Vaccines speak louder than words

One year after financial markets first woke up to the coronavirus pandemic, the rollout of vaccines has boosted confidence worldwide. We expect rapid global economic growth this year and next as the release of pent-up household savings unleashes demand. In our latest Global Economics Overview, we have increased our growth forecasts for the world, the US and the UK.

Despite decidedly mixed news on first-quarter output worldwide, the trend in market sentiment has been firmly upbeat in the past month. Driving this has been the expectation that pent-up household savings will unleash demand as vaccine rollout proceeds, helping to restore economic activity. Outside of the UK, it now looks as though the fastest growth may take place in the third quarter rather than the second quarter, but we have lifted our global gross domestic product growth forecasts for both 2021 and 2022 to 6.5% and 5.2%, respectively (previously 6.2% and 5.1%). However, we feel bond markets may have got a little ahead of themselves - central banks are unlikely to tolerate much more by way of yield rises as yet before intervening to keep financial conditions sufficiently loose to aid the recovery.

Congress is debating President Joe Biden’s $1.9 trillion pandemic relief bill. The Democrats are using a reconciliation bill to pass the package without Republican support. After three consecutive falls, retail sales rebounded by 5.3% in January, helped by stimulus cheques from the $900 billion stimulus bill at the end of last year. Indeed, fiscal policy should be a major driver of growth this year – we have raised our GDP forecast by 0.6 percentage points to 5.9%. Bond yields have continued to rise, signalling market jitters over inflation. We are inclined to the view that this is overdone. The official measure of unemployment hides significant slack in the form of marginally attached workers and misclassified individuals. The Federal Reserve is probably nowhere near signalling a tightening of monetary policy.

In the Eurozone, several themes have been evident over the last month. Clearly, the pandemic remains central, with the vaccine rollout - or rather the slow progress relative to other developed markets - a focus. This we suspect will result in a more significant pick-up in activity taking place in the third quarter. Our revised forecasts for annual growth now stand at 4.6% for 2021 and 5.2% for 2022. On the political front, former European Central Bank President Mario Draghi’s elevation to Italian Prime Minister and avoiding of an early election has been a highlight. His priority will be addressing the pandemic and finalising Italy’s Recovery and Resilience Plan. And while Draghi has an overwhelming majority, comprising all the main political parties, keeping such a government together over the full parliamentary term will be no easy feat.

Speculation persists over possible tax rises at the government's Spring Budget on 3 March. Meanwhile, GDP rose by 1% in the fourth quarter. Putting together the various moving parts, we have nudged up our view of 2021 GDP growth to 6.4% (previously 6.2%). The recovery looks set to be underpinned by the UK’s impressive vaccine rollout, enabling the economy to return to more normal conditions in line with the government’s latest roadmap. Indeed, the yield curve has removed the pricing of the risk of negative interest rates. That said, the Bank of England still plans to include this in its toolkit, which looks set to include a tiered system of bank reserve remuneration. Sterling has already risen beyond our end-year target of $1.40. It is the speed, rather than the direction, which is a surprise. For now, we are holding fire on changing our forecasts, leaving our end-2022 projection at $1.53.

Global

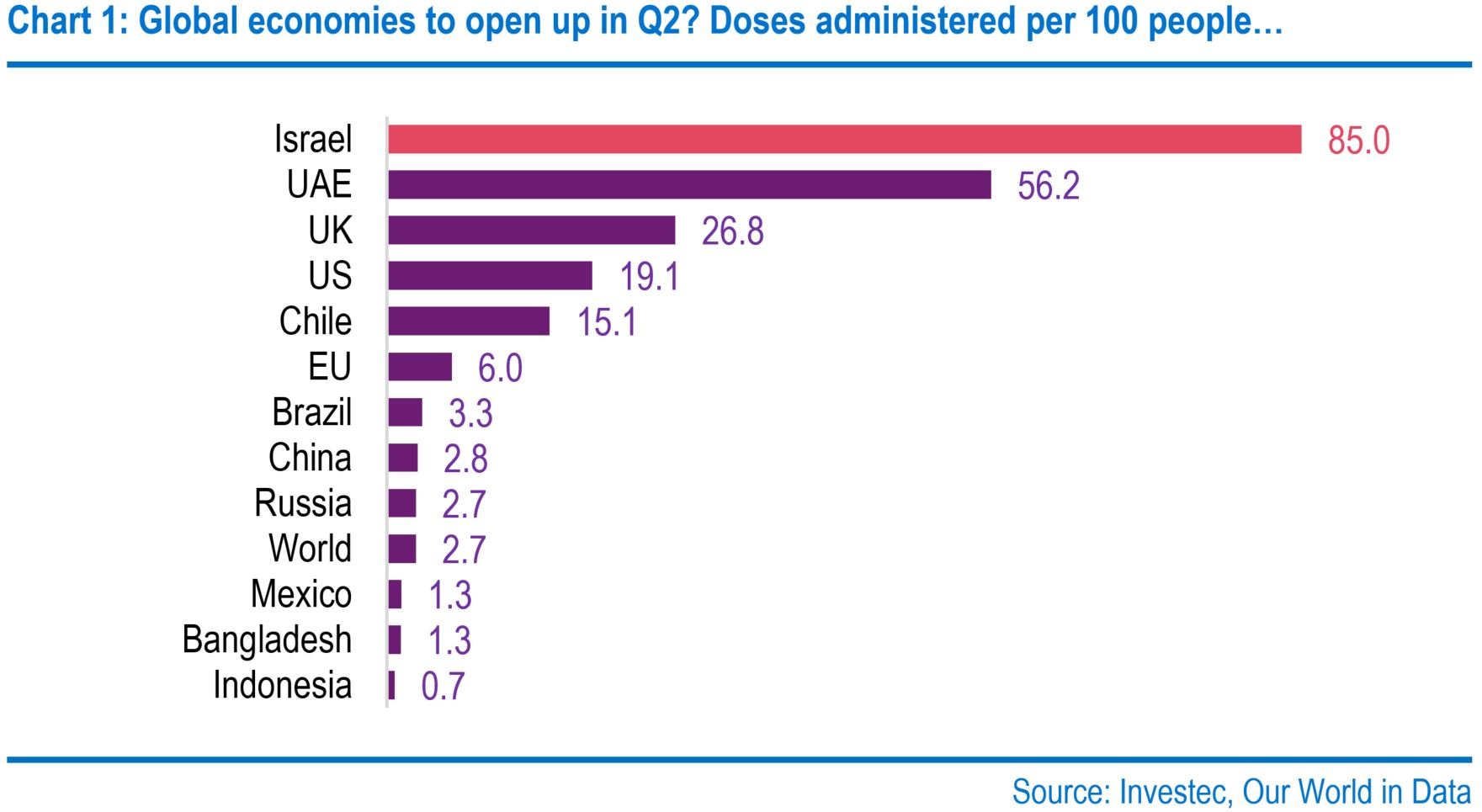

The vaccine rollout continues to gather pace globally, with Israel leading the way. The UK and the US are vaccinating rapidly, Chile is ahead in South America, and Singapore and China lead in Asia. After an initial slow start, vaccination rates in the European Union are starting to pick up too but are still modest. For now, governments worldwide continue to err on the side of caution about social restrictions, with stringent lockdowns in the UK and several EU countries holding back activity. But falling cases globally and increased vaccinations point to some loosening of restrictions and a rebound from the second quarter. As such, we pencil in global growth of 6.5% in 2021 and 5.2% in 2022.

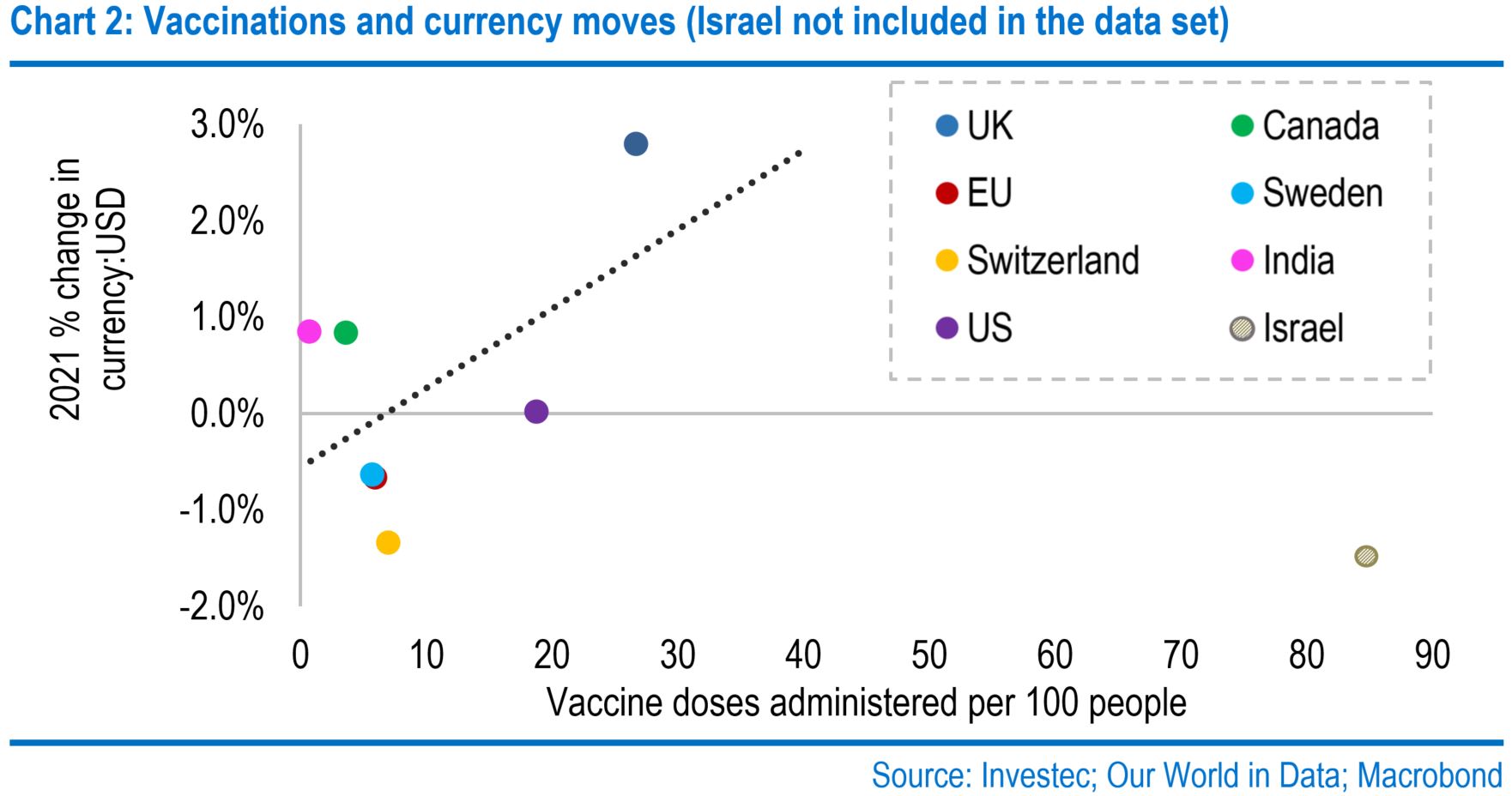

Since the turn of the year, vaccine rollouts, enhancing recovery prospects, have helped buoy market sentiment. It could be argued, tentatively, that currencies have reacted too - chart 2 shows that the US dollar has depreciated against the pound, the Canadian dollar and the Indian rupee, which may reflect a greater risk appetite. Meanwhile, the Israeli shekel has underperformed. But we note that vaccine rollout, although a key factor, will not be the only driver. For example, the pound may have benefitted from the UK’s free trade agreement with the EU, the BOE ruling out negative rates in the near-term, and a more supportive global equity scene. That said, it is worth keeping an eye open for further currency moves as vaccine rollouts ramp up.

Meanwhile, bonds have been catching some attention: US 10-year Treasury yields rose above 1.3% for the first time since February 2020, while gilt and Bund yields have been on the march too. This trend is evident in steepening yield curves as well - the spread between US 2-year and 10-year yields is now at its widest since 2017. The notion of a reflation trade remains the key driver of nominal yields, with inflation expectations contributing much of the rise, although real yields also ticked up in the last week. The expansion of US fiscal stimulus has been a key factor in Treasury moves and is likely to have lifted gilt and Bund yields. We suspect that vaccinations may also be a factor at play, mimicking the trends seen in currency markets. For example, the faster vaccine rollout in the UK likely contributed to the greater steepening in yields relative to Germany.

Aside from steepening yield curves, a further noticeable theme across major economies has been the acceleration in the stock of household bank deposits. With social restrictions initiating a change in spending patterns, and government support schemes protecting incomes, household savings have increased over the past year. In the UK, we estimate the magnitude of these "excess savings" to be 4.3% of 2020 GDP, with the US at 3.5% and the Eurozone at 1.8%. What is yet to be seen is how much of these extra savings will translate into consumer spending. The BOE assumes that 5% of the UK’s extra savings will be consumed, but there could be an upside surprise.

Turning attention to Asia, as one of the few economies to report economic growth in 2020, one may wonder whether China can help revive world economic activity. There certainly is a precedent for it: China played a dominant role following the 2008-09 global financial crisis, supported by large fiscal packages. Policymakers have refrained from large-scale stimulus this time. However, the economy has still managed to hold its ground, especially in terms of production, translating into China taking a larger share in global exports. The consumer economy has struggled to keep pace, but a recent strengthening suggests that modest gains are being made to enhance China’s role as an important global demand source.

Indeed, China is not the only nation in the spotlight, with several of its neighbours also experiencing economic success. Many southeast Asian economies have reported positive quarterly growth profiles in the latter of 2020, with the likes of Taiwan and Vietnam even managing to join China’s small club of economies that experienced growth over the course of 2020 as a whole. We expect these economies to continue their recovery into 2021, with emerging and developing Asia acting as a beacon of hope for global growth prospects.

United States

As with his first, former President Donald Trump’s second Senate impeachment trial also resulted in an acquittal - seven Republican senators voting to convict was insufficient for a two-thirds majority. Arguably more significant was the trial's short duration – just five days – freeing time to debate President Joe Biden’s $1.9 trillion pandemic relief bill. After a brief flirtation with bipartisanship, the Democrats have decided to go it alone to pass the package into law. Indeed, via the use of a "reconciliation bill", approval can be with a simple majority rather than 60 needed to overcome the filibuster. The final package's exact shape is uncertain, but we still view this as the key economic driver over 2021.

US GDP chalked up annualised growth of 4% in the fourth quarter, despite a subpar contribution from consumer spending. Indeed, retail sales fell back in each month during the quarter. However, recent data show the efficacy of fiscal policy - retail sales surged by 5.3% in January, thanks to $600 stimulus cheques to households, part of the $900 billion stimulus bill passed late last year. Our 2021 GDP forecast is now 5.9% (previously 5.3%). Indeed, the total earmarked fiscal stimulus is substantial - $1.9 trillion and $900 billion equates to 13% of GDP. Work on Mr Biden’s infrastructure package will start later in the year too. Moderate Democrats may insist on curbing its size, but even so, fiscal policy seems set to lend material medium-term support to the economy.

Despite the official unemployment rate falling to 6.3% in January, this may not represent the true extent of labour market slack. An alternative measure, known as U6, captures so-called "hidden unemployment’, such as those that have left the labour market due to discouraging job prospects and the underemployed. That suggests the true unemployment rate could be as high as 11.1%. The spread between the pair hit a record high in April 2020 as the pandemic took hold, but this has since narrowed. Although we believe U6 to be a better indicator of slack, there could still be unemployment unaccounted for, with US Bureau of Labor Statistics misclassifications on pandemic-related unemployment potentially further inflating U6 by an estimated 0.6 percentage points.

The January report also revealed that non-farm payrolls contracted by 6.1% annually. In terms of this contraction's sectoral composition, 40% of the fall can be attributed to leisure and hospitality, a sector decimated by ongoing social restrictions. The civil service also takes the lion’s share. However, this is skewed by the group's size, with government payrolls actually contracting by less than average at 5.5% annually. Conversely, the large contribution of private education and health services is significant. This is partly driven by a large drop in child daycare payrolls and a big fall in nursing and residential care facilities payrolls, which is perhaps more surprising.

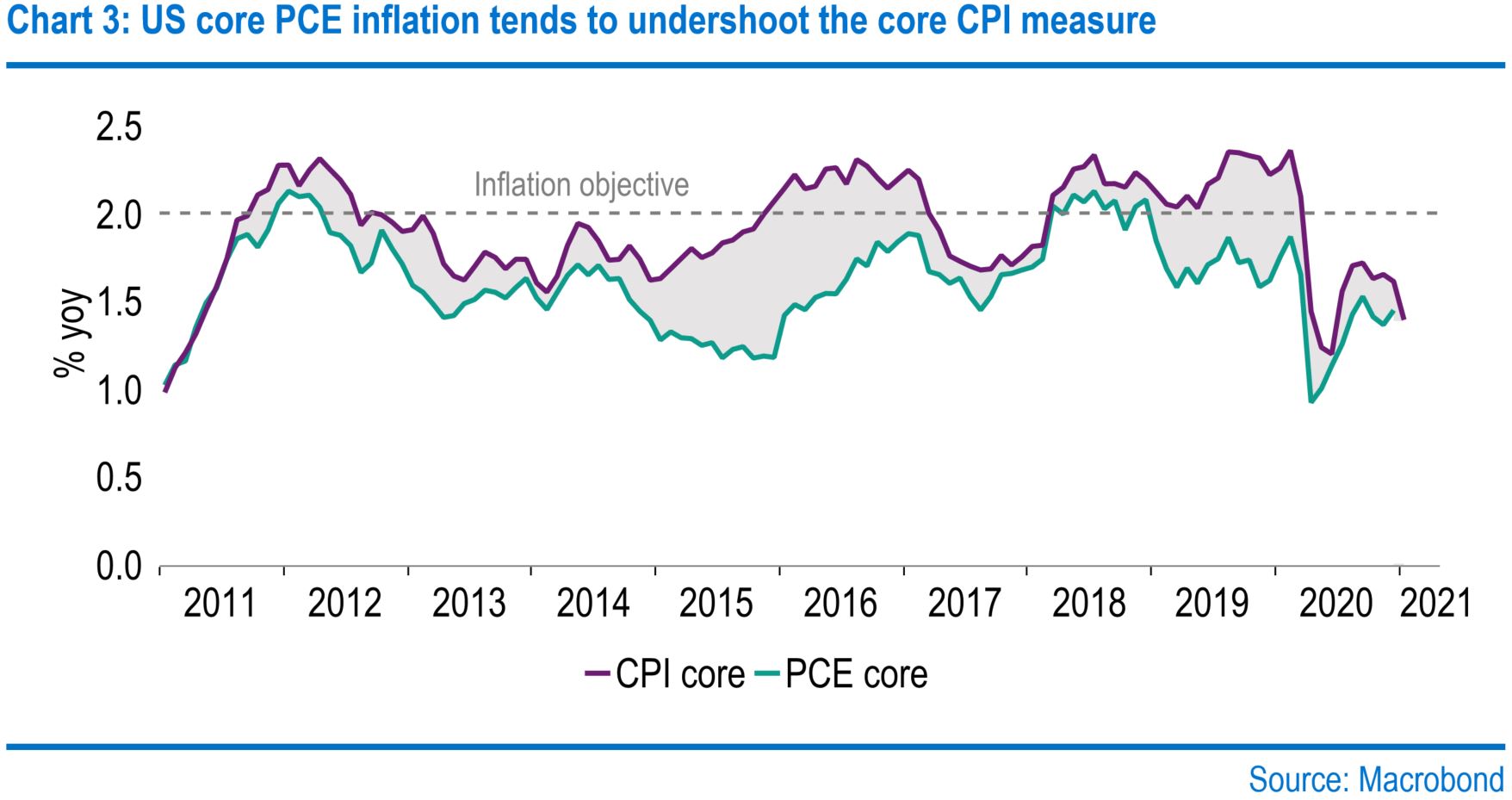

Treasury yields have risen again – those on 10-year bonds are a little short of 1.40%. While the trend has still largely been due to rising inflation expectations (breakeven yields), real yields have rebounded by 20 basis points to -78basis points over the past few days. The compensation of Treasury Inflation-Protected Securities, or TIPS, a type of bond indexed to inflation, is based on the CPI index, where the inflation rate is currently 1.4% (both headline and "core"). We would note that rental-related items make up a material proportion of the CPI – rent and “owners’ equivalent rent” account for 40.3% of the core index. Moreover, the Fed’s inflation mandate is based on the PCE price index, which has consistently run below the CPI measure over the past 10 years, and which has undershot the 2% inflation objective 89% of the time.

We suspect that economic strength will push rent prices higher, pulling CPI inflation higher relative to the PCE measure. With substantial labour market slack still available and the Fed’s mandate explicitly insisting on running inflation above 2% for a while to compensate for a period of low inflation, the Fed is nowhere near tightening, other than perhaps technical moves on its interest rate on excess reserves (IOER) and reverse repo rate. We still see the Fed reversing quantitative easing in 2023 and raising the Fed funds target in 2025. Our 10-year Treasury forecasts remain at 1.25% for the end of 2021 and 1.75% for the end of 2022, the pullback from current levels occurring perhaps on Fed warnings about financial conditions tightening too quickly.

Eurozone

This month has seen former European Central Bank President Mario Draghi elevated to Italian Prime Minister, heading a government of national unity. Following confidence votes in the Senate and Chamber of Deputies, Mr Draghi and his cabinet, which comprises a good mix of technocrats (Daniele Franco appointed as finance minister) and mainstream politicians, will turn to the priorities of the pandemic and finalising Italy’s Recovery and Resilience Plan by April, to unlock 200 billion euros of EU funds. Beyond this, Draghi will also need to address Italy’s long-term growth and structural issues while holding together a government that comprises all the main political parties, including the League following its surprise U-turn. Historically this has been no mean feat with Mario Monti’s unity government lasting only 18 months.

Markets have given the thumbs up to the new Italian administration: spreads of Italian 10-year government bonds to their German equivalent have fallen by 34 basis points since their peak on 22 January, following the withdrawal of Italia Viva from the previous government on 13 January. This is a five-year low. Yet Italian bond yields are only 15 basis points lower over the past month. This is as the spread compression occurred against a wider market backdrop of rising bond yields. As elsewhere, risk-on sentiment has prevailed in the Eurozone on hopes of an easing in social restrictions later this year, pushing German 10-year Bund yields up to -0.32%, the highest since mid-June.

Adding to the rise in bond yields in the Eurozone has been higher inflation: January’s HICP flash estimate reading was +0.9% year-on-year, up from -0.3% in December. The surge was boosted by the restoration of the usual VAT rates in Germany after last summer’s temporary cuts and the introduction of carbon pricing. But inflation also jumped in France, Italy, and Spain by 0.8 percentage points, 1 percentage point and 1 percentage point, respectively. Some of this – 0.14 percentage points at the Eurozone level – reflects an update in the weights of the price basket's constituents. The new weights reflect the substitution in the pandemic away from travel and hospitality services towards goods. As the weights are updated only annually, inflation was understated a little last year.

Looking ahead, coronavirus developments remain the central theme. A key consideration is vaccine rollout, where the EU19 has lagged behind other developed economies: in the Eurozone’s four largest countries, vaccinations stand at just 6 per 100 people, whereas in the UK, the figure is five times higher. This implies that social restrictions may remain for longer or even tighten – a new lockdown has been touted in Italy. Hence, while we still look for a recovery in the second quarter after a likely 1.2% contraction in the first quarter, we have redistributed the extent of the GDP rebound. Now we see a more significant pickup in activity in the third quarter. On an annual basis, our GDP forecasts now stand at 4.6% for 2021 and 5.2% for 2022.

For the ECB, this is set to lead to an exceptionally accommodative policy stance for an extended period of time. Indeed, we do not envisage the ECB altering its deposit rate until the fourth quarter of 2023. In the meantime, quantitative easing remains the marginal policy tool of choice. Given December's decision to raise the pandemic emergency purchase programme (PEPP) envelope by 500 billion euros to 1.85 trillion, and an end date of March 2022, any adjustment to policy, if needed, is likely to come via this lever. An area that the ECB has been watching closely is financial conditions. Should these see an unwarranted tightening, this could be addressed by frontloading purchases, making use of the flexibility of PEPP. The converse is obviously also true.

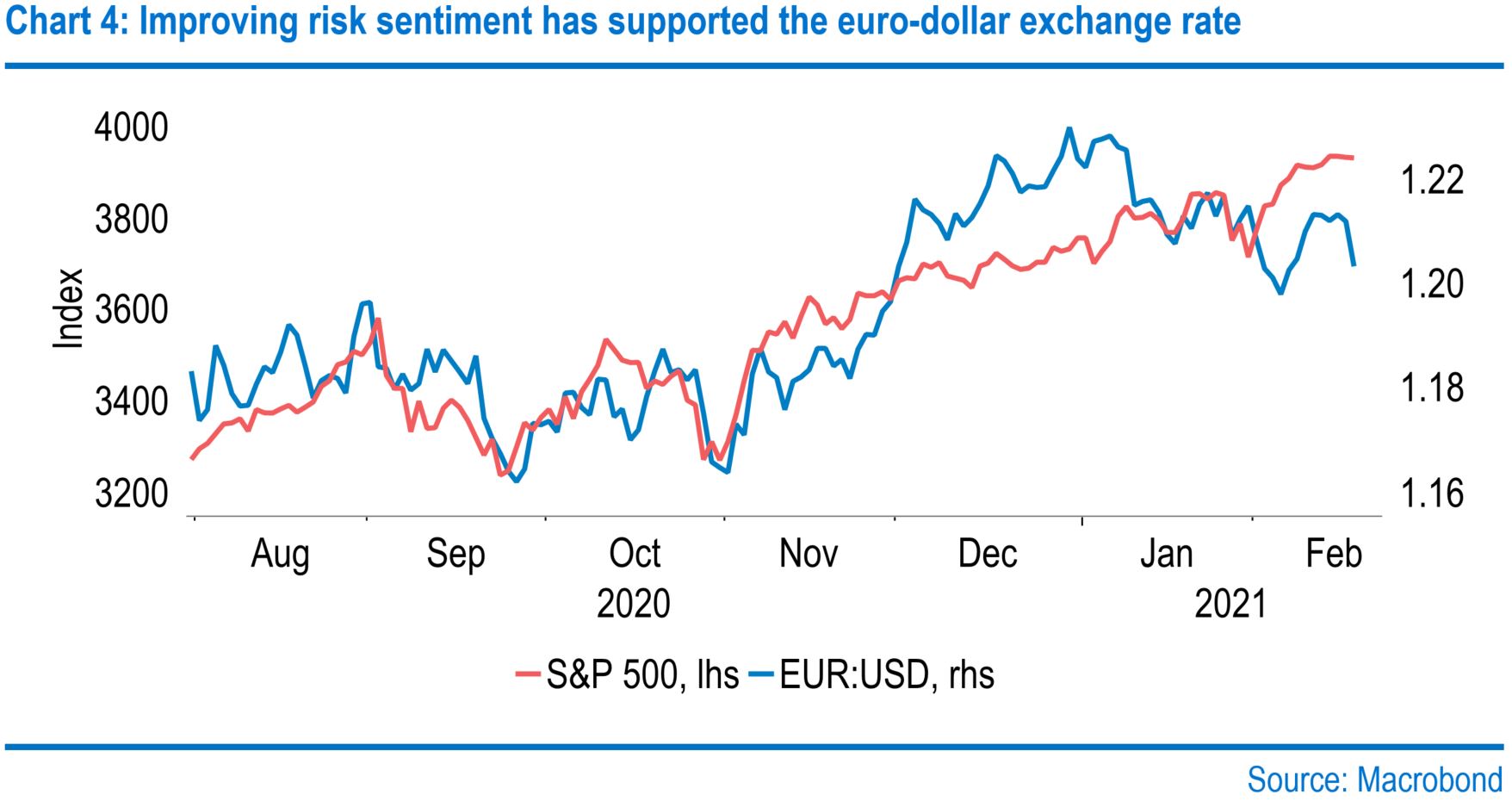

The euro’s strength has been one additional worry for the ECB. Over the last six months, general risk sentiment has clearly been a factor pushing the euro higher as the US dollar has weakened. However, over the last month, the upward momentum in the euro-dollar exchange rate has stalled around the $1.20 level. One might question whether the rise in US Treasury bond yields has supported the US dollar. However, this argument is certainly not conclusive, given that Germany's yields have also increased. In fact, the rise in 10-year US yields since the end of January has only outpaced that in Bunds by 4 basis points. We still expect the euro to rise this year, increasing to $1.25 by the fourth quarter and $1.30 by the fourth quarter of 2022.

United Kingdom

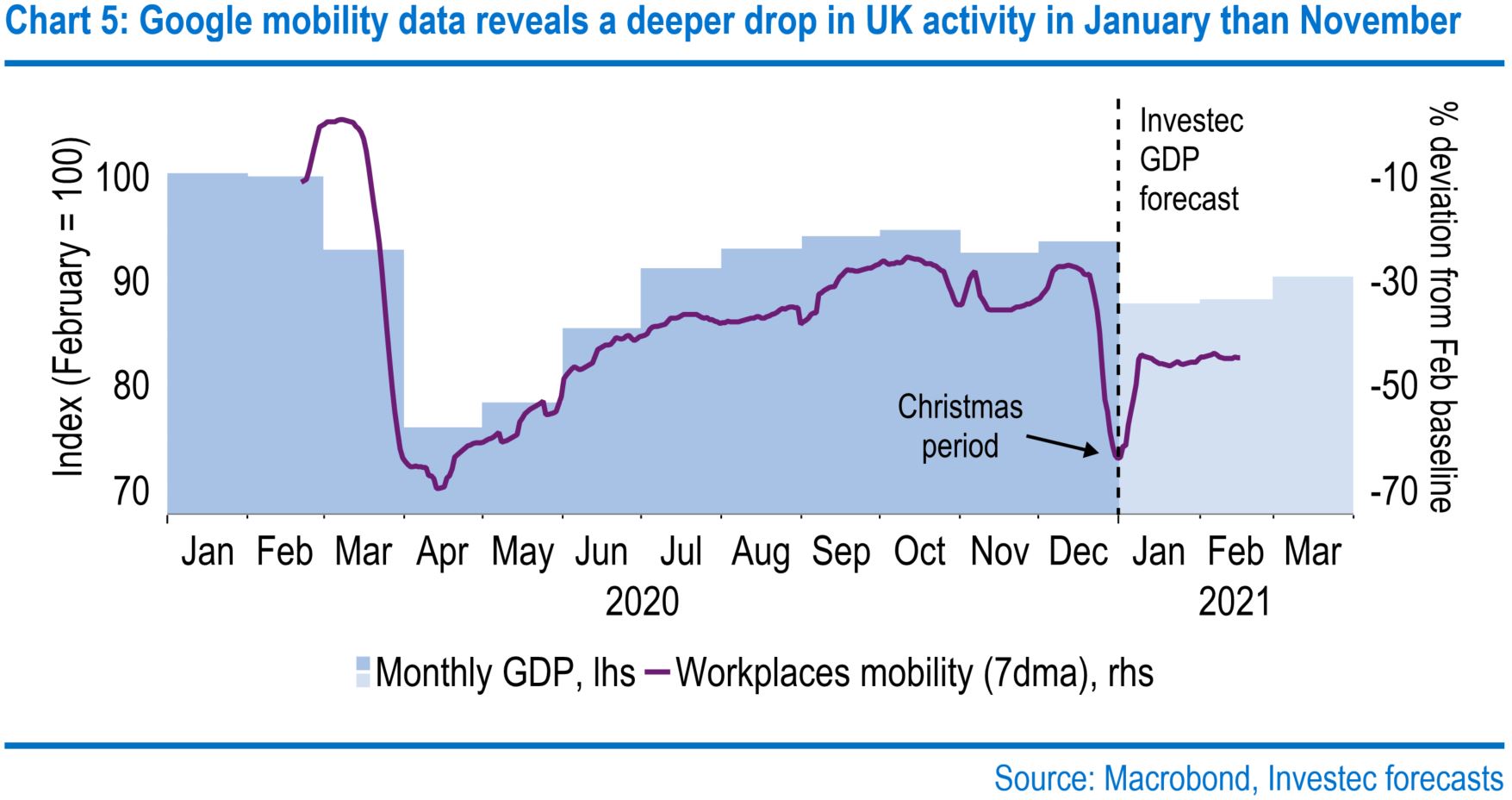

UK GDP rose by 1% in the fourth quarter from the previous three months, helped by a 1.2% rise in December. We have lowered our expectations for the first quarter due to the duration of the lockdown. We now see GDP falling 5.3%, compared with a drop of 2.5% seen previously. In contrast, we have pushed up our GDP forecast for the second quarter to expansion of 10.1%, compared with a rise of 6.9% seen previously. Our 2021 GDP forecast now sees growth of 6.4%, an increase of 0.2 percentage points from what we previously expected. We also now see growth of 6.5% in 2022 (previously 5.3%). The rapid vaccine rollout supports our general outlook. So does our estimate of "excess" household savings. This stood at £93 billion in December, up from £76 billion in November.

There are good reasons to expect a sizeable fall in output during the first quarter. Google’s mobility reports suggest that the drop in workplace mobility between pre-Christmas levels and the start of January’s lockdown was around twice that of November’s lockdown. A slightly stricter set of restrictions this time around also saw schools, colleges and universities forced to switch to online learning. Also, the emergence of more infectious variants of the virus drove case numbers up to record levels, prompting British workers and firms to take more caution with non-home working. However, we expect the economy to make up ground as restrictions begin to ease from March.

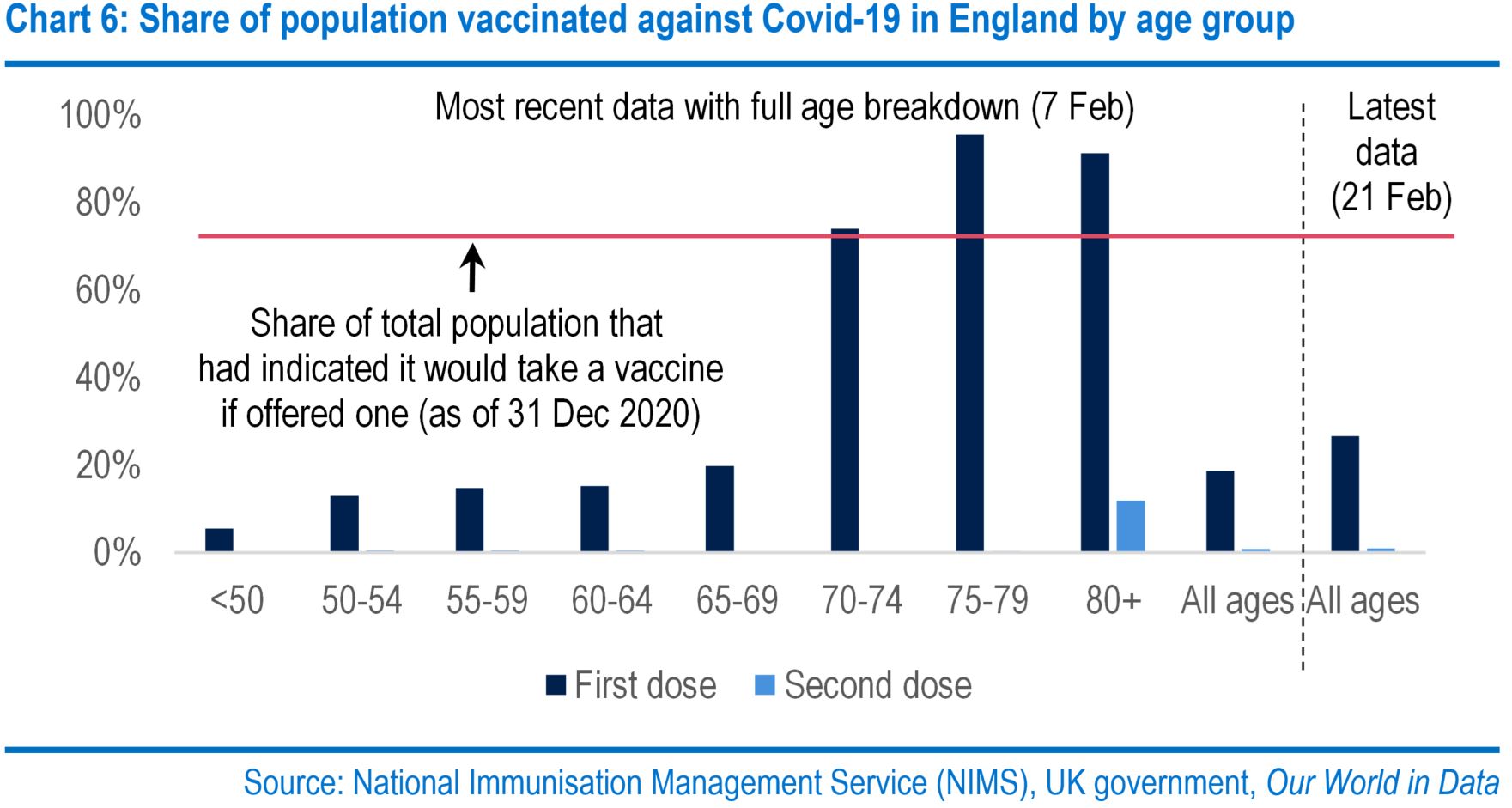

Prime Minister Boris Johnson’s roadmap for easing through the coming months, allowing the economy to recover, is underpinned by the vaccine rollout. This has been rapid to date - the government hit its initial target of offering a vaccine to all those in its top four priority groups by 15 February, which had comprised those aged 70 and over, care home residents, health and social care workers and clinically extremely vulnerable people. Encouragingly, the take-up of vaccines has been very high and exceeded what surveys had previously indicated. The burden of Covid-19 on the health care system should hence ease without requiring lockdowns for much longer.

The BOE has given banks six months to prepare their systems for negative rates. Mainly due to quantitative easing, bank balances at the BOE are high, currently £794 billion. Remuneration at a subzero Bank Rate would hit the banks - at -0.15%, the aggregate annual cost would be £1.2 billion. To dampen the impact, "tiering" is being considered, i.e. paying interest on bank reserves at graduated rates. The ECB uses reserve requirements as the basis of its tiering structure, but in the UK, these were suspended in March 2009. We still doubt that the policy rate will go negative. But preparing for the possibility requires some way of setting tiering thresholds, perhaps based on balance sheet size.

As the 31 March expiry for the Covid-19 business loan schemes comes into view, their use continues to increase. Chancellor Rishi Sunak has indicated that the government will announce a successor programme at the Spring Budget on 3 March. Its shape remains to be seen. Speculation is that a new programme could entail lower government guarantees on loans. What is clear is that the schemes to date have helped stem business failures and have, in turn, propped up the labour market. All eyes, therefore, will be on Mr Sunak on 3 March for "extra time".

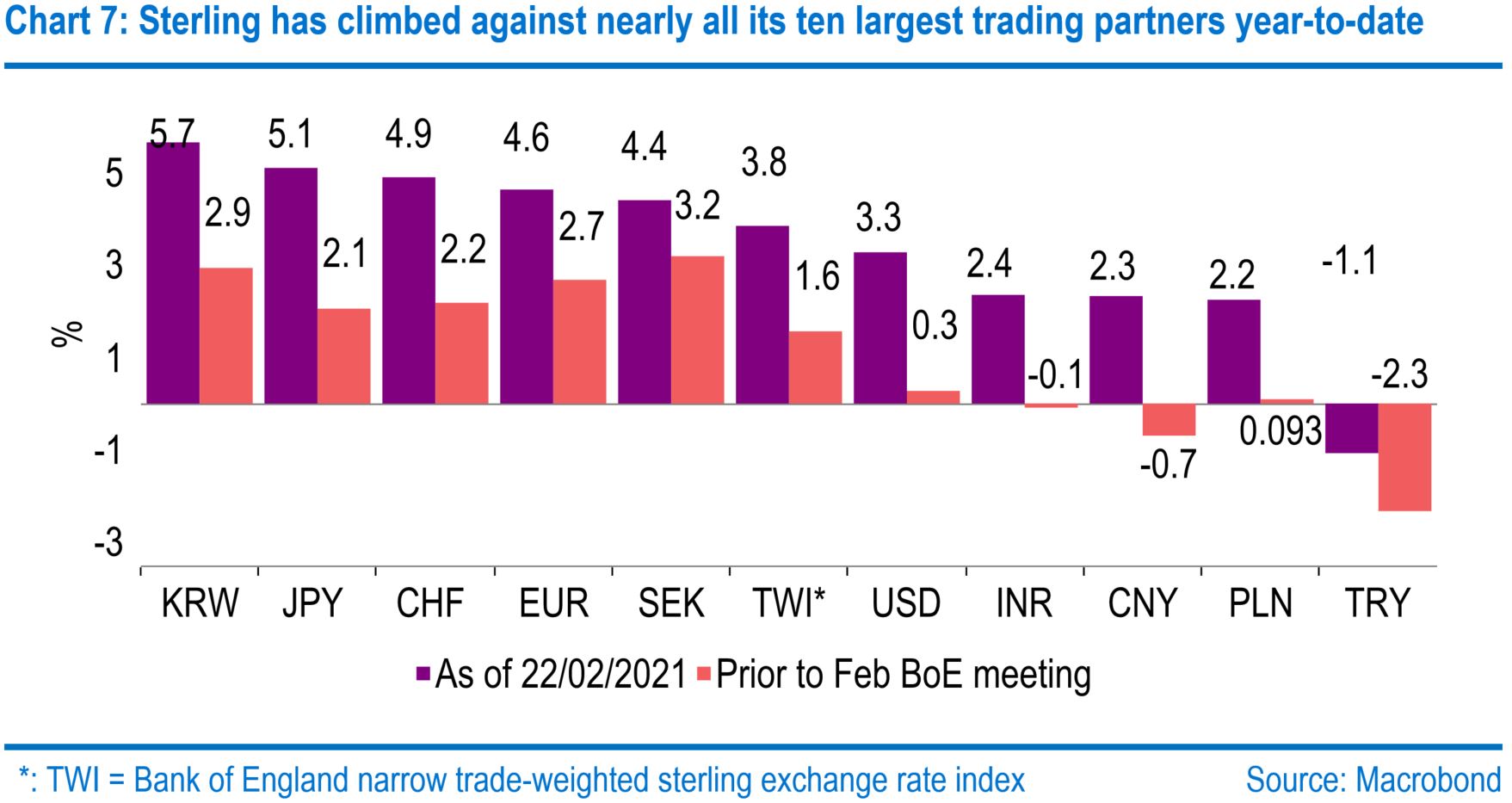

The pound has continued its steep climb that began around the start of the year, with further gains against both the US dollar and the euro. Indeed, sterling is a little above our 2021 year-end target of $1.40 against the dollar, and euro-pound already where we had pencilled it in for some time during the third quarter of 2022. That said, we have long identified sterling as fundamentally undervalued, so it is the speed of the move, not the direction, that is the surprise. The pound appears to be buoyed by the UK’s relatively swift vaccination rollout and by the BOE ruling out near-term negative rates at its last monetary policy decision. As others catch up, its momentum may slow, so we are not yet minded to make major changes to our pound forecasts.

Would you like to hear from our economists directly?

Sign up to receive invites to our monthly economic Q&A with a member of our team.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.