A shot in the arm, not a shot in the dark

Prospects for 2021 heavily depend on the successful and prompt roll-out of various Covid-19 vaccines and test and trace systems. Of course, other factors are at play such as the new Biden administration in the US and more locally, Brexit. Our economics team analyse all of this in the latest Global Economic Overview.

We are looking for 2021 global growth of 5.8%, following an estimated 4.0% contraction in 2020. The recent good news on vaccines is supportive, and we hope for progress in dismantling some of the US’s trade barriers once President Biden has his feet under the table. Overall, we are looking for a modestly risk-friendly year, with the US dollar and safe haven sovereign bonds both retreating. Even so, we are wary over possible downside risks such as Covid-19 mutations and other ‘left-field’ negative demand shocks which could derail the recovery.

On the 20 January, Joe Biden will be inaugurated as US President. Importantly, though we await the result of two Georgia Senate run-offs on 5 January to see if the ‘Blue Wave’ emerges. This would likely unlock more material fiscal support. Importantly though the more fiscal support we see, the less assistance the Fed will need to unleash, equilibrating the upside for investors. Mr Biden may also start to consider revenue-raising tax action if 2021 growth picks up rapidly. Our forecasts are for a contraction of 3.6% in 2020 and a rebound of 4.5% in 2021, amidst a strong expected consumer-led recovery, aided by high household saving deposits.

Given the tightening in coronavirus containment measures over the last month, we see GDP declining again in Q4. Is this the start of a double-dip recession? We suspect not and expect activity to rebound in Q1 2021 and strengthen through the year, supported by the expected rollout of a Covid-19 vaccine and also under the assumption that the EU’s recovery package is ratified. Our GDP forecasts stand at -7.2% (2020) and +5.2% (2021). We continue to see the euro rising through 2021, ending the year at $1.25, supported by improving fundamentals and a general unwind of some of the US dollar’s strength. We also see 10-year German Bund yields rising to -0.30%, with any greater increase being restrained by significant ECB asset purchases, given we now see another €500bn being sanctioned in December.

Across the UK, various versions of ‘lockdown’ have been in place over the past month or so. Wales has now exited its ‘firebreak’, England and Northern Ireland remain in ‘national’ lockdown, whilst Scotland moves into more stringent restrictions for 11 areas. Such restrictions have dampened our near term economic assessment materially; we now look for a contraction in Q4 GDP. However additional government support such as the extension of the furlough scheme until March 2021, alongside positive vaccine news, bolster prospects for 2021. We forecast an 11.0% contraction in 2020 GDP and 7.6% growth in 2021. At the time of writing, Brexit negotiations continue and there does appear to be some light at the end of the ‘tunnel’. Our central case remains that a deal will be done. As a result, we forecast that £:$ will stand at $1.34 at the end of this year and reach $1.40 by the end of 2021, buoyed by a UK-EU deal and the roll-out of Covid-19 vaccinations.

Global

Positive vaccine news appears to be a turning point in the Covid-19 pandemic. Phase 3 (large scale) trial results show the efficacy of the Pfizer/BioNTech and Moderna vaccines to be 90-95%. Roll out should begin in December and gain ground through 2021. Globally 12 vaccines are at the Phase 3 stage, with those from Oxford/AstraZeneca and Janssen also at advanced stages. Estimates of globally announced Covid-19 vaccine capacity by the end-2021 stand at 2.94bn doses. But it is thought that this could reach as much as 10bn. In the meantime, recorded daily global Covid-19 cases and deaths have reached record levels. Europe currently accounts for 54% and 47% of these, respectively.

Denmark has seen an outbreak of a unique Covid-19 variant (‘cluster 5’) transmitted to 12 humans via farmed mink. Worryingly, initial findings suggest ‘cluster 5’ is less sensitive to antibodies. Denmark’s 17m mink are to be culled, but the episode raises questions over the possible effects of a mutating virus. Currently, countries experiencing 2nd (or in the case of US cities, 3rd) waves, have tightened social restrictions. Our baseline is that successful vaccines will enable the unwinding of social distancing over 2021, driving the world economy forward. We had already factored in a positive vaccine effect into our forecasts. But we now expect a slightly greater impact starting in Q2, not Q3, as previously stated.

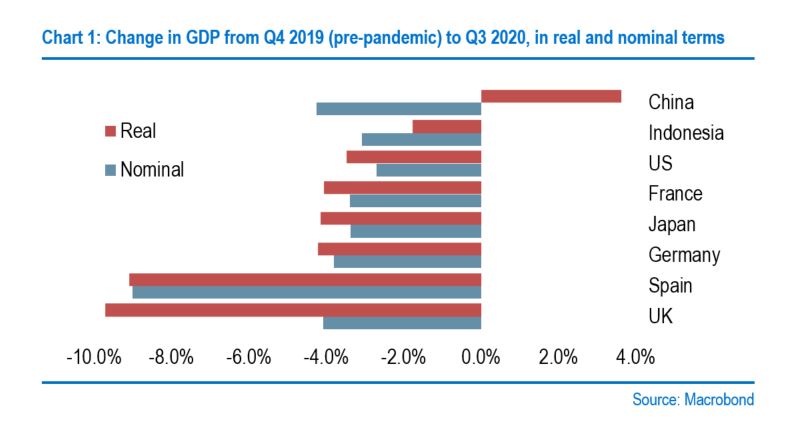

Around half the G20 economies Q3 GDP figures have now been published. Chart 1 shows that (excluding China) despite big Q3 rebounds, output was still 2-10% below Q4 2019 levels. Such variations are due to factors such as; the stringency of Covid-19 restrictions; the scale of monetary and fiscal responses; and the economic dependency on services, especially the hospitality sector. Another is perhaps the way that statistical authorities measure output, especially in the public sector. Chart 1 also shows changes in nominal GDP (where available), which reveals different patterns in specific economies, notably the UK and China, warning that one should not take data at face value.

Global trade is recovering, despite Covid-19 containment measures. It is worth noting that trade relations between the US and China were fraught throughout 2019 which weighed on global trade growth. Given Biden’s victory, we expect a departure from Trump’s protectionist approach. Biden will likely return to an era of ‘multilateralism lite’ in 2021 but not a ‘Clintonesque’ globalist approach. Whilst the US battles with increased Covid-19 cases and thus restrictions, China has returned to growth and continues to suppress cases. China’s position as the ‘world’s growth engine’ in 2021 will keep countries’ eyes on Beijing and indeed other east Asian centres, for trade.

Perhaps an early test is whether the new Democratic administration begins to dismantle some of President Trump’s trade barriers with China, and possibly the EU. The net effect on our thinking is that we have nudged up our 2021 world growth call to +5.8% from +5.6%, despite a likely negative ‘carry-over’ effect from the weakness of GDP in Europe, at the end of this year. Our 2020 forecast is now -4.0%, previously -4.3%, thanks to positive data from India. In this environment we envisage sovereign yields rising over 2021 – our end-year 10y Treasury target is still 1.25%. But our wariness over downside risks, including Covid-19 variants, means that we would stop short at embracing the ‘reflation trade’.

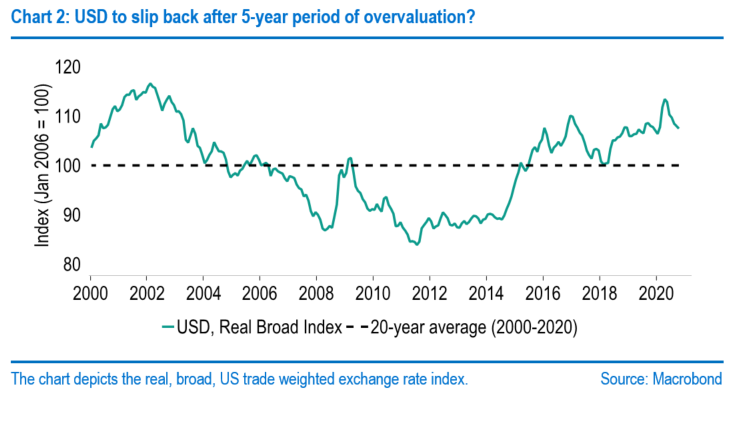

On FX, we judge that the dollar will retreat modestly in 2021 as risk appetite normalises (i.e. improves), which may end what we see as having been a five year period of overvaluation (Chart 2). Indeed this process could be more rapid if talk of the USD’s loss of reserve currency status re-emerges. Last, we (or others) did not have the ‘2020 vision’ hoped for 12 months ago and so we are wary over sounding too strident over our thoughts for 2021! Indeed, we are aware of the world’s vulnerability to a ‘left-field’ negative demand shock. How effective any policy response might be in these circumstances is questionable, given the monetary taps are already wide open and that fiscal metrics look highly adverse.

United States

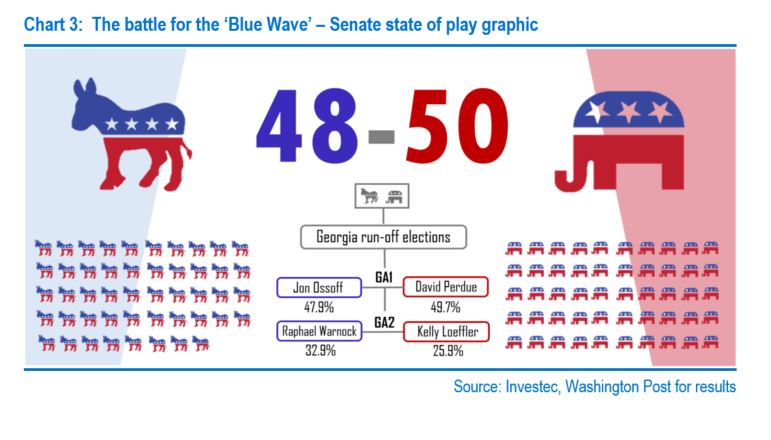

The 3 November US Election result sees Joe Biden head to the White House in January. That is, however, based on our expectation that legal challenges will not be successful and that ‘faithless electors’ will not be sufficient in numbers to overturn the result when the Electoral College ‘meets’ in December. The result has also returned a House of Representatives still under the control of the Democrats. However, we wait to hear if the ‘Blue Wave’ will be forthcoming, with two Georgia Senate races set to head to a 5 January runoff (chart 3). If the Democrats take both seats they will control the Senate, with Vice-President Kamala Harris holding the casting ballot.

Voters in Georgia are therefore set to decide if 2021 will be the year of the Biden-Harris agenda or of renewed efforts to make bipartisan policymaking work. When the new leadership arrives at 1600 Pennsylvania Avenue, big ideas may need to sit on the back burner for a time with some firefighting to do instead. Fast forward to the New Year and the leaders are likely to be faced with an economy that has emerged from a difficult Q4. Covid-19 infection rates have risen rapidly in recent weeks forcing some states to retighten restrictions. We judge that this retrenchment will weigh on Q4 GDP and we have modified our projections.

However, we look for a 3.6% decline for 2020 overall, after the robust Q3. 2021 continues to shape up positively, aided by vaccine news. The US administration has contracts with several vaccine producers, where progress/efficacy appears faster/higher than anticipated. Moderna (94.5% effective in its late-stage trial) views the US as its priority market. With high take-up expected (a study published by Lancet indicated 67%), we expect virus reproduction rates to fall markedly. That would pave the way for a marked easing in social restrictions, which should drive a sharp rebound in consumption.

Our central assumption is for GDP to grow 4.5% next year. One uncertainty is how supportive fiscal policy will be. Amidst a ‘Blue Wave’ investors had been anticipating a big giveaway. However, if consumption is picking up robustly in Q1, Mr Biden may shift to focus on some of his wider plans, which include an uplift to Corporate Tax from 21% to a higher 28% rate. If the Senate remains under GOP control, there are bipartisan politics to navigate. But even then, the pursuit of bipartisan objectives such as "Made in America" tax subsidies might help progress a package where some tax increases on the wealthy are laid against modest tax cuts for low and middle-income households.

One stabilising force for risk sentiment is that the more fiscal support Congress provides the less we can anticipate from the Fed and vice-versa. The Fed voting rotation in January looks set to usher in a slightly more dovish voting panel. However, already, in the aftermath of the Fed’s strategy update, the FOMC would rather err on the side of providing more rather than less support. A temporary overshoot of inflation against target would be welcome, given the shift to inflation averaging. Our central assumption is that the FOMC will hold the Federal funds rate steady and continue with open-ended quantitative easing (QE) through 2021. It may even tinker with the latter, to weigh down longer-term yields. Mr Biden’s win should signal a calmer approach to international relations and global trade sentiment.

A return to an ‘international’ approach looks likely, albeit a prudent one. Why? He will need to ensure that an outward-looking US also looks inwards to help manufacturing, for example. Finding a balance is something that will define the success of Mr Biden’s trade policy. What this means for the USD is less clear cut - moves over the Trump era reflected much more than Trump’s trade war action. As such, under Mr Biden, the dollar could well gain from the so-called ‘sanity premium’ of fiscal stimulus being agreed as much as from a positive shift in trade relationships.

Eurozone

EU19 downside risks materialised in the last month, the resurgence of coronavirus almost certainly triggering an economic contraction in Q4. Tighter social restrictions are the key factor, but differences in stringency are set to see economic performances vary across countries. However, we do not see Q4 witnessing the same severity as Q2’s 11.8% GDP fall, principally as measures have not been as harsh. Sectors such as manufacturing have remained open, as has hospitality in many countries (Spain, Italy). Do we see this as a precursor to a double-dip? Ultimately no, with our expectation being for social restrictions to be eased and for activity to rebound in Q1 2021.

Looking into 2021 our broad view of the economic outlook is supported by two key assumptions. Firstly, we are now factoring in a firmer pace of growth given developments around a Covid-19 vaccine, its roll out over the year and ultimately an abandonment of social restrictions. Secondly, whilst issues remain in ratifying the EU’s long term budget and recovery fund, we have assumed that those difficulties are ultimately overcome providing the EU with a significant degree of fiscal stimulus. As such our GDP forecasts now stand at -7.2% 2020 and +5.2% 2021 (4.8% previously). Note 2020 sees an upgrade, principally due to France’s performance in Q3.

During the summer, EU leaders agreed on a significant package to address the Covid-19 pandemic, including the historic deal over the NextGenerationEU initiative, which includes the RRF*. However, ratification is being held up by Poland and Hungary who vetoed a critical plank in the package which ultimately risks its delay and may undermine the recovery. €1.82trn of fiscal support is at stake (€1.07trn budget, €750bn NextGen), which we see as being a key point in supporting the recovery, but also helping to foster an improvement in long term growth, given an emphasis on public investment. Despite political posturing, we assume that an accord can be reached given Poland and Hungary receive significant fund allocations and that a failure to reach a deal would not be in their interests either.

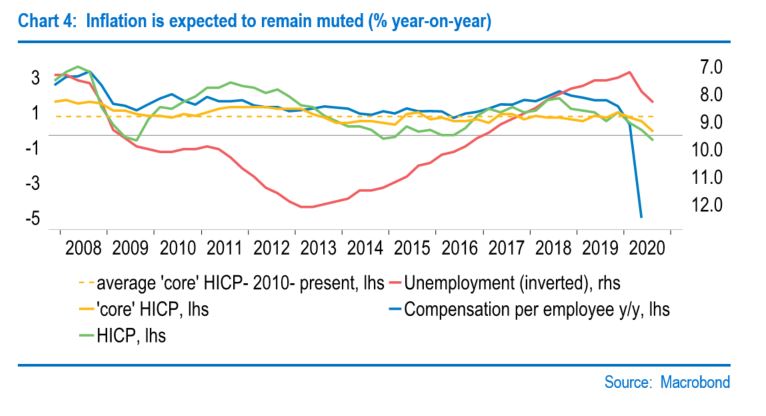

Meanwhile, inflation prospects are set to remain muted, the pandemic dealing another blow to a pick-up in inflation, which over the last decade had seen core HICP (Harmonised Index of consumer-prices) average just 1.1%. One factor is set to be the labour market. To date, unemployment has risen to 8.3% and is set to tick higher in the near term, before recovering in the longer term. However, even by the end of 2022, we still see the unemployment rate higher than pre-pandemic levels and as such a degree of spare capacity is likely to exist and weigh on the inflation recovery. It is worth noting that this outlook would have been weaker were it not for the job support schemes across the EU19, many of which have been extended into 2021 and beyond.

Against this outlook, ECB policy is set to remain exceptionally accommodative in 2021, with December’s Governing Council meeting already signposted for a ‘recalibration’. Here the ECB has stated that all tools are under consideration, but we see policy announcements centred on QE. On the former we see the ECB sanctioning a €500bn increase taking the total up to €1.85trn. Meanwhile, amidst a reported tightening of credit supply in the ECB’s bank lending survey, we see TLTRO again being made more attractive to support credit growth. We see the deposit rate remaining at its current setting of -0.50% until late 2023. One final point is that the ECB’s framework review will be concluded in 2021 and could have implications for the ECB’s inflation target.

In terms of market forecasts for 2021, we see €:$ rising to $1.25 by the end of the year. Prominent factors here include a better risk backdrop, a rebound in growth as economies loosen restrictions and vaccines are rolled out, as well as extensive EU fiscal support. In the fixed income space, we see 10-year German Bund yields firming marginally to -0.30% in Q4, as significant ECB asset purchases restrain any greater rise. Politically, 2021 plays host to a number of elections, most notably the German Federal election concluding in October. Moreover, the Dutch general election will take place in March and the Portuguese presidential election in January.

United Kingdom

An easing of coronavirus restrictions has seen the UK economy rebound from its lockdown lows, with GDP jumping 15.5% in Q3 after a historic 19.8% slump in Q2. But output is still 8.2% below February’s pre-pandemic level and consistent with mid-2014. To make matters worse, the recovery is set to suffer a setback after England imposed a four-week lockdown (ending 2 Dec). Still, this will not be as disruptive as the one in March, as manufacturing and construction activity can continue. We also suspect that service providers are better positioned after having to adapt earlier in the year. For instance, remote working is now entrenched and more firms now offer collection and takeaway.

Even so, November is likely to see a near double-digit decline in GDP, meaning that a contraction over Q4 is now inevitable. But the subsequent re-opening should mean that Q1 will be firmer than we had initially expected. As such, we now look for sharper 11.0% decline in 2020 (prev. -10.1) followed by a firmer rebound of 7.6% in 2021 (prev. +6.3%). Also, any further ‘scarring’ should be limited by the furlough scheme being extended, but unemployment still looks set to climb after its planned winding up in March. More broadly, the path to recovery will hinge on the development and rollout of a vaccine, which is discussed in more detail in our ‘Global’ section.

Another key determinant of the outlook will be the future UK-EU trading regime. Both sides are said to be working towards a 23 November deadline, but remain far apart on fishing rights and the “level playing field”. While there is a material risk of ‘no deal’, we still expect an interim agreement to be clinched, with a full FTA following at a later date. However, firms will have little time to prepare for the new arrangements, all whilst having to deal with the second wave. The latest BoE Agents’ survey found that ⅓ of EU-trading firms expect to be fully prepared for the transition, with ⅔ ‘as ready as they can be’. This is likely to result in some trade disruption in H1 2021, weighing on GDP, though this should later ease as new processes are bedded in.

At its last meeting, the Bank of England’s MPC decided to raise the gilt purchase target by £150bn to £875bn. One thing noticeably absent was a negative rate discussion, but this may come into greater focus as the Bank closes in on its self-imposed limit of owning 70% of the gilt “free float”, with the latest round of QE leaving it roughly £66bn of ‘headroom’. Although this will rise as the DMO issues more debt, the MPC is unlikely to be able to repeat this year’s £440bn expansion. Attention could turn to unwinding of QE before rate rises, which the Governor has indicated is his preference. Otherwise, negative rates are more likely to be deployed in the next crisis

Politically, 2021 is set to be an interesting year as the delayed 2020 ‘Local’ elections take place on 6 May. These include English Councils and 13 directly elected mayors in England. Moreover, there are elections in Scotland, Wales and London, the last in conjunction with the London mayoral election. As seen in Chart 23, Boris Johnson’s popularity has decreased since the onset of the COVID-19 pandemic, thus these ‘locals’ may further increase that view. More recently, Nigel Farage is set to re-brand the Brexit Party into the Reform Party on an anti-lockdown ticket, which may provide problems for the Tories. Another headache is likely to come in the form of a renewed SNP Holyrood majority demanding IndyRef2.

Mr Johnson will attempt to see off these threats with his ‘levelling up’ pledge. While this has been waylaid by the pandemic, its structural consequences provide a unique opportunity for a bold industrial strategy that closes regional productivity gaps. We may see how ambitious he plans to be in the 1-year Spending Review on 25 November. If he fails to turn around his party’s fortunes, he may well make way for a new leader. Media reports suggest he is struggling on his £150k salary and Betfair odds indicate a ⅓ likelihood that he steps down in 2021. A leadership change poses bimodal risks to our end-21 target of $1.40 for sterling, but Brexit and virus developments are likely to still dominate UK risk sentiment.

Would you like to hear from our economists directly?

Sign up to receive invites to our fortnightly economic Q&A with a member of our team.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.