A summer break from dismal economic data

The newsflow around the coronavirus pandemic continues to improve globally, with the rate of infections slowing, progress toward a vaccine being made, and economic data indicating a rapid pick-up as governments continue to ease social restrictions. While we remain cautious in the medium-term, our latest Global Economic Overview sees some mild forecast revisions, including an upgrade to the growth outlook for the US and Eurozone.

A more positive tone surrounding the coronavirus has emerged, as worldwide daily infections appear to have fallen back and further progress is made on various vaccines. Economic indicators have been on the firm side of market expectations, vindicating our view of a restricted or "lopsided" V-shaped recovery in most economies. But we remain cautious in the medium-term. First, the surge in retail sales in areas such as the US, Eurozone and the UK reflects pent up demand deriving from unspent income over the lockdown months and is not sustainable. Second, although some countries are extending worker protection schemes, the degree of overall fiscal support is set to wane, given adverse budgetary positions. We dismiss talk of an upsurge in inflation, despite increases in breakeven yields and inflation swaps, plus rallies in precious metals prices.

The evolution of the Covid-19 situation in the US looks less concerning given lower daily infections and rapid declines recorded in hotspots such as Florida and Arizona. Despite a lack of agreement on a fiscal stimulus bill in Congress and some related weakness in selected economic indicators, the balance of news has been positive over the past month and we have pushed up our 2020 gross domestic product forecast to ‑4.9% from ‑5.6%. During Republican National Convention week, President Donald Trump still finds himself lagging well behind Democratic challenger Joe Biden, both nationally and in swing states. The source of the balance of power in November seems likely to be from the Senate races, where the overall contest looks very tight.

The second quarter saw the euro-area economy contract at the fastest pace on record, with a 12.1% quarterly drop in GDP, albeit with differences in regional performance influenced by the stringency of individual country lockdown measures. In a reversal of the second quarter’s decline, the subsequent easing of containment measures looks set to prompt a material rebound in third-quarter GDP. However, this is subject to risks stemming from the sharp rise in daily coronavirus infections which is fuelling fears of a material second wave. In light of the second-quarter GDP, we have revised our 2020 GDP forecast to -7.2% from -7.5%, while 2021 is unchanged at +5.3%. Significant moves in the euro have also resulted in us pushing up our euro-dollar forecasts, which now stand at $1.17 in the fourth quarter and $1.25 in the fourth quarter next year.

UK GDP climbed by a record 8.7% in June as the reopening of the economy pushed forward. Also, surveys and real-time data indicate the recovery has persisted through both July and August. Our forecasts are broadly unchanged - we look for a contraction of 8.4% in 2020 to be followed by a rebound of 6.6% in 2021. Risks to the outlook remain to the downside, not least due to the possibility of a severe second wave. Besides this, the continued stalemate in UK-EU negotiations brings with it the prospect of a cliff-edge at the end of the year. However, we still believe talks will yield a bare-bones deal, with a more comprehensive free-trade agreement (FTA) secured later. That underpins our forecast for a strengthening in the pound to $1.34 by the end of 2020 (previously $1.28), and to $1.40 by the end of 2021 (previously $1.35).

Global

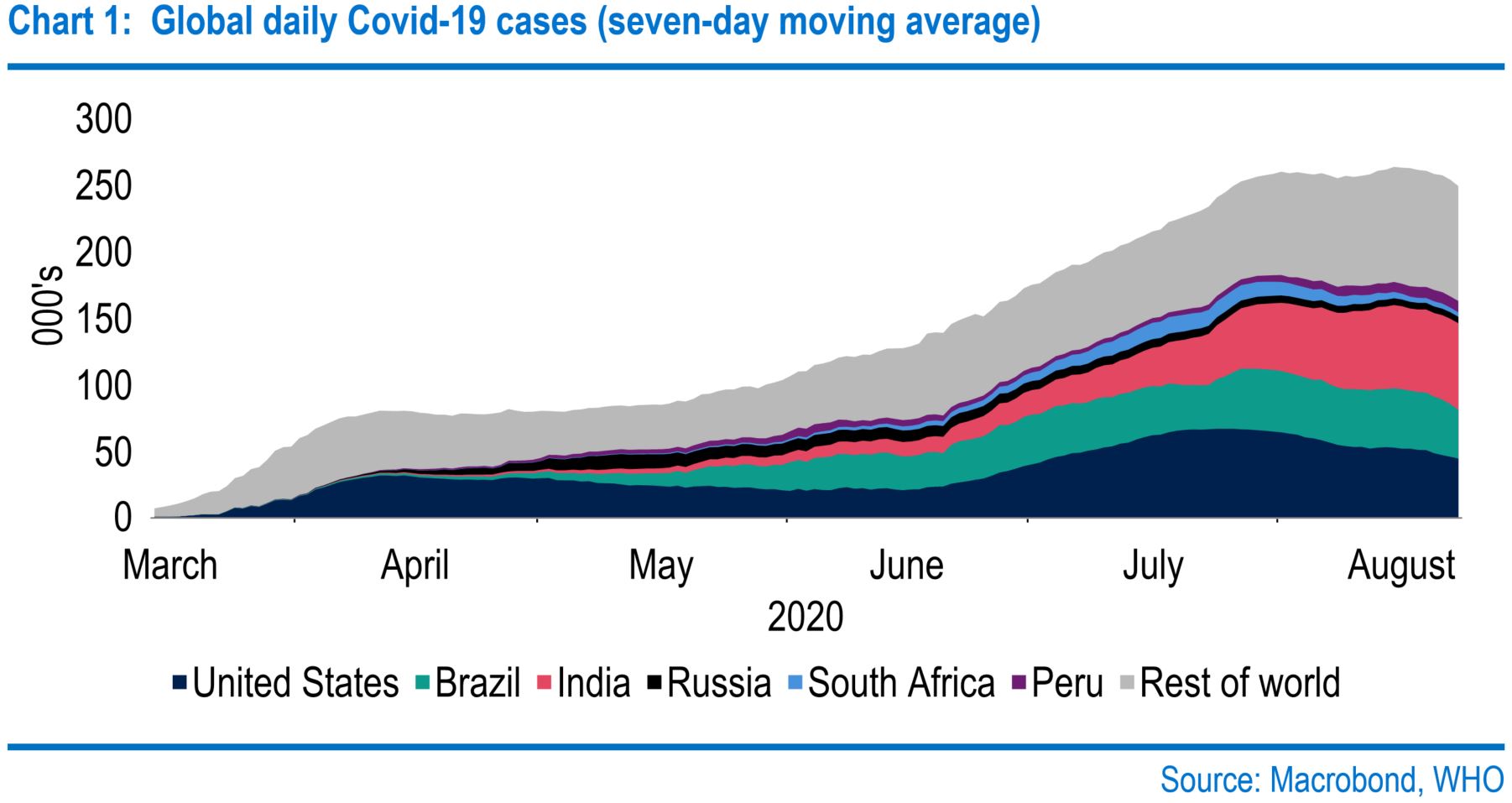

The coronavirus impact continues to dominate the world economy and financial markets. Better news has arrived in the shape of an apparent levelling out in daily infections – of the six countries with the highest infection rates, only Peru is still on a rising trend, and daily cases in the US are now declining. With this data, caveat emptor applies as we cannot vouch for its accuracy. Even so, progress is being made with a vaccine. Over 165 are in development worldwide, with 32 in phase 1 and phase 2 human trials and a further eight at the mass phase 3 stage. Also, vaccines by CanSino and Gamaleya have gained limited approval in China and Russia. All being well, 2021 will see less need for lockdowns and social distancing.

We have argued for some time that despite what is likely to be a difficult two to three years for the global economy, the path of the recovery cannot be described as "U-shaped". Second-quarter GDP data, now available for most major economies, show the extent of the declines, but the monthly dynamics of surveys (plus various official data such as retail sales, industrial production and GDP itself where available) clearly show a rapid pick-up. Various central banks have remarked on the sharper than expected rebound in activity since April, driven by the easing of social restrictions and the release of pent up demand. The latter is demonstrated by UK, US and euro-area retail sales (in cash terms) now standing at levels above a year ago.

But the current pace of retail sales reflects temporary factors such as the unwinding of record saving ratios (which stood at 33.5% in the US in April). For some perspective, there has been wide variation in the GDP declines across various economies since the fourth quarter last year. These range from 22.7% in Spain, to a fall of 10.6% in the US, to a 0.4% increase in China. Note that arithmetically, a straight percentage reversal of these declines would not bring GDP back to end-2019 levels, as they occur from a lower base. After what is likely to be a decent third quarter in most economies, progress in regaining pre‑pandemic GDP levels seems set to stay modest, especially given a likely withdrawal of some fiscal support.

Highly expansionary fiscal policy has been essential in containing the economic effects of the "Great Lockdown". But fiscal sustainability arguments point to indefinite fiscal support on this scale not being an option. In June, the International Monetary Fund estimated that deficits would average 14% of GDP this year, while debt-to-GDP ratios would exceed 100%, a deterioration exceeding that in the financial crisis. Also, these calculations exclude not only a possible new US package, but also the new 750-billion euro European Recovery Fund. Overall, we see no need for any material shift in our global GDP forecasts. These are now -3.9% this year and +5.6% next (previously -3.8% and +5.5%).

Much talk in our Global Economic Overviews recently has concerned sub-zero government bond yields and how far forward policy curves have priced in negative US and UK rates. Benchmark 10-year bond yields have jumped by 10-15 basis points this month, so this is now less of a talking point. Even so, it is interesting to look at these moves by examining their real and inflation components. The key driver in the turnaround is that real yields have stopped falling and in some cases risen. Meanwhile, breakeven yields, on a rising path since late-March, are still climbing. But the point is that they have not yet regained late-2019 levels, i.e. inflation expectations are still normalising from very low levels and not providing a warning signal of high inflation.

More positive news on the economy and Covid-19 trends have helped to propel many global stock indices upwards. In particular, the S&P 500 and the Nasdaq have hit record highs over the past month, while the DAX, OMX and SMI are up on the year. Still more striking has been the surge in gold and silver prices since the end of June. These surged during the height of the speculation about extensive negative rates and accordingly have given up some of their gains. But markets have not given up on a search for alternative investment vehicles (Bitcoin has risen more than 25% since June). Question marks in some quarters over the possible death of the US dollar as a reserve currency may also be a contributory factor.

United States

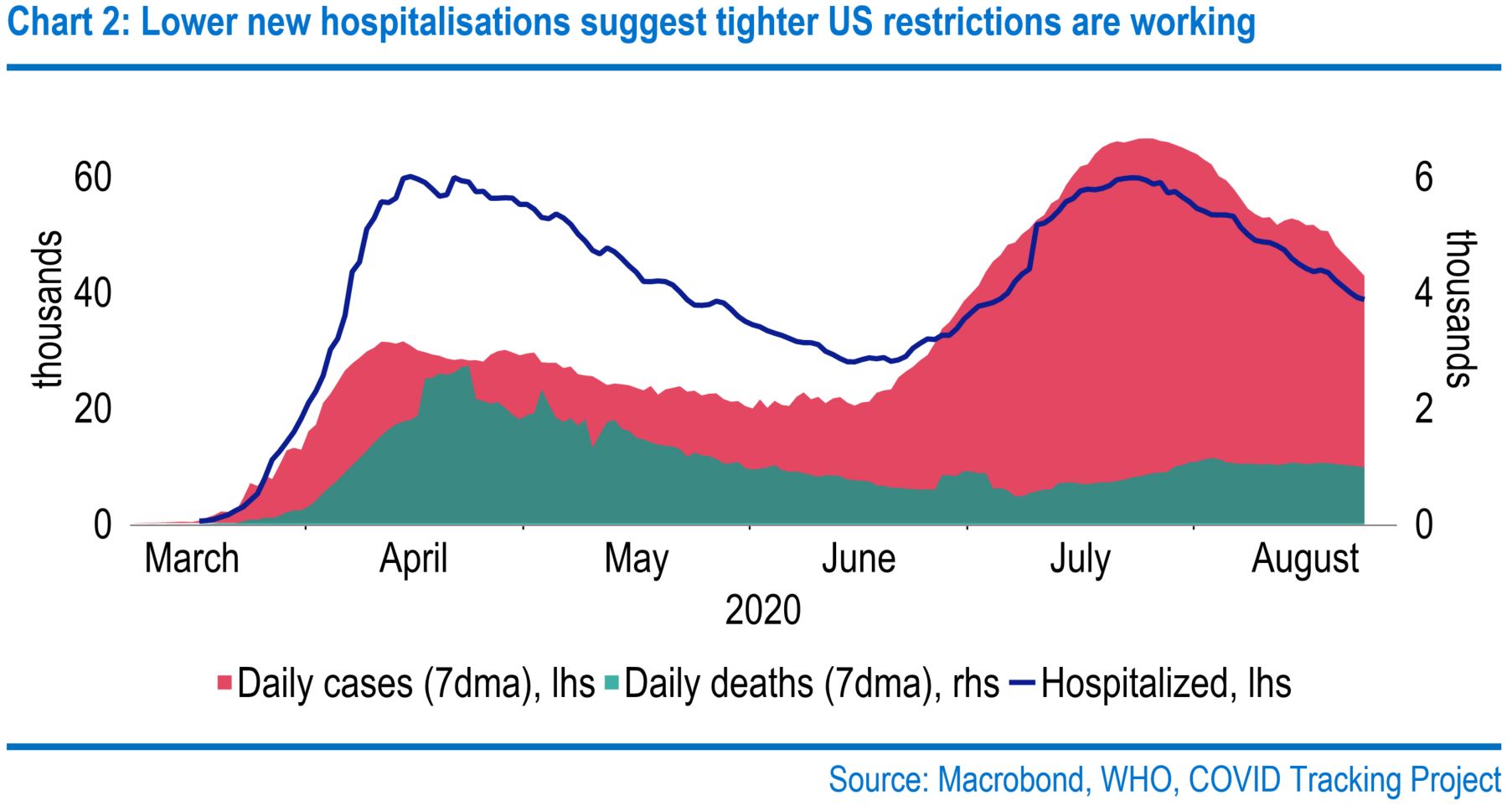

The evolution of the US Covid-19 case situation looks less concerning than a month ago. The seven-day average case total is now down to 43,000 from 66,000 at the end of July. Lower reported infections come amid a lower daily number of tests, raising questions over the validity of the improvement. However, the better situation does appear to be real. Although the daily deaths trend is relatively flat, new hospitalisations have reduced. Furthermore, the proportion of positive tests has fallen. The improvement reflects the tightening in restrictions that followed the July peak in cases. For example, in Florida, daily reported cases are down to around a third of their peak level and in Arizona, down to a fifth.

The tightening in restrictions has come at a price, with real-time activity metrics suggesting a subsequent softening in the pace of recovery. However, we maintain that a strong rebound in activity over the third quarter is likely and this prospect is confirmed when looking at metrics such as the New York Federal Reserve’s Weekly Economic Index (WEI). This is an index of ten daily and weekly indicators of real economic activity scaled to align with the four-quarter GDP growth rate. Despite some volatility in the WEI, it does suggest that recovery momentum has picked-up steam again over the past month. The shape of the recovery so far has persuaded us to raise our expectation for third-quarter GDP growth, and for 2020 we now look for -4.9% (previously –5.6%).

We look for +4.2% next year (previously +4.4%), with the possible availability of a vaccine paving the way for something of a return to normality in business operating conditions. That should help to drive further improvement in the jobs recovery, which still has a long way to go. Fed Chair Jerome Powell is keen to emphasise that the US central bank will be there right through this recovery. We expect the Fed to add to this message, with more formal forward guidance at some point, but it is not ready to do so yet. When it does, rather than tie guidance to unemployment rates, which are being subject to noise and misclassification errors currently, we suspect the Fed will opt for inflation-based guidance.

One further uncertainty for the economic backdrop is how supportive the fiscal stance will be. After cross-party fiscal talks broke down, President Trump signed four memorandums and executive orders enhancing unemployment benefits, deferring payroll taxes and student loans, and on housing assistance. These are no substitute for a comprehensive fiscal package - at face value, they provide some $165 billion of near-term funds. But as much of the money was already allocated and deferred taxes would be paid later, the Committee for a Responsible Federal Budget estimates the net cost at $10 billion.

Beyond the end of the year, the policy backdrop faces much more significant change if polling models are to be believed. As things stand, Joe Biden retains a large lead. FiveThirtyEight released its first election model prediction which had Biden with a 71% (Trump 29%) chance of winning the Electoral College, in a simulation run 40,000 times. Interestingly, their final forecast in 2016 also had Trump at 29%! But the latest prediction still reflects the significant amount of time to pass before the 3 November election, rather than because polls are close. Indeed, Mr Biden’s lead has already topped Hillary Clinton’s post-convention peak, plus he enjoys more overall support.

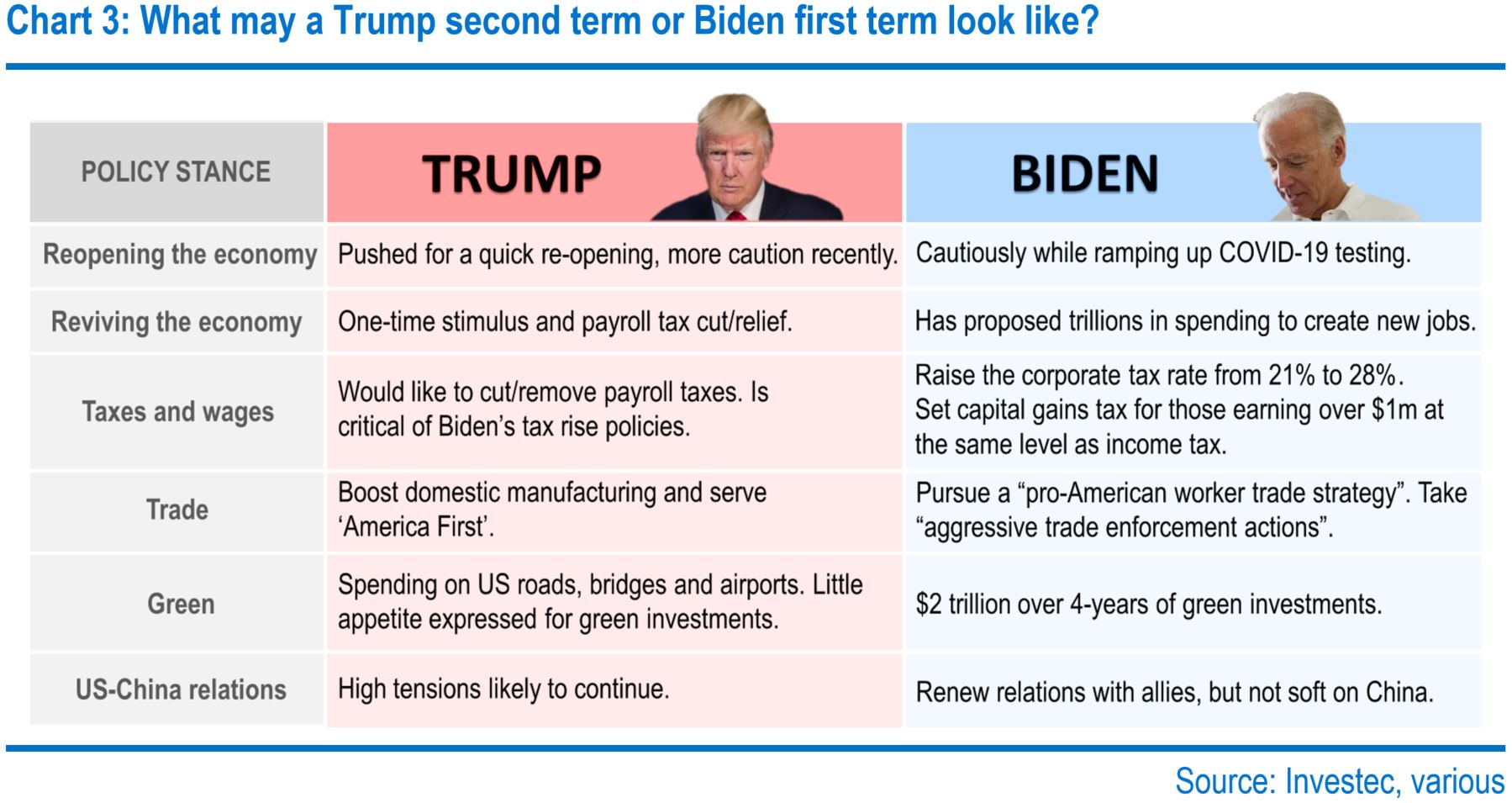

Current polling shows Biden is ahead in Florida, Wisconsin, Michigan, Pennsylvania, Arizona, Ohio and in Nebraska’s second congressional district - Clinton lost these in 2016. If he won those states (and held those Clinton won), he would have 352 of the 538 Electoral College votes. Chart 3 summarises Mr Biden’s key policies, where his tax pledges could have significant ramifications for investor sentiment. However, one question is whether he might be limited by Congressional opposition. The battle for Senate control looks tight, with RealClearPolitics currently putting the Democrats at 44 seats, the Republicans at 46, and 10 seats too close to call.

Eurozone

Official Eurostat figures highlight the extent of the economic shock in the second quarter, with GDP falling 12.1% quarter-on-quarter (QoQ), by far the largest decline in history. Outside the current crisis, the sharpest drop was -3.1% in the first quarter of 2009. However, the performance did vary across the euro area, with Spain at the bottom of the pack (-18.5%) and Finland at the top (-3.2%). What is apparent is that the stringency of the lockdown measures during the quarter had an evident influence on the severity of the second-quarter GDP shock. In terms of the outlook, one question is whether the reverse will be true. If that were to be the case, it would suggest that France could be one of the top performers of the major EU19 economies in the third quarter given that it has seen the most significant relaxation in stringency so far. But this is met with a degree of uncertainty given the backdrop of rising infections.

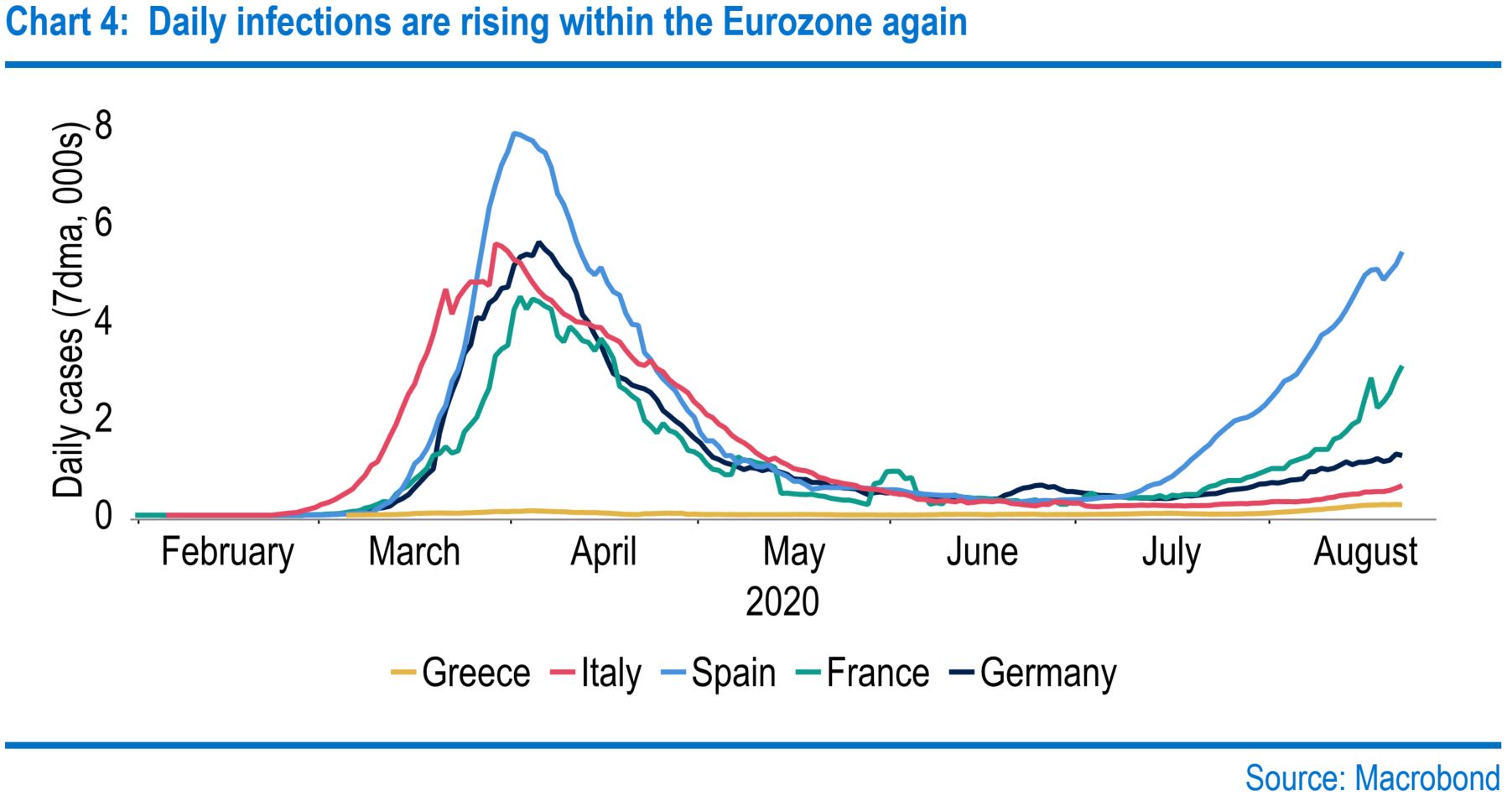

With earlier restrictions being lifted and more social interactions taking place, a rise in cases was to be expected. But the increase in certain countries, most notably Spain and France, is worrying and fuelling concerns over a broad-based and material second wave across Europe. From a growth perspective, what is important is whether wholescale lockdowns are reintroduced. So far, this has been avoided in favour of more localised measures. However, at some point, the level of cases may become unpalatable for governments prompting more stringent restrictions, damaging activity again.

There are early signs that the recovery is at risk. Having risen sharply from April’s lows, the Eurozone's Purchasing Manager Indexes (PMI) witnessed a retracement in August, with the Composite PMI falling back to 51.6 from 54.9 (a reading below 50 indicates contraction and one above growth), with the re-emergence of rising infections being cited as a critical factor. That still points to the economy expanding but suggests that the pace of recovery could be slowing. Currently, our forecasts envisage a 10.2% QoQ rebound in euro-area third-quarter GDP, but this will be at risk should the Covid-19 data not begin to moderate soon. Consequently, our 2020 forecast stands at -7.2%, but with risks to the downside from a second wave. Our forecast for 2021 stands at +5.3%.

The European Central Bank (ECB) has played a crucial role in supporting the recovery by stabilising financial conditions. For example, household and corporate borrowing rates have remained steady around 1.4%. Meanwhile, annual corporate credit growth has firmed, increasing to 7.1% in June from 3% in February. Government loan guarantees and the ECB’s Targeted Longer-Term Refinancing Operations III (TLTRO III), which incentivises banks to lend to the private sector, have been supportive (1.3 trillion euros was drawn down in June). That has contributed to Eurosystem excess liquidity rising to 2.9 trillion euros, putting downward pressure on three-month Euribor, pushing it to a record low (-0.491%), and leading to a negative spread on the three-month overnight indexed swap.

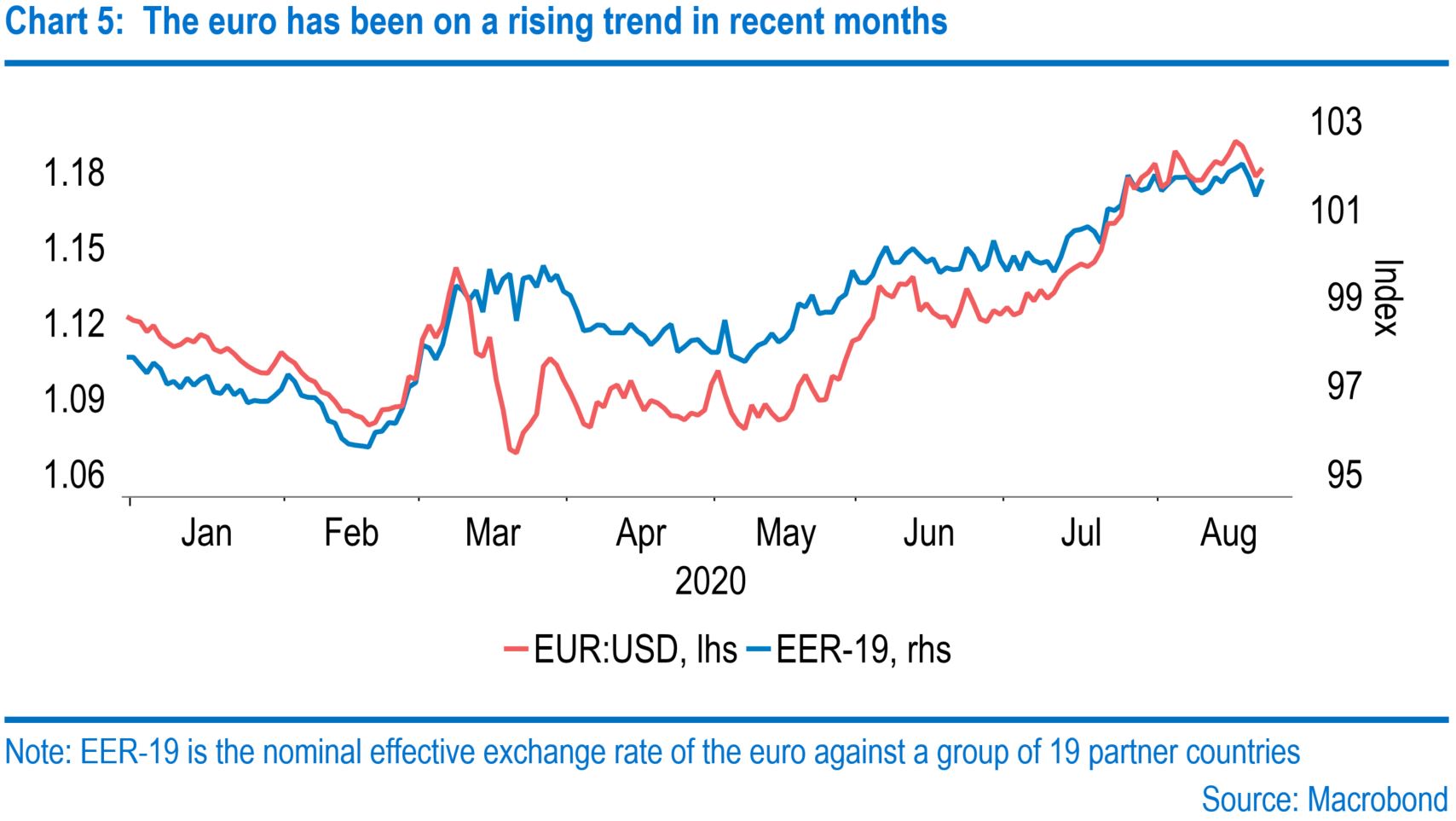

That suggests banks are reticent to hold the liquidity given it attracts the ECB's deposit rate of -0.5% and that future TLTRO drawdowns may be smaller as a result. However, excess liquidity is also driven by quantitative easing. The ECB is set to buy another 1 trillion euros of bonds over the coming year under the current policy stance, suggesting excess liquidity will continue to rise. Our baseline case envisages no further reductions in ECB policy rates, but the risks are clear given uncertainties over the economy and inflation. A related factor is that the euro has been strong, gaining 2% in trade-weighted terms over the past two months. Several factors have been at play, including dollar weakness.

Given this momentum, we have raised our forecast for where we see the euro at the end of the third quarter to $1.20. However, we suspect that the euro will give up some gains towards the end of the year (we see it at $1.17 at the end of the fourth quarter) as second wave fears intensify in the euro area. Our end-2021 forecast is also pushed up to $1.25. One question of late has been whether the dollar is losing some of its reserve currency status to the benefit of the euro. For example, Russia and China’s use of the euro in transactions with each other has risen to 30%, an all-time high. Near term, we see the dollar's position as the global reserve currency as secure since no other financial market offers depth and liquidity as the US. However, the long-term dynamic may change should China’s financial markets deepen and the European Union's historic recovery fund represent the first step towards a deep and liquid unified euro safe financial instrument.

United Kingdom

England's economy took the next step towards reopening this month after indoor entertainment was permitted to resume. But this came after a last-minute delay of a fortnight amid concerns Britain was at risk of a severe outbreak. Several factors must be taken into account to determine whether the virus is spreading. An obvious one is daily variation in the number of tests administered. But a less obvious cause of "caseflation" is individuals being tested multiple times. Additionally, a distinction must be made between the main four different types of test, as only two capture new cases. However, this data just covers England (and even then on a lagged weekly basis). But it does appear to suggest that infections have stabilised in recent weeks.

How does this compare to other countries? It is difficult to say due to the different testing regimes and calculation methods. But one thing that is clear is that Britain has suffered one of the most significant economic tolls - GDP slid by 20.4% in the second quarter, the sharpest drop since records began in 1955. Taken with the 2.2% fall in the first quarter, this has left the economy some 22% smaller than its pre-pandemic peak, worse than any other Group of Seven country. However, the flipside of this is that the UK is likely to see one of the most robust recoveries over the second half of this year. In June, GDP climbed a record 8.7% as the phased reopening pushed forward.

It is also probable that the Bank of England delivers a further bout of stimulus, but the prospect of the central bank cutting interest rates below zero seems unlikely.

Surveys and real-time data suggest that July and August will see a continuation of this recovery. But for this to be sustained, more households will need to feel confident participating in leisure activities, with only four out of 10 adults feeling comfortable eating indoors. However, this looks to have improved on the back of the Eat Out to Help Out Scheme, with diner numbers above year-ago levels between Monday and Wednesday in August. Another priority is the return of schoolchildren in September, but it has been suggested that there may need to be trade-offs to achieve this, such as closing bars and pubs.

There are reports that Chancellor Rishi Sunak has made contingency plans to delay the next budget if there is a resurgence of Covid-19 in the UK. This is scheduled to take place in the autumn, close to the end of October when the Coronavirus Job Retention Scheme (CJRS) is set to be wound down. While the measure has helped to keep the jobless rate steady at 3.9%, other metrics show that the labour market is feeling the strain of the pandemic. Tax data shows that payroll employees have fallen 730,000 as of July. Also, total hours worked fell by a record 18.4% in the second quarter to levels last seen in 1994. But although Mr Sunak has ruled out an extension to the CJRS and plans to pivot towards putting the public finances on a sustainable footing, we expect him to set aside fiscal worries for the meantime and instead focus on limiting long-term economic scarring effects.

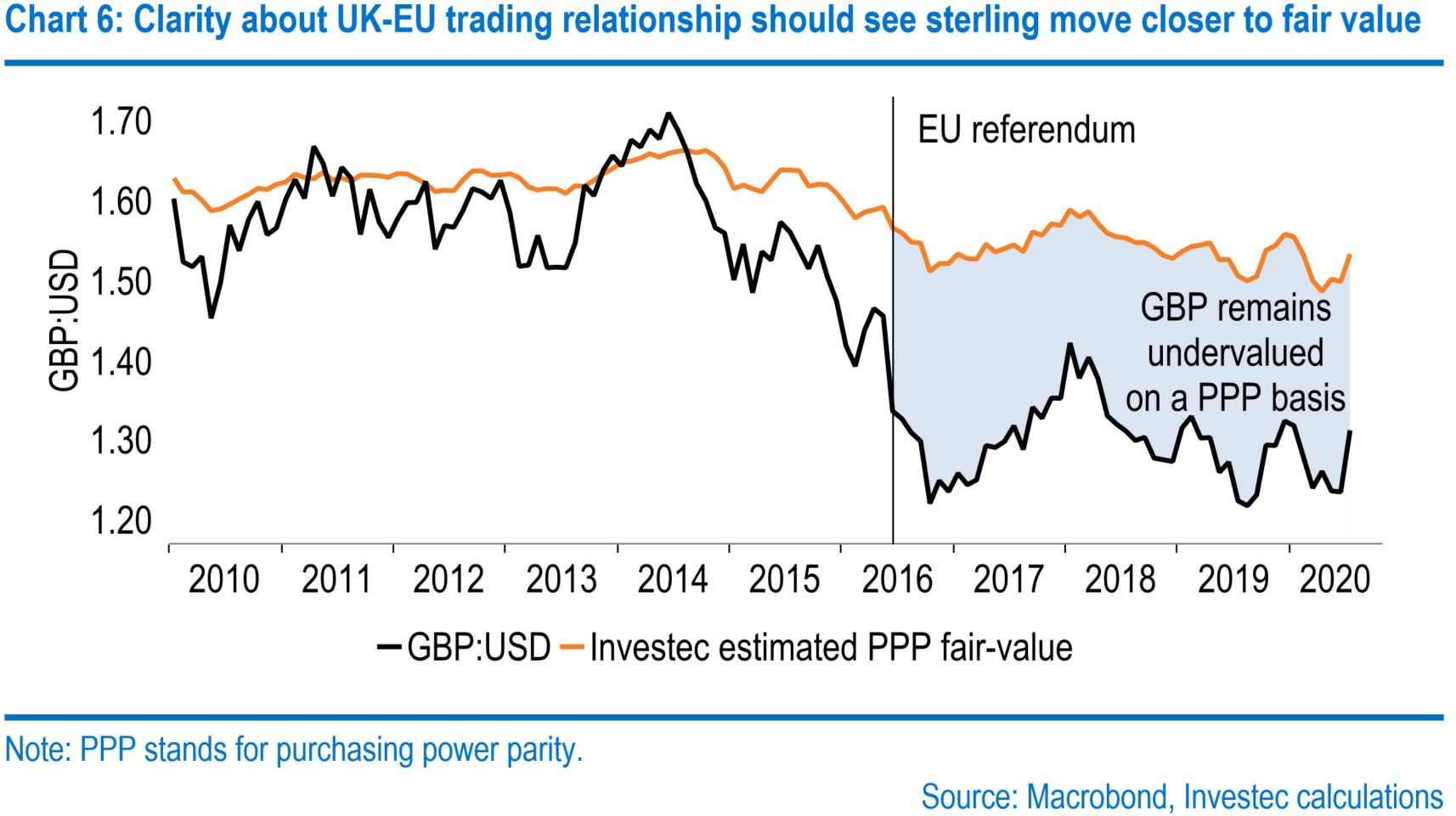

It is also probable that the Bank of England (BOE) delivers a further bout of stimulus, but the prospect of the central bank's Monetary Policy Committee (MPC) cutting interest rates below zero seems unlikely. Although the committee continually reviews the effective lower bound of interest rates, it concluded this month that negative rates could be "less effective" than other tools. Instead, a more likely course of action is another round of quantitative easing, potentially in November given that net asset purchases are set to conclude around the end of the year. In any case, the pound has been buoyed by the diminished prospects of negative rates as well as the global shift to risk assets. It now trades around $1.31, having stood at just $1.26 in mid-July.

But we expect sterling to return to those levels by the end of the third quarter as Brexit trade negotiations go down to the wire. After months of talks, the UK and EU remain at loggerheads over fishing rights and Brussels' demand of a "level playing field". Although this risks a cliff-edge Brexit on 31 December, extending the transition period is politically toxic for the UK. Instead, we still assume that talks will yield a bare‑bones deal, with a more comprehensive free trade agreement reached later. That should underpin a rise in the pound, with our end‑year targets having been raised by an expectation of further dollar softness and less talk of negative rates. We see cable ending 2020 at $1.34 (previously $1.28) and 2021 at $1.40 (previously $1.35).

Would you like to hear from our economists directly? Sign up to receive invites to our fortnightly economic Q&A with a member of our team.

Browse articles in