Never mind the Brexit, here's the "Lockxit"

The coronavirus pandemic has tipped the world's major economies into their worst crisis since the Great Depression, with the global economy forecast to shrink almost 4% this year. While some countries edge toward reopening their economies, reversing the lockdowns too early raises the risk of a second wave of infections. The Investec economics team set out their latest estimates in this month's Global Economic Overview.

The global daily death toll from the coronavirus now seems to be in decline, with several countries unwinding elements of their lockdowns. Risk asset markets have rallied from their late-March lows, on the expectation of a return to global economic growth, despite the still unknown severity of the downturn and uncertain strength and timing of recovery. While fears of a "U"-shaped recovery seem too pessimistic, we still judge that the unprecedented drop in activity expected in the first half of this year is unlikely to be reversed by the end of 2021 in developed economies, thanks to "economic scarring". We now see a much sharper fall in global GDP over the first half, and though matched by a more robust rebound in the second half, we have slashed our 2020 forecast to -3.9% (from -0.5%), but raised our 2021 estimate to +6.5% (from +3.9%). We are aware though that reversing lockdowns too early could result in a sharp "second wave" of the virus.

The daily rise in US Covid-19 cases has offered glimmers of hope as new daily cases edged lower ahead of the rise in testing. Across America, the easing in lockdown restrictions is coming in a variety of forms and often sooner than official guidance implies they should. Even so, Donald Trump feels the pressure to get the US economy fired up again, with continuing jobless claims at more than six times the long-term average six months ahead of an election. The suddenness of the economic shock presents an enormous challenge, not least for the administration where support has not met demand fast enough. For 2020, we now see US GDP falling 5.6% (previously -3.9%) and rising 4.4% in 2021 (previously 2.5%). We re-iterate that the road back to pre-crisis GDP levels will not be short.

Four weeks ago, Europe was cited as the new epicentre of the coronavirus, with particularly acute outbreaks in Italy, Spain and France. However, restrictions implemented in March now appear to be bearing fruit, with a gradual relaxation of lockdown rules being announced. Nonetheless, a significant amount of economic damage has already been done, with surveys and data pointing to an unprecedented sudden stop in the economy. We now anticipate a sharper economic downturn in the first half of 2020, with a peak to trough fall in GDP of 15%, before rebounding in the third quarter. We now see the region's economy contracting 8% this year before growing 5.5% in 2021. Meanwhile, our forecasts for euro-dollar remain unchanged at $1.10 by the fourth quarter and $1.12 by the fourth quarter of 2021.

With infections appearing to have peaked, a gradual easing of the lockdown now looks to be on the cards. But the restrictions seem to be inflicting a more severe economic impact than we envisaged. We now look for an 8.9% contraction in 2020 (previously -4.4%), followed by an 8.4% rebound in 2021 (previously +3.3%). Risks to the outlook remain skewed to the downside, albeit mitigated by the UK Treasury’s proactive approach. We see its decision to temporarily tap the “Ways and Means” facility at the Bank of England as prudent given the strains in financial markets rather than as monetary financing. The Ways and Means facility is not new – it was part of the BOE’s original charter in 1694! Sterling’s recovery over the past month has caught us by surprise. We have raised our end-2020 forecast to $1.26 and 87 pence per euro from $1.20 and 92p.

Global

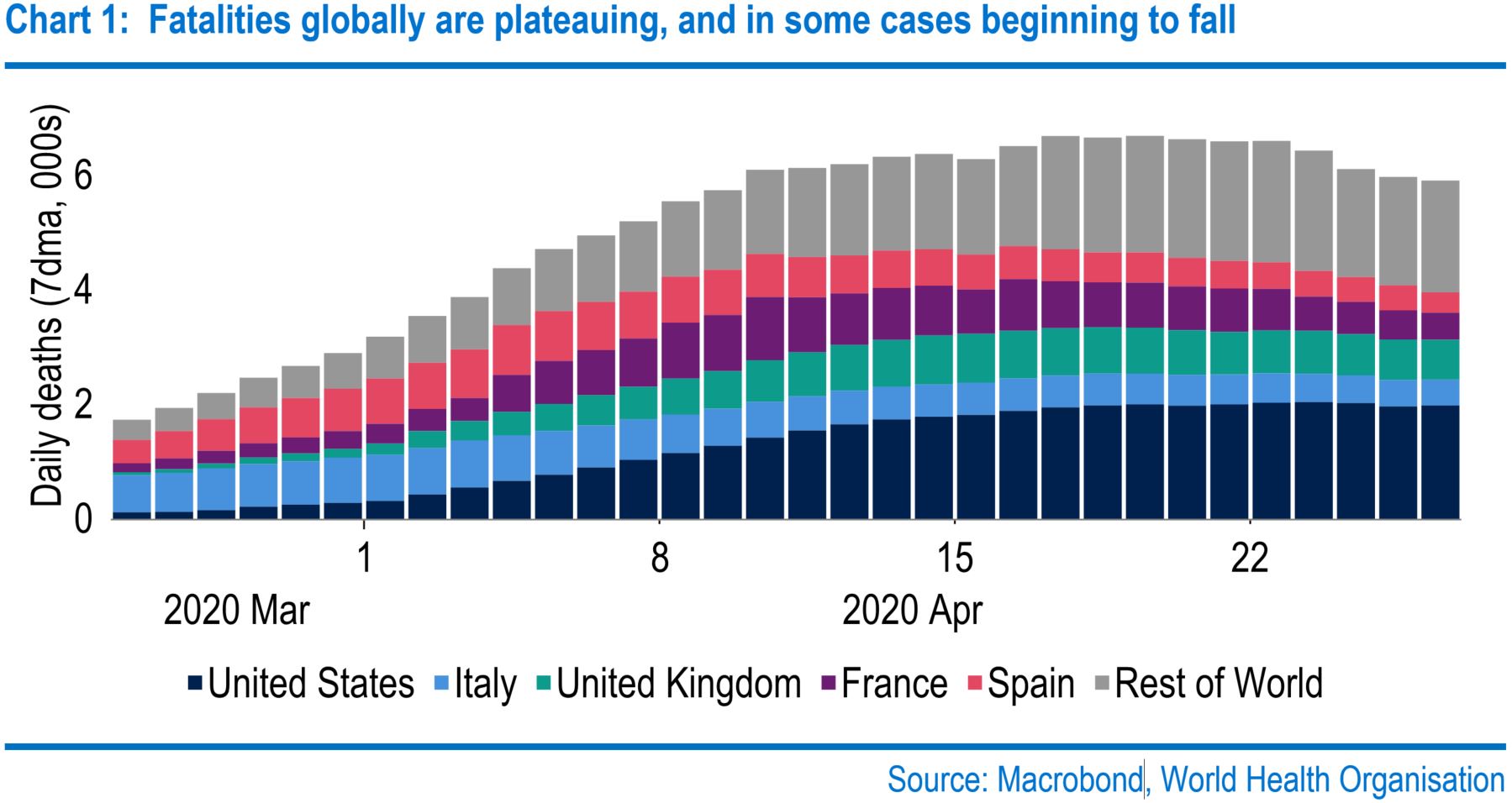

Covid-19 continues to dominate the headlines worldwide. Infections rose from 1 million to 2 million in just two weeks, with the count currently just above 3 million. Coronavirus-induced fatalities are somewhat of a lagging indicator to confirmed cases, but still carefully watched. Chart 1 shows that the daily death (seven-day moving average) curve has flattened, with tentative signs that the peak has passed. Indeed, some of the hardest-hit countries are beginning to reopen their economies, including Italy, Spain and several other European nations. Despite some worries of a second wave in South-East Asia, these encouraging signs have hoisted markets higher, albeit with some quirks.

The flattening of the various curves, plus a limited unwinding of lockdowns in Europe have fuelled significant rallies in stock markets. At the time of writing, the MSCI World Index had recovered by 24% from its late-March lows. But investors are mulling various paths forward, such as the timing and extent of the relaxation of restrictions and the length of time that factors such as continued social distancing will be enforced (and the resulting economic consequences). With releases of first-quarter GDP data globally getting underway and the publication of surveys for April yielding some clues on the extent of the downturn, what markets have more in mind is the timing, speed and the extent of the recovery.

A related point concerns shockwaves arising from the sheer rapidity and scale of the plunge in activity. We note the surge in rice prices as consumer preferences shifted towards non-perishable foods. Another has been the involuntary stockpiling of US crude oil and the erosion of available storage facilities. Last week, the front West Texas futures contract traded at -$40 per barrel intraday. It is difficult to foresee these situations of specific, idiosyncratic collateral damage. But we guess that we may expect several more before we have moved through the current crisis, which may add to investor risk aversion.

We now have Chinese first-quarter GDP data, which showed a 9.8% quarter-on-quarter (QoQ) fall, close to our expectation. Industrial production figures for March hint at a rebound during the month - the annual decline eased to 1.1% from January-February’s 13.5%. But two points suggest caution. First, at -15.8% year-on-year (YoY), March’s retail sales were very soft. The danger flagged here is that ongoing coronavirus fears restrain Chinese consumers for some time. Second, China is reopening its economy at the weakest point in recent global history, curbing the ability of exports to drive the recovery. The second quarter should see a modest rebound. Even so, we have lowered our 2020 GDP forecast down to -0.3% from +0.1%.

Governments in the US and Europe will look very hard at what to unlock, when and how. Rising social interaction may well reignite Covid-19 cases (and deaths). But the aim may be to contain another outbreak to manageable levels and avoid the need for subsequent full-scale lockdowns. How this is done makes a difference. Studies of the 1918 Spanish flu epidemic (which killed up to 50 million people globally) show varying fatality patterns across US cities. For example, New York enforced quarantines early and achieved a mortality rate of 60% of that of Philadelphia, which acted later. And though St Louis’s death rate was low overall, the city suffered a sharp second wave after it eased its measures.

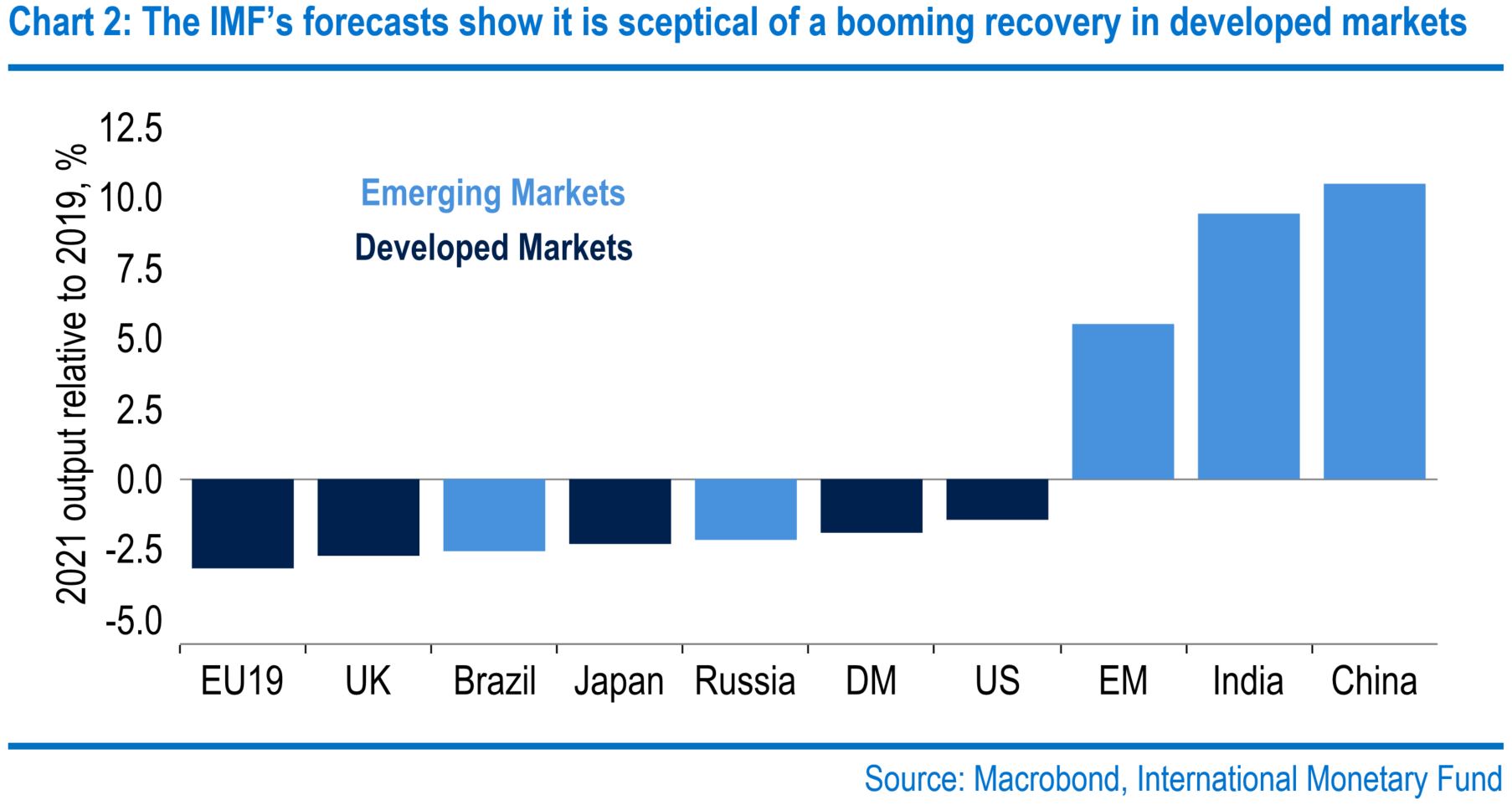

This is not a 1930s or 2008-type situation, given the relative health of banks. World output should recover as lockdowns are eased and a true “U”-shaped trajectory, i.e. activity bumping along the bottom, should be avoided. The critical question is the extent of the upturn. The nature of the current crisis carries its own risks, and we expect economic scarring from business failures, unemployment and perhaps idiosyncratic factors as well. We now forecast a global contraction of 3.9% this year followed by a rebound of 6.5% in 2021, (previously down 0.5% and up 3.9%). The International Monetary Fund’s latest forecasts are similar and make the same point as we do, in that growth in developed economies next year is unlikely to reverse this year’s decline.

United States

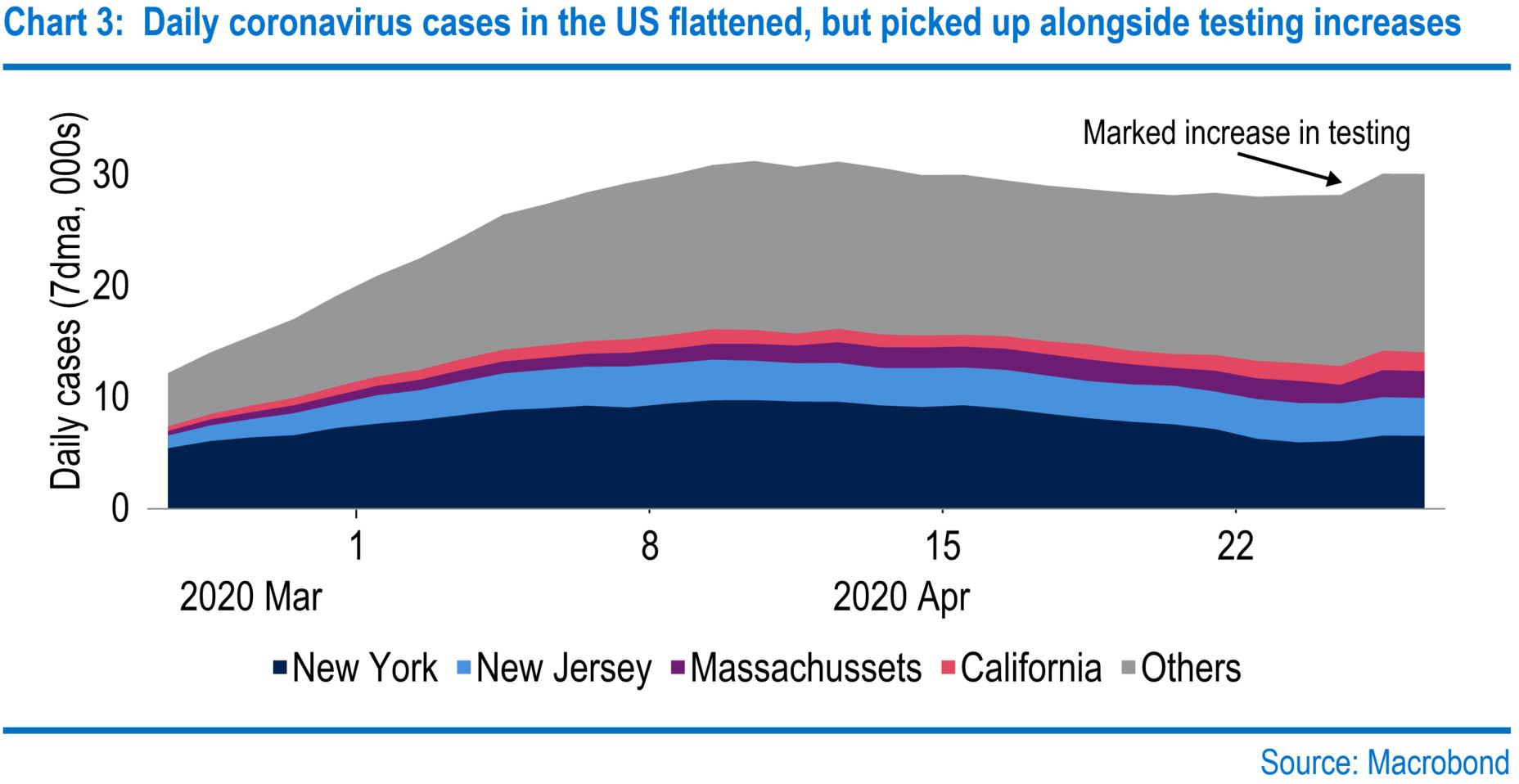

The total number of Covid-19 deaths in the US is alarmingly high, with the total above 50,000 and the most recent 26 April daily rise at 1,184. However, there are glimmers of hope; new cases were edging down ahead of the past week’s step up in testing. The evolution of case totals varies across states, but this trend has been visible across the US overall.

As state governors have sparred with President Donald Trump, it has become increasingly apparent we will see many variations in easing restrictions which will likely trigger a divergence in the state-level case curves over the weeks ahead. The risk of mismanaging the easing of restrictions was laid bare in Kentucky, where, following protests against restrictions, the state saw its highest spike in coronavirus cases. President Trump’s guidance is that states should wait until there is a “downward trajectory of documented cases with a 14-day period”.

However, some of the hardest-hit states have indicated they don’t plan to follow Mr Trump’s guidance with some planning to coordinate bilaterally. The surging number of jobless claims shows why economically Mr Trump is focused on getting a grip on re-opening plans, with the total number of continuing claims at 16 million, more than six times the long-term average. This is an incredible concern in itself but for a president, just six months ahead of an election, and one that will need to be addressed fast.

Mr Trump may be worried that the longer the disruption persists, the greater the economic scarring will be. This is likely true, but the speed of the decline presents an unprecedented challenge. The US administration’s $2.3 trillion fiscal package will no doubt limit some of the damage. Still, the rapidity of the disruption has meant support in some areas has not met needs fast enough, while questions have been raised over scheme design. One such example was the $350 billion Paycheck Protection Program, where the pot ran dry amid reports that the take up by large companies has left small firms without access to the funds. Indeed, data showed that nearly half the cash was in loans over $1 million.

The administration has since set more aside, but for some, the worry is that it arrived too late. The speed of the economic decline is laid bare in the data releases starting to come through. March was a month only partly affected by social distancing and lockdowns, yet retail sales saw the biggest monthly fall since records began and industrial production the largest drop since 1946. April will be much worse. In light of data steers, we have taken another knife to our first- and second-quarter GDP growth forecasts. However, we have lifted our forecast for the rebound in the second half. For 2020, this puts our US GDP forecast at -5.6% (previously -3.9%) and 2021 at 4.4% (previously 2.5%). Nevertheless, we re-iterate that the road back to pre-crisis GDP levels will not be short.

The fiscal consequences of the coronavirus and the measures deployed imply we can expect to see lower interest rates persist over the medium term.

The Federal Reserve has moved to what feels like maximum accommodation with Chair Jerome Powell saying we are “doing all we can”. The extent of the economic shock has led to a hugely extensive policy response from the Fed with the central bank taking the Funds Rate back down to 0-0.25%, shifting to open-ended quantitative easing (QE) and adding a flurry of other measures to deal with strains across a swathe of markets. The Fed may well tinker with these as needs and pressures change, but this stance is likely to remain broadly steady now until the recovery is strong and consistently underway. A caution here is likely to be reinforced by uncertainty over the shape of the recovery, which may well not be smooth amid further potential waves of coronavirus cases and additional restrictions.

This means we are likely to see the Funds Rate held at its current low for the foreseeable future. The fiscal consequences of the coronavirus and the measures deployed also imply we can expect to see lower interest rates persist over the medium term too. The Committee for a Responsible Federal Budget’s projections show an enormous leap in borrowing this year with unwelcome consequences for the US debt trajectory; debt is forecast to exceed the size of the economy this year. In light of fiscal pressures and the need to stabilise debt, monetary policy will need to provide some offsetting support to boost demand for a time.

Eurozone

Four weeks ago, Europe was labelled as the new epicentre of Covid-19. Euro-area nations are now pioneering the return to “normality”, seeking to find the right balance between the economic fallout and the risk to health. Italy and Spain, the hardest-hit European nations, have announced plans to reopen their economies over the coming months gradually; a host of other Eurozone members are following a similar path. The seven-day moving average of daily diagnoses in Austria, Italy, Spain, France and Germany plot an encouraging arching of the curve in the last few weeks. However, it may be some time before the economic data trough.

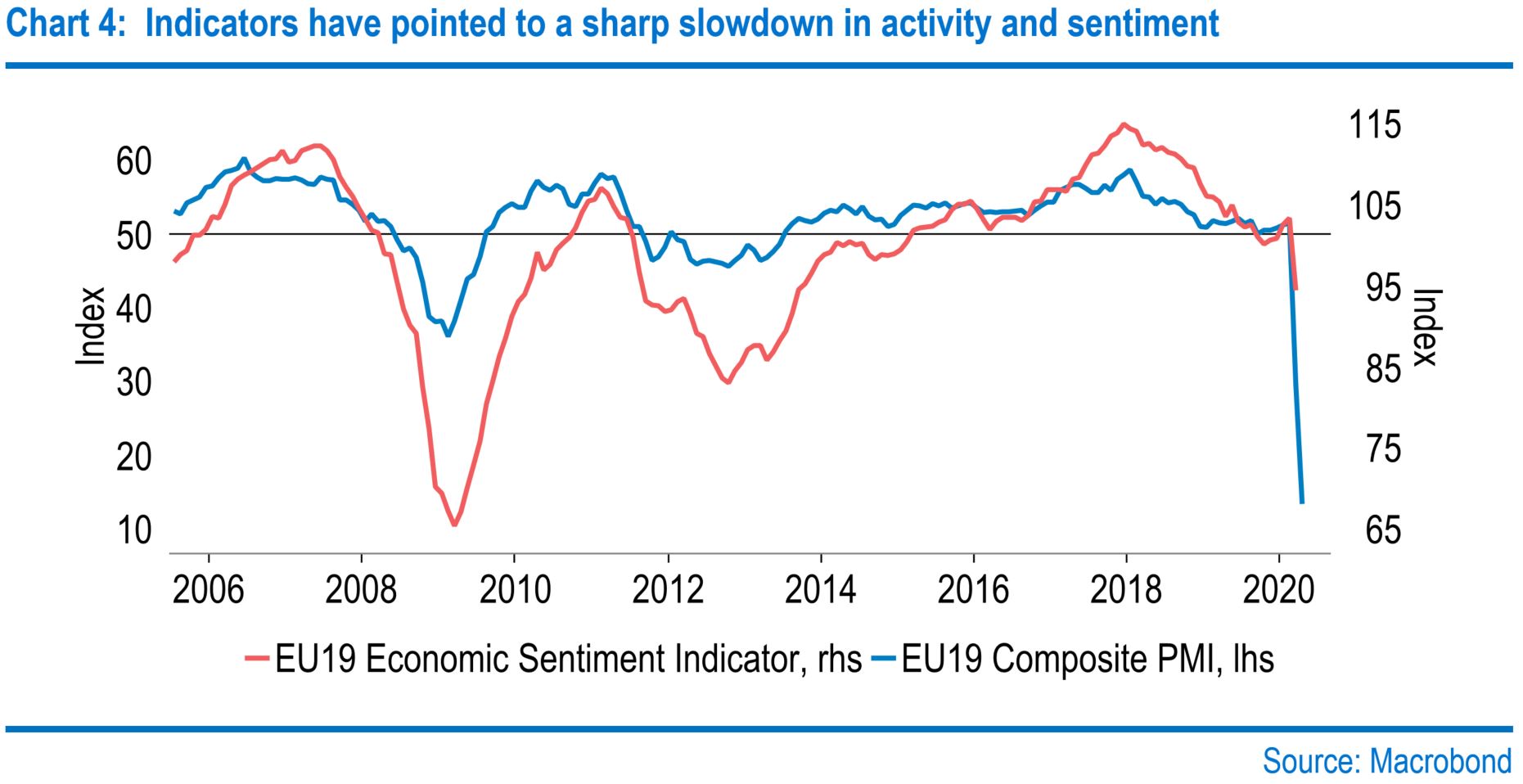

Clearly, a more limited period of social restrictions would be positive for the path of economic recovery. Nonetheless, significant economic damage has already been done, particularly given the speed of declines in activity, which are unparalleled in modern times. The region’s composite Purchasing Manager Index (PMI) stands at just 13.5 after witnessing a 39-point fall in two months. Limited official data is pointing to a similar picture within retail trade, with French retail sales falling 24% month-on-month (MoM) in March echoing the plight of the sector seen internationally. Chinese and US figures fell 15.8% YoY and 8.7% MoM respectively.

Retail sales figures sit alongside other survey evidence such as Eurostat’s Economic Sentiment Indicator, which registered its biggest monthly fall on record in March. Figures for April are likely to be worse. There are still big unanswered questions over how cases will evolve from here and how restrictions will be adjusted accordingly. As such, the shape of the economic recovery remains very much uncertain. At present, the very gradual relaxation of restrictions is broadly in line with our current view of economic activity returning to some form of normality in the third quarter and recovery after that. But the balance of risks remains clearly to the downside for our 2020 GDP forecast of -8%. One factor that could aid the recovery is a more unified fiscal response, via a jointly financed recovery fund, although differences remain over how funds should be dispersed.

In the month since the European Central Bank introduced the Pandemic Emergency Purchase Programme, financial conditions have stabilised after a deterioration to levels not seen since the Eurozone sovereign debt crisis in 2012. Corporate bond spreads have narrowed after reaching eight-year highs, while sovereign bond spreads have also retraced some of their widenings. This follows a big step up in asset purchases in March, with the ECB buying €94 billion. But perhaps even more notable is the flexibility the ECB has implemented over the share of each country’s bonds it buys. The central bank has focused on those countries with the most acute market strains in an apparent backtrack after ECB President Lagarde stated that the ECB was not there to “close spreads”. For example, the ECB share of Italian bonds purchased in March stood at 35%, more than double the 17% that it would usually buy given the capital key.

On a 12- to 18-month view, we see a recovery in economic fundamentals supporting euro-dollar, which we see going to $1.10 by the end of this year and $1.12 by the end of 2021.

While financial conditions have improved, they remain tighter than average and there remain some signs of money market stress. For example, the three-month London Interbank Offered Rate-Overnight Index Swap Rate (LIBOR-OIS) spread - a measure of the cost for banks to borrow - remains 28 basis points wider than pre-coronavirus levels at 30 basis points, an eight-year high. While the Euro Interbank Offered Rate (Euribor) spread has not reached sterling or dollar levels, it does point to some ongoing concerns over counterparty risk in the interbank market. These strains should ease as economic activity begins to rebound and with ECB policy remaining highly accommodative.

Despite other aggressive policy moves in March, the ECB has kept its Deposit Rate on hold, given the assessment that QE was a more appropriate response to market strains. However, we do suspect that the ECB will make one further 10 basis-point cut in the Deposit Rate to address a continued undershoot of the inflation target and almost record-low inflation expectations. We suspect the rate cut will occur in June, putting further near-term pressure on euro-dollar, which we see falling to $1.07 by the end of the second quarter. However, it should be noted that the euro is not universally weak, with the trade-weighted index actually up year-to-date, suggesting the move lower in euro-dollar has primarily been driven by dollar strength. On a 12- to 18-month view, we see a recovery in economic fundamentals supporting euro-dollar, which we see going to $1.10 by the end of this year and $1.12 by the end of 2021.

United Kingdom

Five weeks of lockdown appear to have succeeded in stemming the spread of the virus, with cases peaking around Easter. Attention has shifted towards easing the restrictions, but a premature move risks a big “second wave” and a resurgence in fatalities. Unwinding the lockdown is therefore likely to be gradual, meaning a full return to normality may be some way off for the UK economy.

Indeed, the Office for Budget Responsibility has published an illustrative scenario which is based on the current lockdown lasting for three months before being gradually being lifted over a further three months. It estimates this would cause GDP to contract by 35% in the second quarter and push the unemployment rate up to 10%. But activity bounces back quickly, bringing the rate of joblessness back down to pre-virus levels by 2023. The implications for the public finances are similarly enormous. Borrowing in the fiscal year 2020/21 would amount to 14% of GDP, the biggest single-year deficit since World War II, before falling back close to the OBR’s medium-term forecast.

A premature move risks a big “second wave” and a resurgence in fatalities. Unwinding the lockdown is therefore likely to be gradual, meaning a full return to normality may be some way off for the UK economy.

But though the analysis provides a useful yardstick, it makes the somewhat unrealistic assumption that there will be no lasting economic damage. In reality, there are limits to what fiscal and monetary policy can do to offset a downturn of the sharpness and severity of that signalled by the PMIs. However, these are unlikely to serve as a useful guide to the scale of the disruption. For one, they do not cover the retail sector, one of the most adversely affected industries, which accounts for 5.3% of the economy. But more broadly because they are diffusion indices and therefore do not measure the change in activity per se but rather how widespread an up/downturn is.

We suspect that the PMIs will underestimate the hit to second-quarter GDP, which now looks set to be more severe than we initially envisaged. Our forecast for 2020 GDP growth has consequently been lowered to -8.9% (previously -4.4%). But given that the shock is expected to be mostly transitory, we resultantly look for a more substantial rebound of 8.4% in 2021 (previously +3.3%). Risks to this outlook remain firmly to the downside, given the potential for second-round effects. Such concerns are shared by the BOE, which has wasted no time in restarting QE. It has bought an additional £69 billion of gilts to date (or 36% of those planned), nearly twice as fast as the previous record pace in May 2009.

Meanwhile, the Treasury has expanded the Coronavirus Job Retention Scheme; the cut-off has been moved back to 19 March and its expiration date delayed to the end of June. But the colossal amount of fiscal stimulus being provided needs to be funded, leading the Treasury to temporarily expand its overdraft-like “Ways and Means” facility (W&M) at the BOE. Some have labelled this as monetary financing. We disagree. The Treasury faces lumpy cash calls for its support schemes amid an uncertain revenue stream from tax receipts. The ability to fund these by drawing down from the BOE will help to prevent surges in gilt issuance, promoting market stability. Note that when the Treasury last tapped the W&M during the financial crisis, it reached a peak of £19.9 billion.

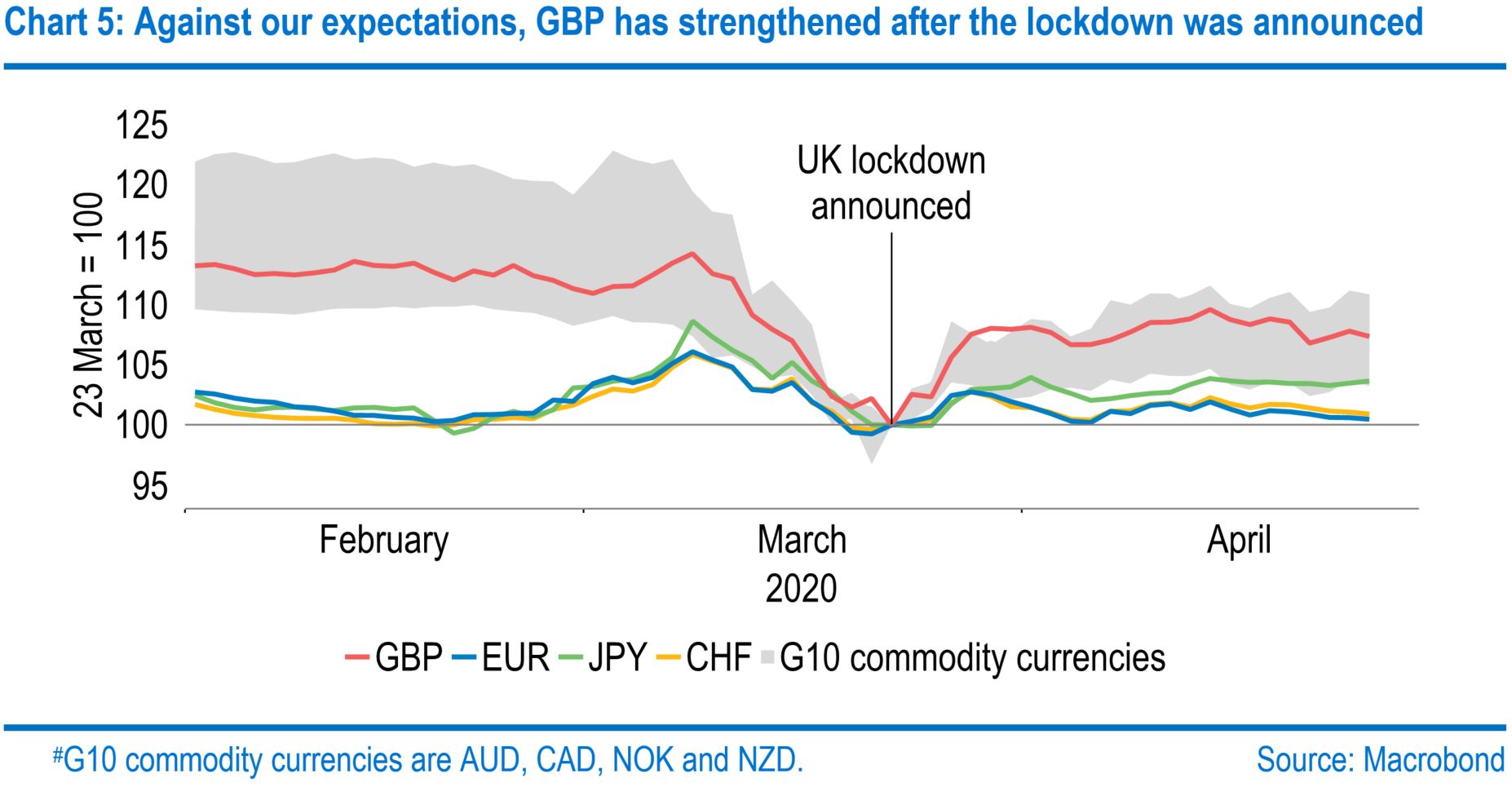

Still, it matters not what level the W&M reaches, but instead that it is returned to its current amount of £400 million as the Treasury HMT has pledged to do by the end of 2020. While the pound was little changed following the W&M extension, it has risen off its 35-year lows reached in mid-March. At the time, we assumed Brexit had meant the pound traded like a commodity currency (i.e. exposed to global trade fluctuations). But this looks to have been wrong. Instead, it appears to have been due to concerns about the UK’s initial response to the virus. Sterling has strengthened following the lockdown on 23 March to a greater extent than its Group of 10 peers. As a result, we have adjusted our forecasts. We now look for sterling to rise to $1.26 and 87 pence per euro by the end of 2020 (previously $1.20 and 92p).

Read more about how the spread of Coronavirus could affect you and your business

Browse articles in