this will likely take some time to achieve. For example, looking across various economies, employment remains significantly below pre-crisis levels and whilst the recovery should see labour market slack eroded, merely recovering the lost jobs is unlikely to close the output gap sufficiently to generate sufficient wage pressures. A factor here is the continued growth of the working population over the pandemic period who also need to find employment.

Although China was one of the few economies to post economic growth in 2020, there are signs that this remarkable recovery has lost some steam. Retail sales and industrial production data for April were weaker than headlines would imply, with the widely quoted annual rates distorted by base effects. The more representative monthly growth rates suggested a stagnant economic environment in April, a narrative supported by the official PMI data. In light of these developments, we have decided to alter the time profile of our growth forecasts, shifting the intensity into the latter half of the year. Arithmetically this results in a 0.2-percentage point downgrade to 2021 and a 0.1-percentage point boost to 2022, to 8.6% and 5.8%, respectively.

United States

Latest Covid vaccination figures show close to 50% of the total population having received at least one shot, allowing further easing of social restrictions. But rollout seems to be stalling in some states with take up correlated with political affiliation – inoculation rates in pro-Donald Trump states are lower. Party line divisions also remain in the Senate over President Joe Biden's $2.3 trillion infrastructure bill. The Republican Party is suggesting a total of $589 billion, but there are still hopes for a bi-partisan approach. Given the longevity of the package, and different approaches to funding via tax hikes, short-term growth prospects should not be too sensitive to the precise outturn. Our 2021 GDP forecast remains at 6.9%.

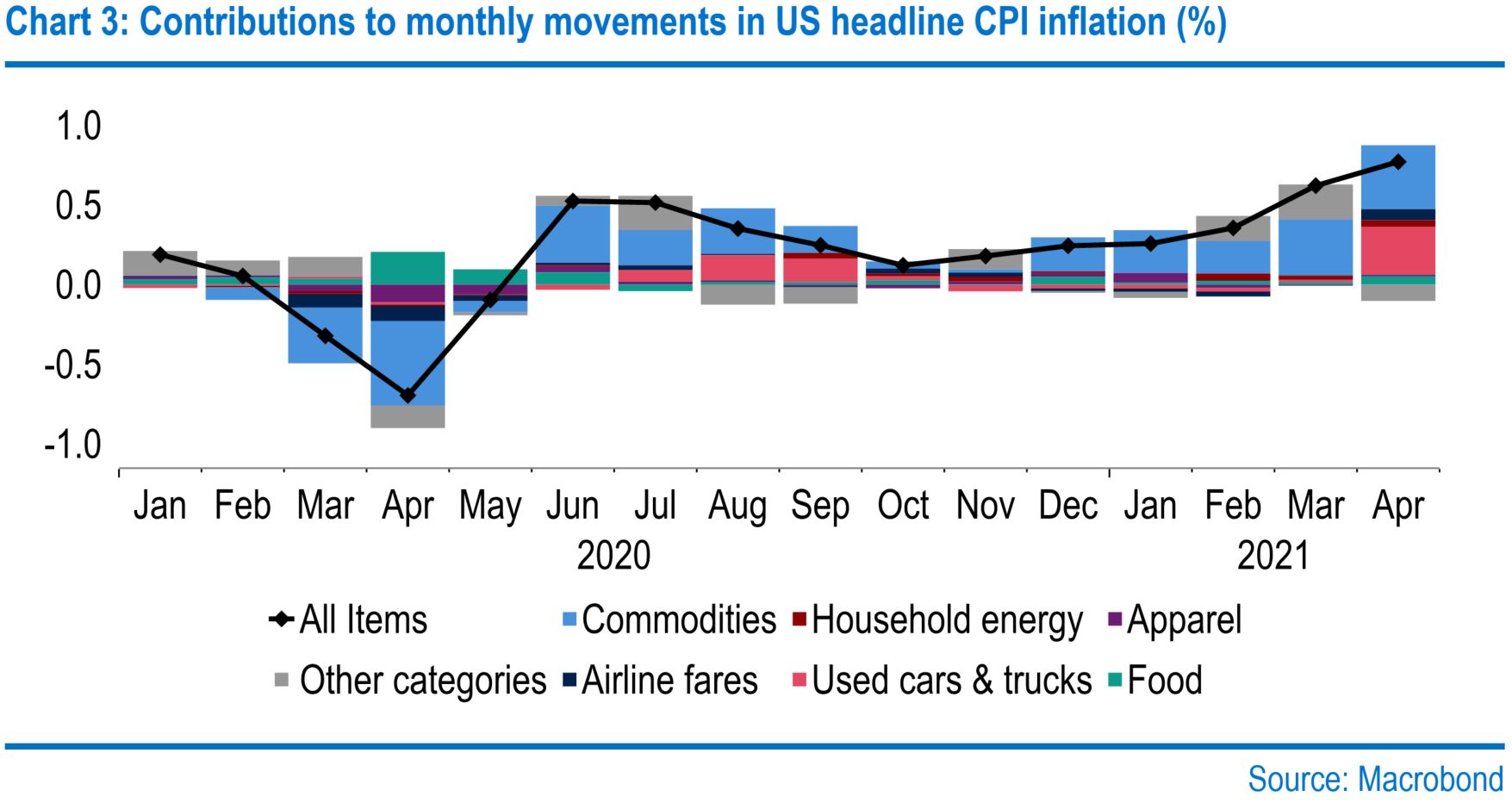

Markets have remained on alert to inflation news. April's CPI rose by 0.8% month on month, the core measure by 0.9% - the latter was the strongest monthly increase for 39 years. Commodity price pressures in world markets have been in evidence recently. Indeed, this was confirmed by April's CPI print. But the majority of the remainder of the increase can be explained by used cars and trucks, as well as airfares. Typically inflation arises as a result of an overheating economy with insufficient spare capacity to raise supply. We would argue this does not apply now, as, at 6.1%, the unemployment rate is 2.6 percentage points above its lows in 2019. Instead, the biting constraint (especially in car markets) is that stock levels cannot match the huge burst in demand.

Data show that total business inventory levels in March were at similar levels to a year earlier. But stock sales ratios are much lower, especially in the auto sector, forcing prices up. In due course, demand should moderate and output will rise, alleviating a bout of transient price pressure. Of course, we cannot be certain things will play out this way. There are risks that demand will be more persistent and of an outsized wage response, despite a relatively high jobless rate. Indeed, the Atlanta Fed's Raph Bostic hit the nail on the head when he remarked that it would take "a couple of months" to understand underlying inflation dynamics.

The more fundamental question, and arguably the key one for the Fed, is whether inflationary pressures will persist once the immediate demand bottlenecks are overcome. That will hinge on the labour market. We doubt wage pressures will spiral. The unemployment rate is still 2.6 percentage points higher than February 2020, and participation 1.7 percentage points lower. And even in what was a much tighter labour market in late 2019, when the unemployment rate stood at a 50-year low of 3.5%, which the members of the Federal Open Market Committee (FOMC) regarded as below its long-run level, wage growth undershot its long-term mean on most measures. In addition, weighted by population, hikes in state minimum wages this year are 4%, one percentage point lower than last year.

Gauging how inflation expectations have evolved, which ought to influence wages, is not simple. In financial markets, implied breakeven rates of expected future inflation can be derived as the difference between nominal and real (TIPS) bond yields. But if there is greater demand for TIPS relative to nominal bonds, for technical reasons, then implied breakeven inflation rates rise and implied real rates fall as nominal yields stay steady. That broadly characterises trends in the second quarter so far. With little news to warrant a downward adjustment to long-term real growth prospects, which may have provided a fundamental justification for such moves, it is unclear that "true" inflation expectations have risen.

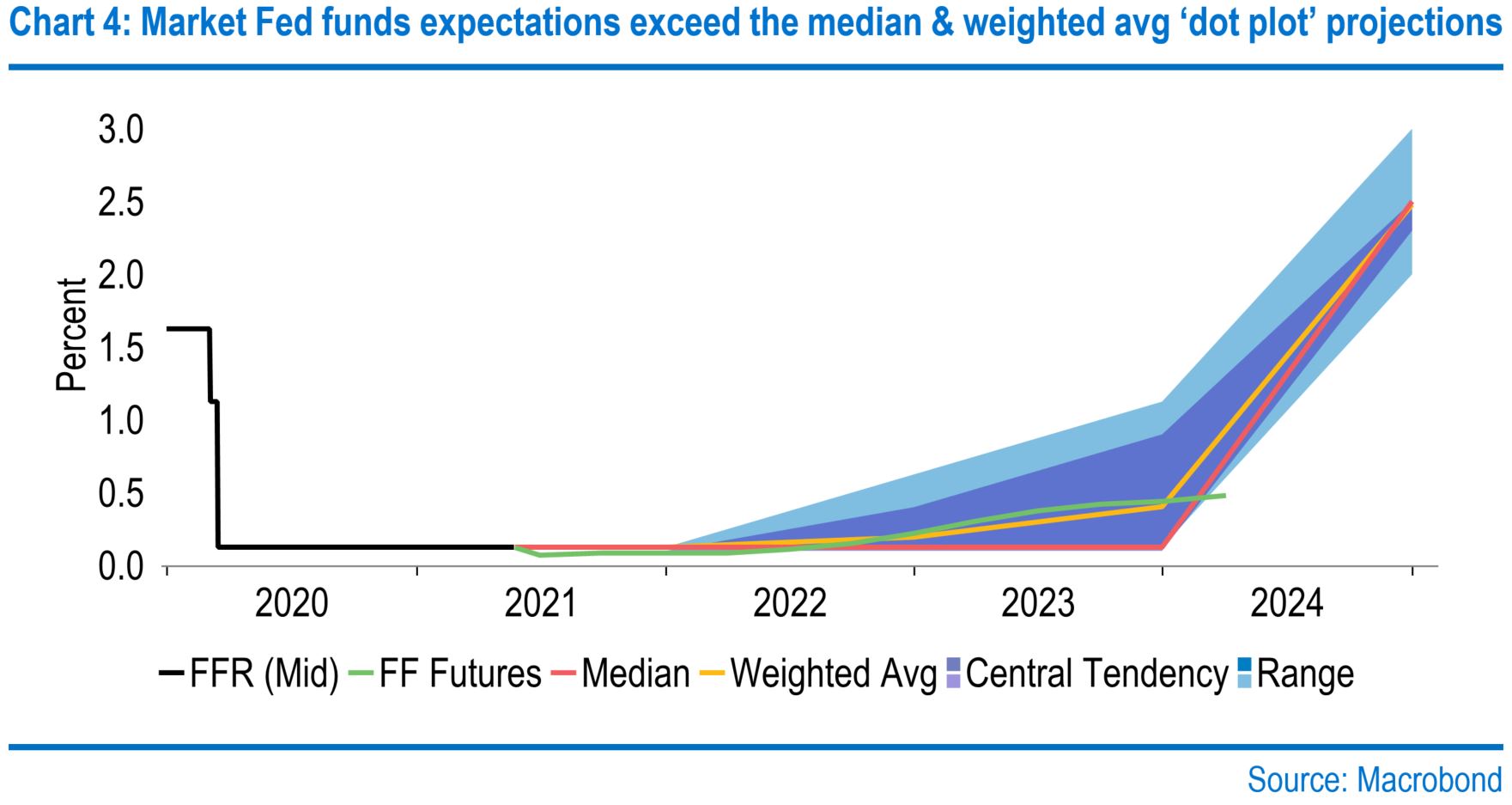

So far, despite concerns voiced by some FOMC members as noted in the latest meeting's minutes, the majority argued that near-term price pressures would be transient. How much inflation can go above target and for how long, to make up for past shortfalls, is not explicitly defined under the Fed's new flexible average inflation targeting monetary policy strategy adopted in August 2020. The current set of circumstances will put this to the test. Through the "dot plot" in the FOMC's quarterly projections, the next of which will be made available on 16 June, individual members can exercise a quasi-vote on future tightening, which may put pressure on Chair Jerome Powell.

Eurozone

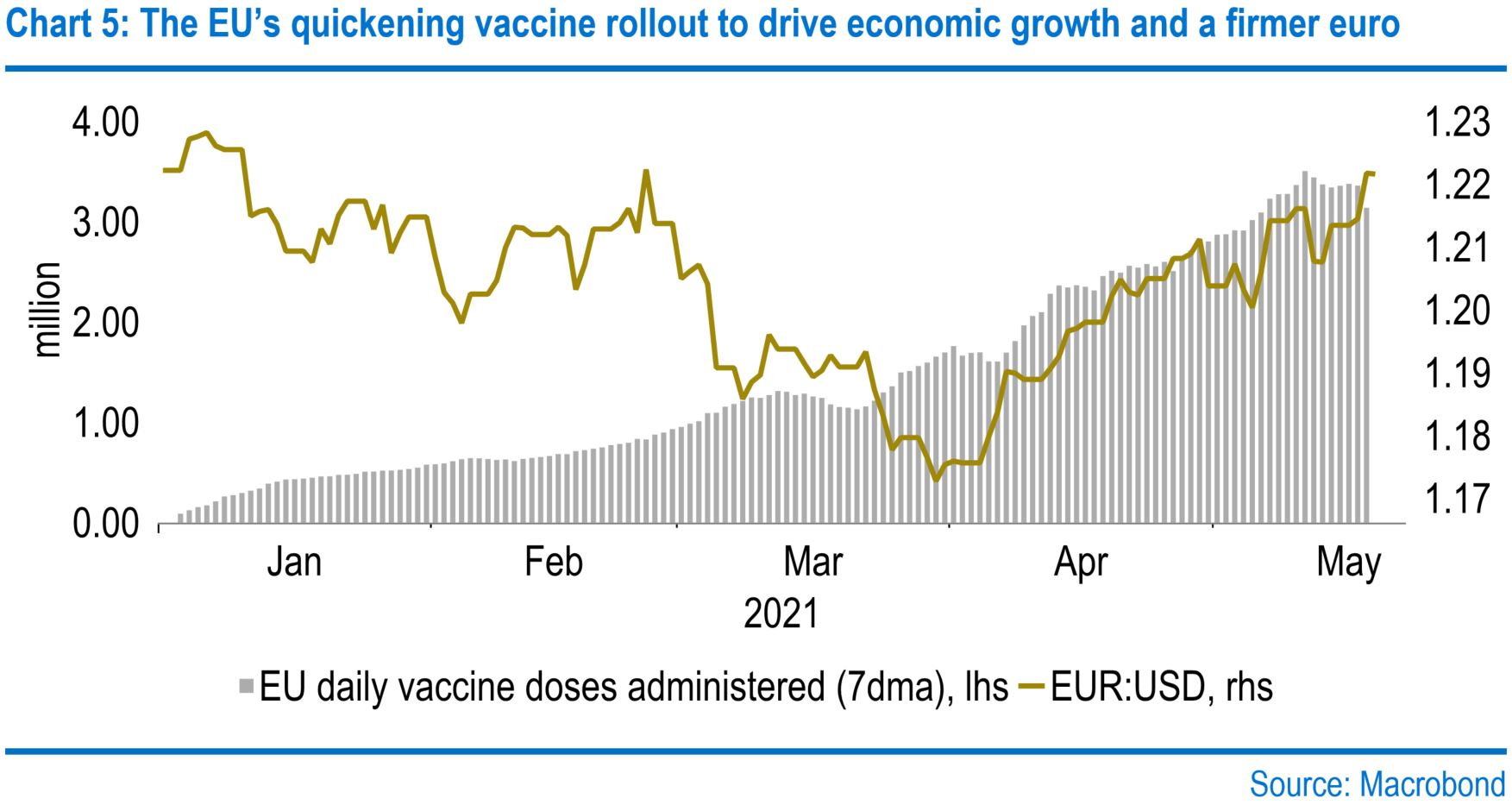

The first quarter saw a weaker euro as coronavirus infections surged, alongside a relatively slow vaccine rollout. However, since the start of April, the pace of vaccinations has significantly increased, helped by a new supply deal with Pfizer/BioNTech and a shift towards vaccinating younger people, who are more easily accessed. Meanwhile, falling Covid-19 infections have allowed much of the zone to begin easing restrictions, prompting a return to some normality and boosting the growth outlook. These factors have inspired some euro strength in the second quarter, which we see continuing as the economy unlocks further. We forecast the euro-dollar exchange rate to reach $1.25 by the end of this year and $1.30 by the end of next year.

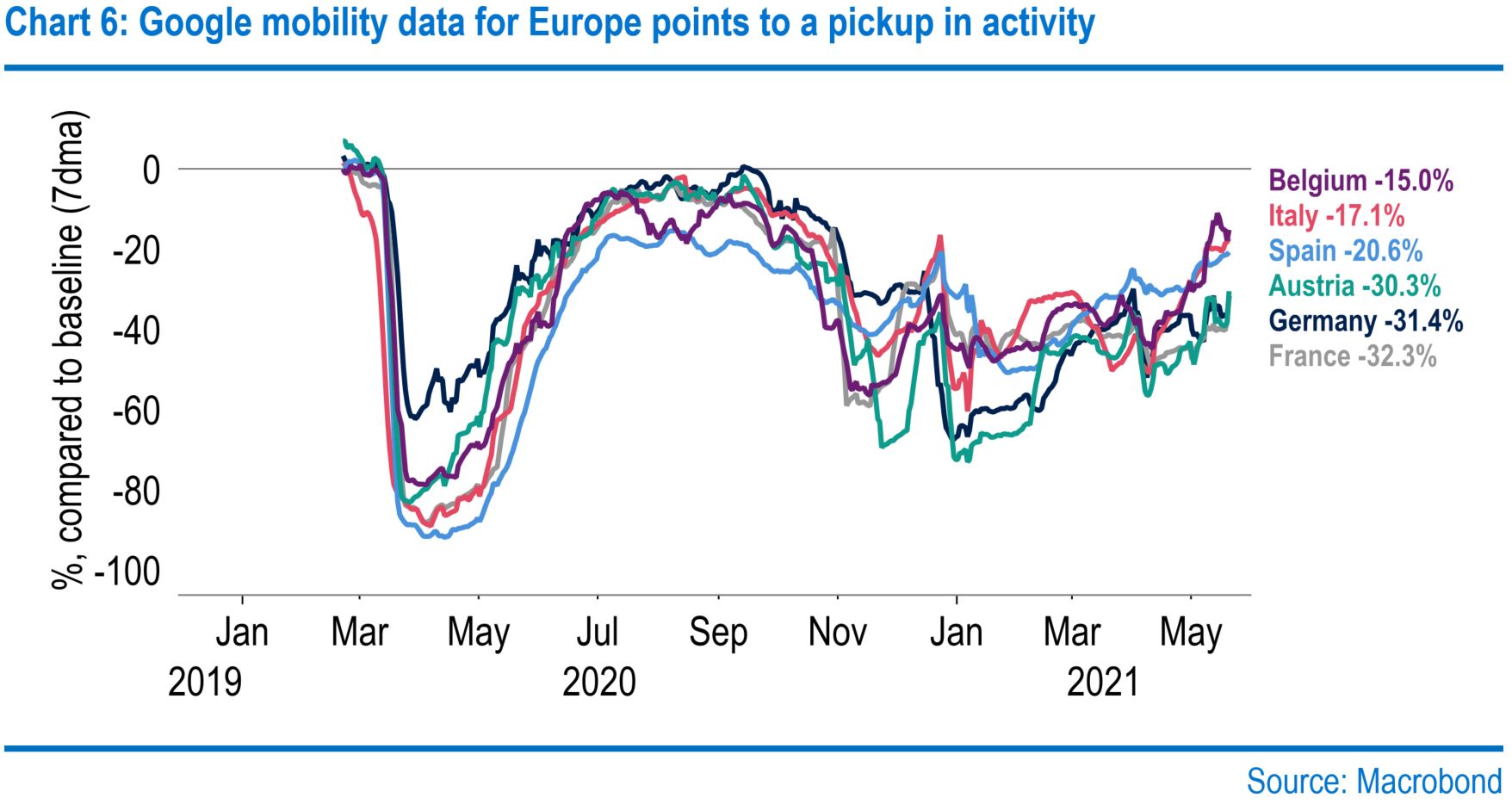

Vaccinations have contributed towards declining infection rates across European countries. Indeed total European Union daily cases now stand at 43,000, the lowest since October 2020. The easing of social restrictions across euro-area member states that has followed the turn in Covid cases has been widespread. For example, Spain has lifted its state of emergency, France has taken gradual steps to ease its lockdown, while Italy has allowed a partial reopening of the service sector. The positive economic implications have been evident in high-frequency data, such as Google mobility, which points to a rebound in Eurozone retail and recreation, now at -25% vs -35% in early April.

We see this as marking the start of a more sustained rebound in euro-area economic activity. Our forecasts for GDP stand at 4.5% for 2021 (4.4% previously) and 4.9% for 2022. We suspect that the ECB will upgrade its view at its June meeting, which could have a bearing on the pace of asset purchases. March's meeting saw the ECB pick up the pace of PEPP buying to prevent a tightening in financial conditions. That has been evident in the data, with purchases averaging €77 billion per month versus the €56bn average in January-February. We envisage the ECB reverting to its previous purchase pace rather than extending the current pace. Moreover, there are now also voices calling for a phasing out of purchases from the third quarter.

Notably, President Christine Lagarde did not rule it out when questioned, simply stating that it was too early to discuss. Ultimately, we suspect that the entire €1.85 trillion PEPP envelope will not be used, with our current forecasts putting total purchases at €1.7 trillion in March 2022. However, if the recovery takes hold and a third-quarter phasing gains support, this total could be smaller. Hence the ECB could slow purchases before the FOMC, given we do not expect a Fed taper until December 2021. A further factor that could suggest the ECB may be open to phasing is the relatively little it has said on the recent rise in European yields. The yield on 10-year German Bunds reached -0.09% on 19 May, exceeding the increase to -0.25% in February that prompted concerns over financial conditions and triggered the stepped-up pace of quantitative easing (QE).

Regarding monetary policy further out, concerns have been voiced by all three previous ECB chief economists – Otmar Issing, Jürgen Stark and Peter Praet – that, in the event of inflation rising too much and staying there, the ECB may be too slow to react. One worry is that forward guidance might restrict the Governing Council's nimbleness, even though it doesn't constitute a binding policy commitment. Another more fundamental concern is whether the ECB would politically be able to tighten as needed. The surge in debt levels, currently more than absorbed through QE, has raised the sensitivity of the public finances to interest rates. Tightening could threaten some governments' solvency.

Turning to other areas of policy, Germany's parliamentary elections on 26 September are garnering attention. Recent polls indicate the current "grand coalition" between the CDU/CSU and the SPD will fail to gain a majority, and that the race between the CDU/CSU, the party of current Chancellor Angela Merkel, and the Greens is neck-and-neck. Germany's electoral system in the Bundestag is one of mixed-member proportional representation, akin to that used in the Scottish and Welsh parliamentary elections. The Bundestag elects the Chancellor by absolute majority. Annalena Baerbock (Greens) or Armin Laschet (CDU) look best placed to succeed Angela Merkel.

United Kingdom

Further signs of economic resilience have been evident, as GDP rose by 2.1% in March month-on-month. Over the first quarter as a whole, output fell by 1.5%, with a net decline in the fourth quarter of 2020 and the first quarter of 2021 of 0.3%. That contrasts with many expectations at the end of last year of a double-dip recession. The reopening of schools in early March accounted for 0.5 percentage points of the gain during the month. Still, the 12 April (Step 2) relaxation of restrictions is likely to have propelled the economy further, helped by high levels of excess household savings, which we estimate totalled £135 billion in March. We have nudged up our GDP forecast for 2021 to 7.7% (from 7.5%), but this could easily exceed 8%. Our forecast for 2022 stays at 5.5%.

The labour market has also shown flexibility, with vacancies in the three months to April hitting their highest level in a year. Unsurprisingly, much of this increase can be attributed to industries reopening following the easing of restrictions, such as retail and hospitality. However, one concern for the labour market is a dwindling supply of available workers to fill vacancies. However, any resulting wage pressures are likely to be short-lived, with the expiry of the furlough scheme in September expected to add to the supply of available workers. Indeed, we project the unemployment rate to peak at 5.8% in the fourth quarter of this year.

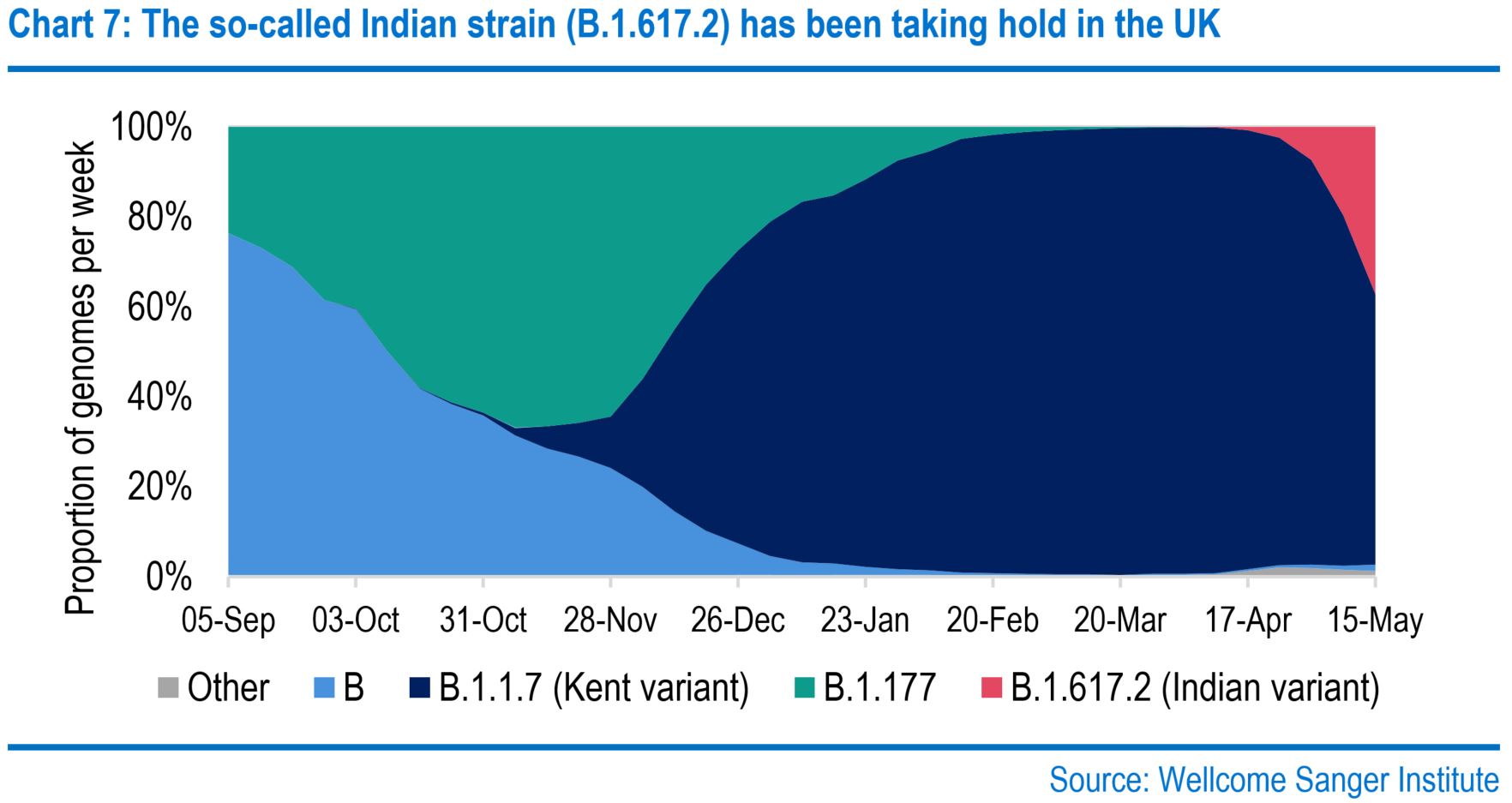

The latest Covid-19 threat is the so-called Indian variant of the virus, known officially as B.1.617.2. Total daily infections remain low and broadly stable. Still, the variant's apparent high transmissibility has seen it gaining ground in parts of the UK amid fears that it will soon become the dominant strain. Work presented to the Scientific Advisory Group for Emergencies (SAGE) suggests that were its transmission rate 30% higher than the so-called Kent variant (B.1.1.7), hospitals may be overwhelmed despite Britain's high vaccination rate. Fortunately, the first signs are that its transmissibility is not as high as feared. Hence, the fourth and final relaxation of social restrictions planned for 21 June may well go ahead as planned, and preventative measures such as local lockdowns may be avoided.

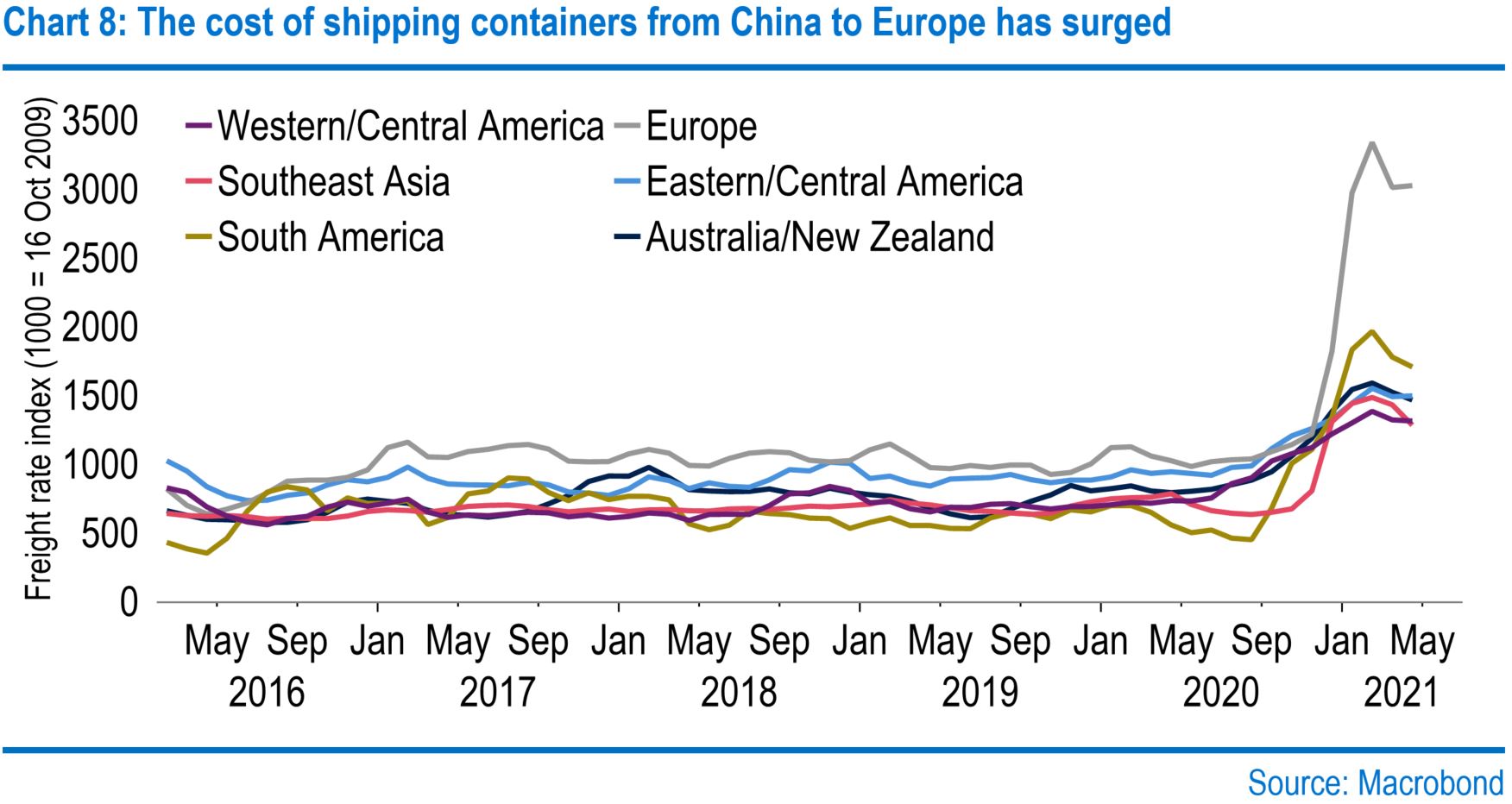

Adding to inflation worries, shipping container costs have soared, especially between China and Europe. The reasons are complex, mostly involving the burst in demand and limited increases in supply post-financial crisis. Covid-19 has left many containers in the wrong place too, with little economic incentive for empties to be picked up. Also, delays at ports have meant more containers are required for any given level of cargo. Container losses at sea have risen materially as well, including by the cargo ship ONE Apus, which lost a record 1,816 containers, with many others damaged. Poor weather and perhaps ship design and stowage techniques have contributed towards a perfect storm.

At its May meeting, the BOE's Monetary Policy Committee (MPC) voted unanimously to maintain its key interest rate at 0.1%. There was a shock dissent regarding asset purchases, with outgoing Chief Economist Andy Haldane voting to lower the targeted stock of purchases to £845 billion from £895 billion, causing some volatility in sterling in the immediate aftermath. Being considered a more hawkish member of the MPC, his late-June departure tilts the committee towards more favourable views on accommodative monetary policy, making the choice of his replacement an interesting one. Regardless of who steps up to the helm, we do not expect a rate hike until mid-2023.

The SNP has continued its hold on Holyrood, winning a record 48% of the constituency vote, but fell short of the 65-seat majority by one seat. With an increased pro-independence movement, supported by the Greens, the timing of a proposal for a second Scottish independence referendum (nicknamed "IndyRef2") remains to be seen, with First Minister Nicola Sturgeon stipulating that her current focus is on the response to Covid-19. Thus, the prospect of a proposal for IndyRef2 in the short term and the associated downside risks to sterling appear muted. Therefore, we have raised our pound-dollar forecast for 2021, now looking for it to end the year at $1.44. However, pound-dollar pressures remain in the medium to long term should IndyRef2 gains traction.

Would you like to hear from our economists directly?

Sign up to receive invites to our monthly economic Q&A with a member of our team.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.