Despite some strengthening in a few survey indicators recently, momentum in the main developed markets is currently lacklustre. Indeed, it is touch-and-go whether or not shallow recessions have begun, under the weight of higher interest rates. We expect similarly challenging conditions to persist at the start of 2024 too.

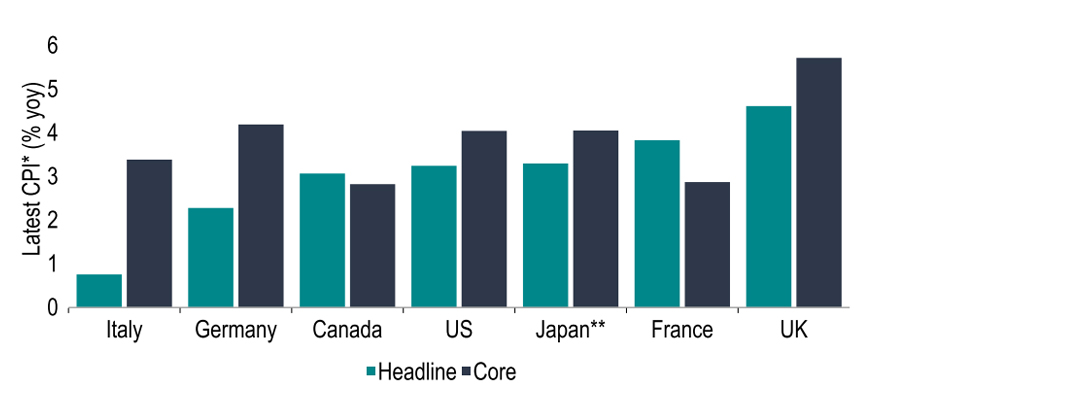

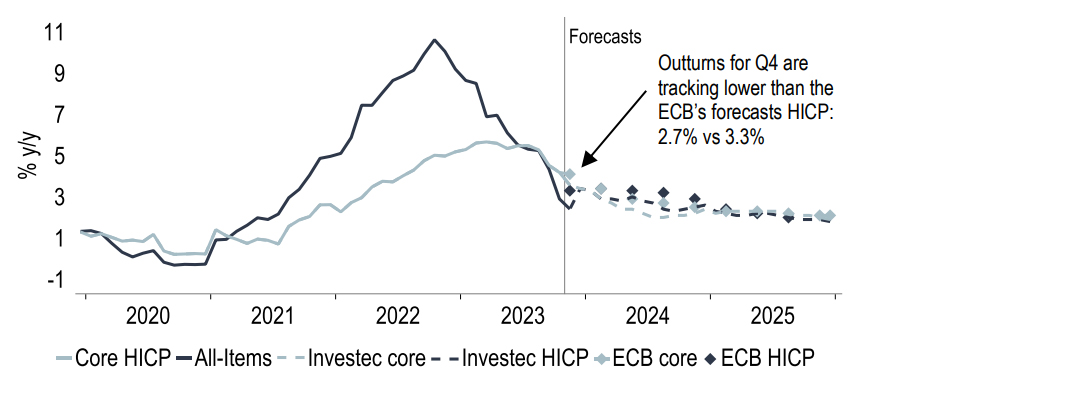

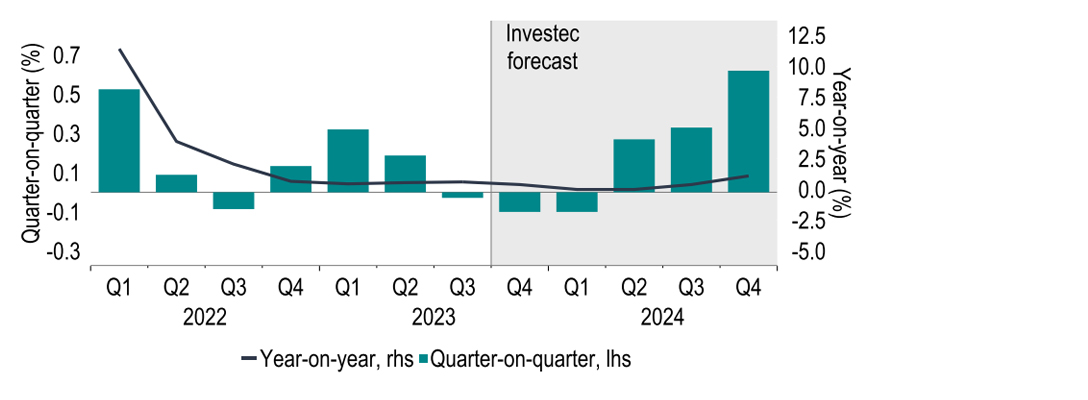

The better news, however, is that inflation has made substantial progress back down towards target – pleasingly to date without large job losses. Energy prices have been the key driver of that until now. This effect is now probably largely behind us. But encouragingly, core inflation has started to recede too, and to a greater extent than policymakers have forecast. A return to target inflation therefore seems in sight before long. As a result, a restrictive monetary stance looks less necessary.

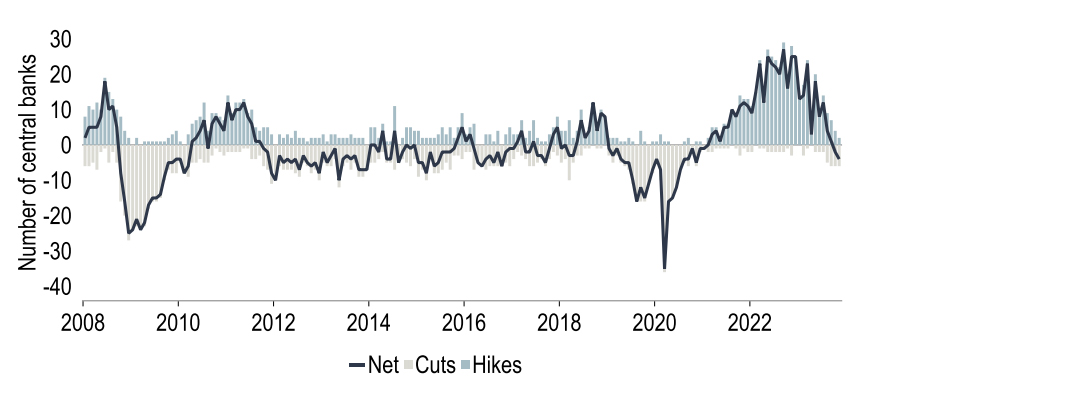

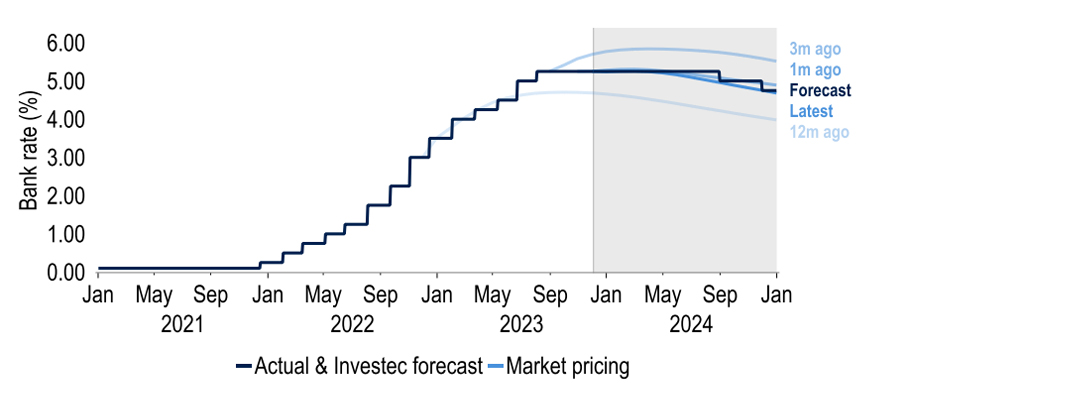

This has given rise to optimism in markets that over the course of 2024, interest rate cuts can spread from a handful of emerging markets, where they have already begun, to the major developed economies. We share this view. But we are mindful that the ‘last mile’ in bringing inflation down is set to be harder. Going as quickly and as far as now priced in seems a little too optimistic to us: we expect a relatively cautious start to policy loosening, with 75bps of rate cuts in the US and the Eurozone next year and only 50bps in the UK, where the fiscal stance has seen some pre-election loosening in the Autumn Statement. Indeed, amid high indebtedness, fiscal considerations could limit further falls in longer-term bond yields next year. Even so, a turn in the interest rate cycle should help set the conditions for a strengthening in growth momentum in H2 2024, along with the direct boost to purchasing power from lower inflation itself.

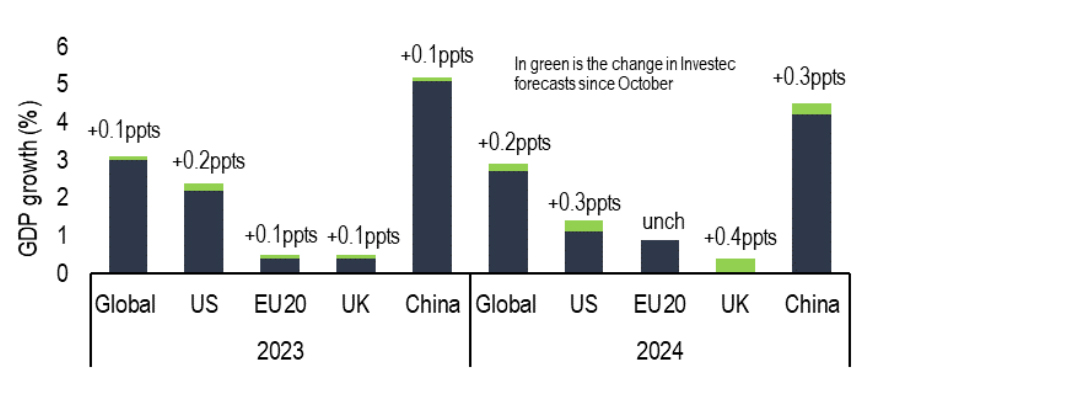

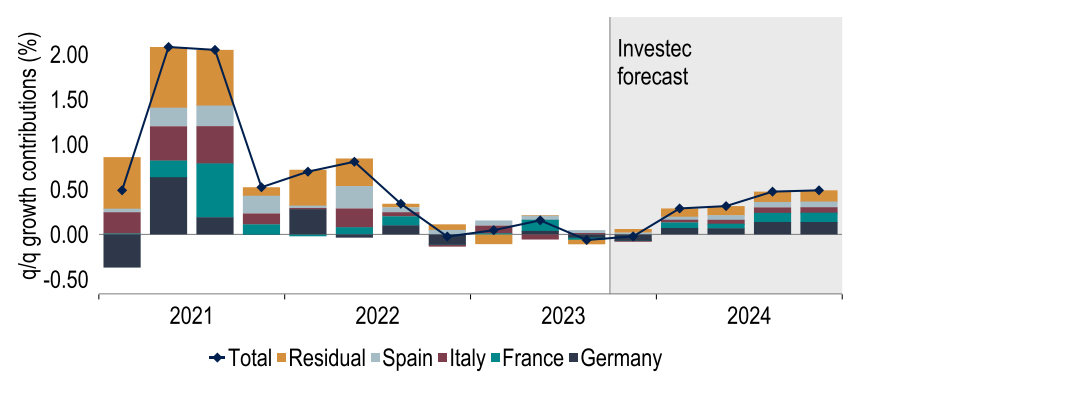

We are looking for global growth of 2.9%, down from 3.1% this year. But this masks an acceleration in H2 2024 as lower inflation and rate cuts boost spending power and investment

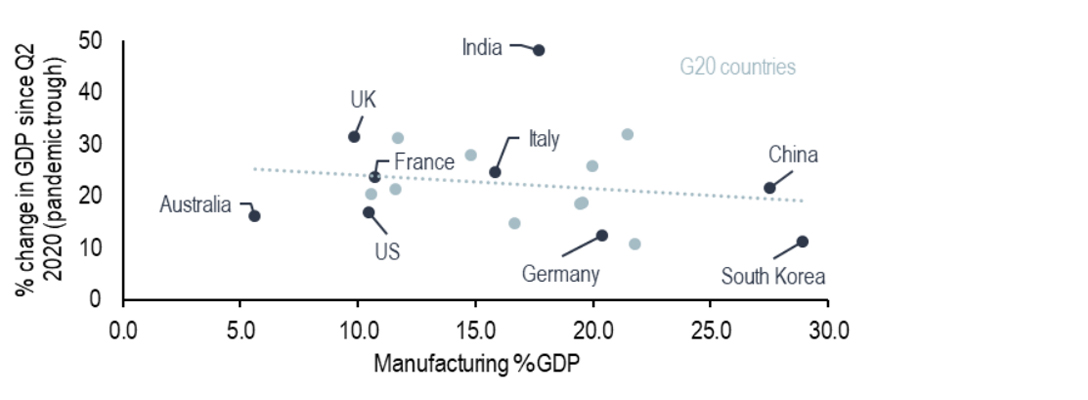

Stimulus measures by the authorities are likely to bear some fruit, but we suspect the rumoured 5% growth target may not be met in full as fiscal constraints on local authorities bite and competition in traded goods from a buoyant Indian economy is strong.

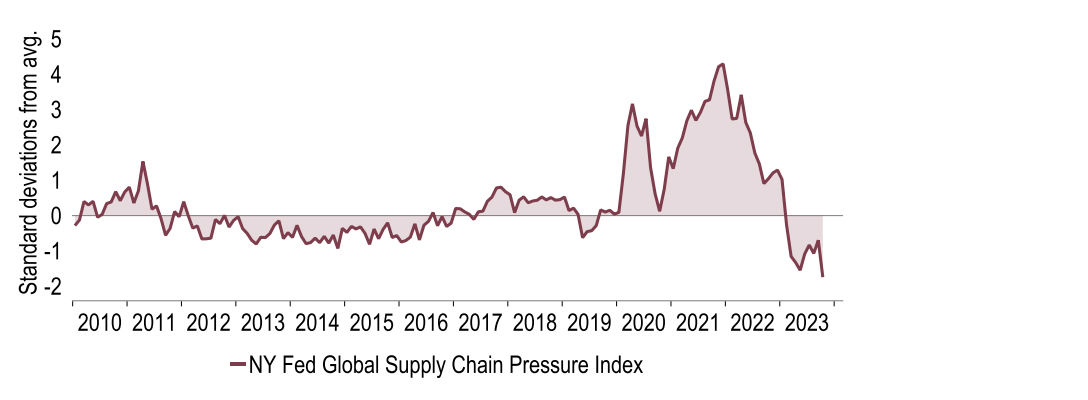

Improved supply chains and falling vacancies look set to bring a sustained return to target inflation within sight, helped by indirect effects of cheaper energy on core prices

Central banks likely want to proceed cautiously to begin with, absent an unforeseen crisis.

Uncertainty about neutral rates and fiscal concerns could limit declines in yields.

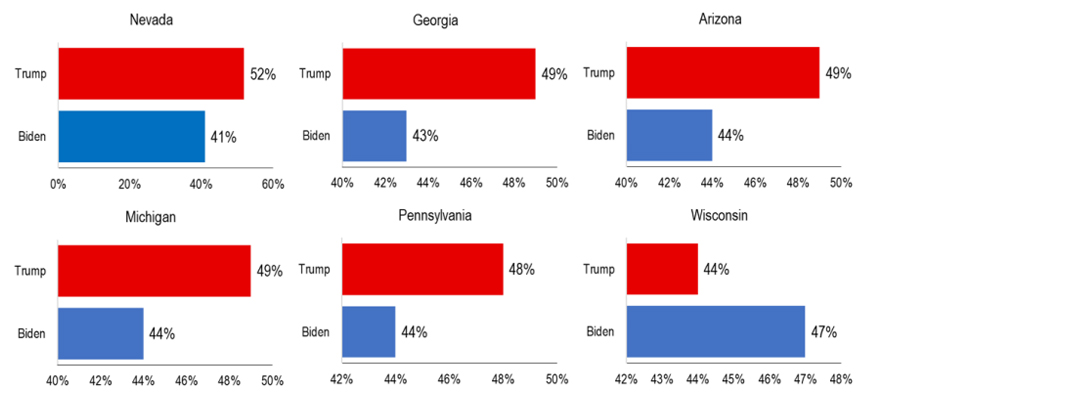

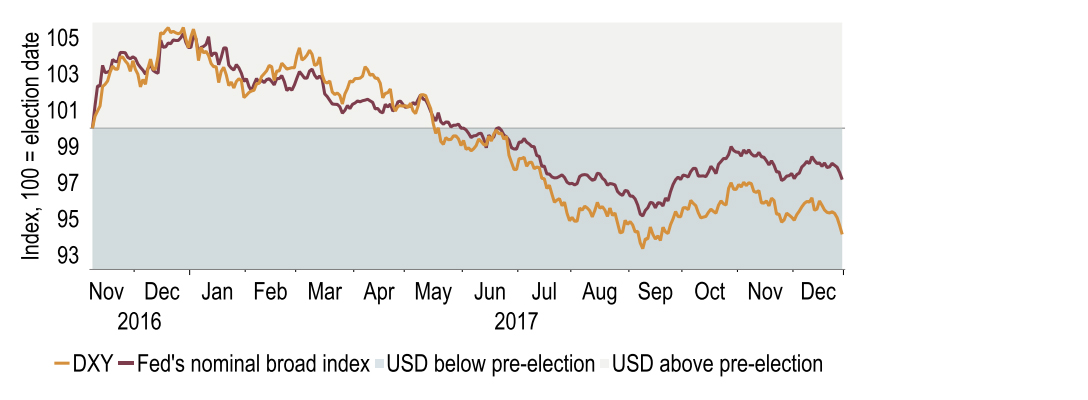

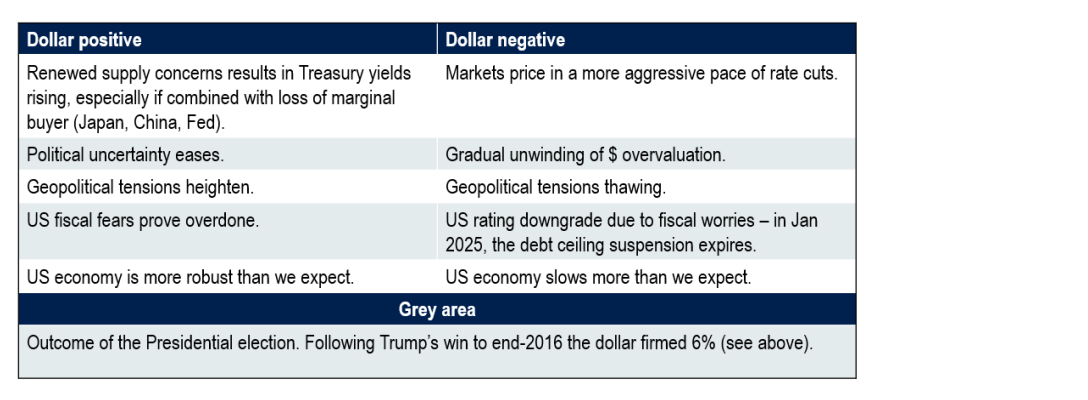

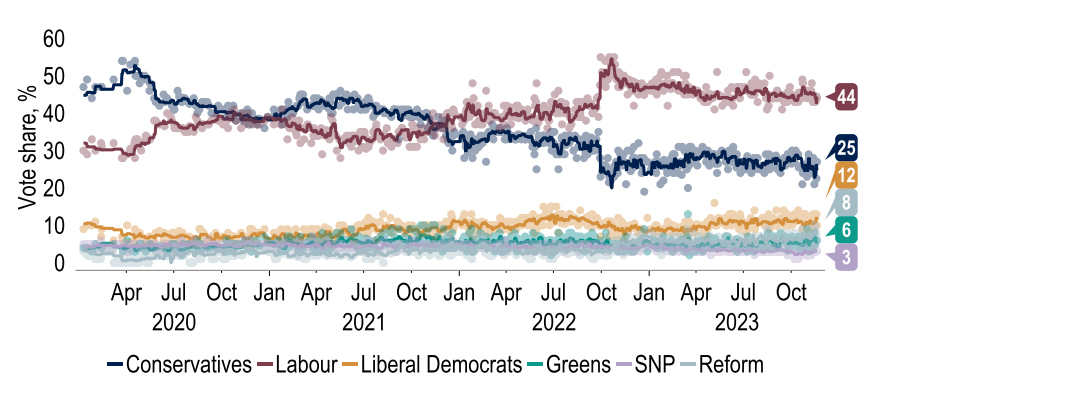

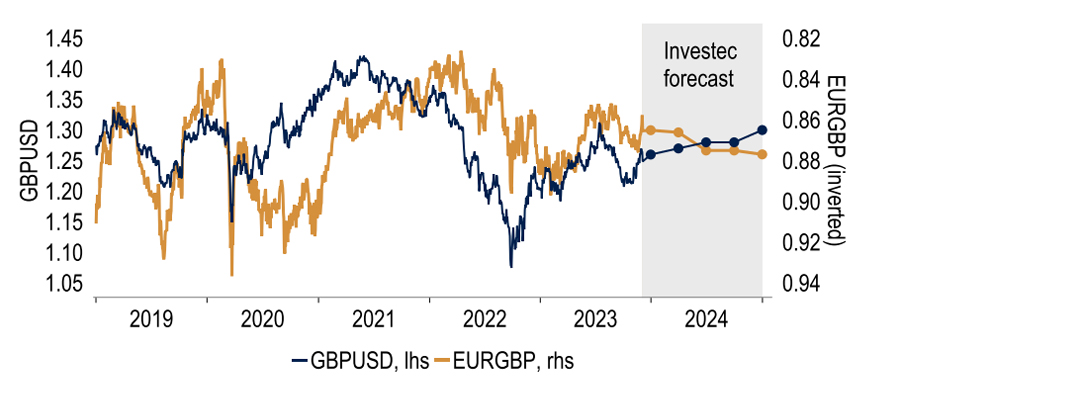

A potential wildcard are elections, chief among them the US Presidential election. Were Labour to win in the UK, the policy (and FX) impact may be limited.

For more information contact our economists

Philip Shaw

Chief Economist

I head up the Economics team for Investec in London after joining in 1997. I am a regular commentator on the economy and financial markets in the press and on TV. I graduated with an Economics degree from Bath University and a master’s in Econometrics from the University of Manchester. I started my career in the Government Economic Service at the Department of Energy before joining Barclays as an economist/econometrician.

Ryan Djajasaputra

Economist

In 2007, I joined Investec as part of the Kensington acquisition, before joining the Economics team in 2010. I provide macroeconomic, interest rate and foreign exchange analysis to Investec Group and its corporate clients. After graduating with a Bachelor’s degree in Economics from UWE Bristol.

Lottie Gosling

Economist

I joined the London Economics team at Investec as a graduate in September 2023. I graduated with a Bachelor’s degree in Economics from the University of Bath with a year-long placement working as an Economic Research Analyst at HSBC.

Ellie Henderson

Economist

I joined Investec in February 2021 as part of the London Economics team, providing economic advice and analysis for the company and its clients. Before joining Investec I worked as an economist for Fathom Consulting, where I predominantly focused on China research. I hold a Bachelor’s degree in Economics from the University of Surrey, as well as a Master’s degree in Economics from Birkbeck, University of London.

Sandra Horsfield

Economist

I am part of the London Economics team, having joined in 2020, providing macroeconomic analysis and advice to the Investec Group and its clients. I hold a Bachelor’s and a Master’s degree in Economics, both from the London School of Economics. I have over 20 years’ experience as a financial markets economist on the buy and sell side as well as in consulting.

Philip Shaw

Chief Economist

I head up the Economics team for Investec in London after joining in 1997. I am a regular commentator on the economy and financial markets in the press and on TV. I graduated with an Economics degree from Bath University and a master’s in Econometrics from the University of Manchester. I started my career in the Government Economic Service at the Department of Energy before joining Barclays as an economist/econometrician.

Ryan Djajasaputra

Economist

In 2007, I joined Investec as part of the Kensington acquisition, before joining the Economics team in 2010. I provide macroeconomic, interest rate and foreign exchange analysis to Investec Group and its corporate clients. After graduating with a Bachelor’s degree in Economics from UWE Bristol.

Lottie Gosling

Economist

I joined the London Economics team at Investec as a graduate in September 2023. I graduated with a Bachelor’s degree in Economics from the University of Bath with a year-long placement working as an Economic Research Analyst at HSBC.

Ellie Henderson

Economist

I joined Investec in February 2021 as part of the London Economics team, providing economic advice and analysis for the company and its clients. Before joining Investec I worked as an economist for Fathom Consulting, where I predominantly focused on China research. I hold a Bachelor’s degree in Economics from the University of Surrey, as well as a Master’s degree in Economics from Birkbeck, University of London.

Sandra Horsfield

Economist

I am part of the London Economics team, having joined in 2020, providing macroeconomic analysis and advice to the Investec Group and its clients. I hold a Bachelor’s and a Master’s degree in Economics, both from the London School of Economics. I have over 20 years’ experience as a financial markets economist on the buy and sell side as well as in consulting.

Get more FX market insights

Stay up to date with our FX insights hub, where our dedicated experts help provide the knowledge to navigate the currency markets.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.