This survey was the first of its kind and comes at a pivotal time for the EIC membership, five years after the oil price crash. Together with the significant focus on climate change, ESG and energy transition, it is timely to seek more in-depth views from the EIC membership.

It was fielded to a variety of companies working in the energy industry, ranging from oil and gas, renewables, offshore wind and nuclear, among others. For the participating companies, the Middle-East was considered one of the main areas of focus as a target market along with recruitment and succession and the debate of the future of oil and gas, of which we will explore in further detail.

The state of oil and gas

From the sample segment, a primary theme emerged. The general sentiment was relatively bullish towards the outlook of oil and gas. 53% of respondents, who mostly operated in the oil and gas industry, considered the sector’s natural cycles to keep it steady over the long term.

However, in a slightly conflicting message, and one of which could alter the outlook of the oil and gas industry, was the increased interest in investment in renewables. With over a quarter of respondents looking to adapt their business model and/or strategy to different sources and applications for oil and gas, and it offers up an interesting debate.

Middle-East

Energy continues to be the prevalent trade within the Middle-East, and a region that many businesses operate in currently. The industry statistics speak for themselves:

Key stats:**

- 627 energy projects in the Middle-East worth $1 trillion proposed or under construction

- 409 projects worth $679 billion across the region implemented or delivered by 2019-2025

- 462 oil and gas projects worth $833 billion are proposed or under construction

- $369 billion upstream, $142 billion midstream and $369 billion downstream

**Data drawn from the EIC DataStream

These stats reveal the activity and potential in the Middle-East region. However many respondents identified the geopolitical risk, which engulfs many countries in the region, as an obvious threat to energy and business expansion.

Furthermore, factors such as gaining entry into the Middle-Eastern market, along with concerns over resource and talent in the region appeared to be on-going issues. Access, in general, into the region seems to be an area of concern.

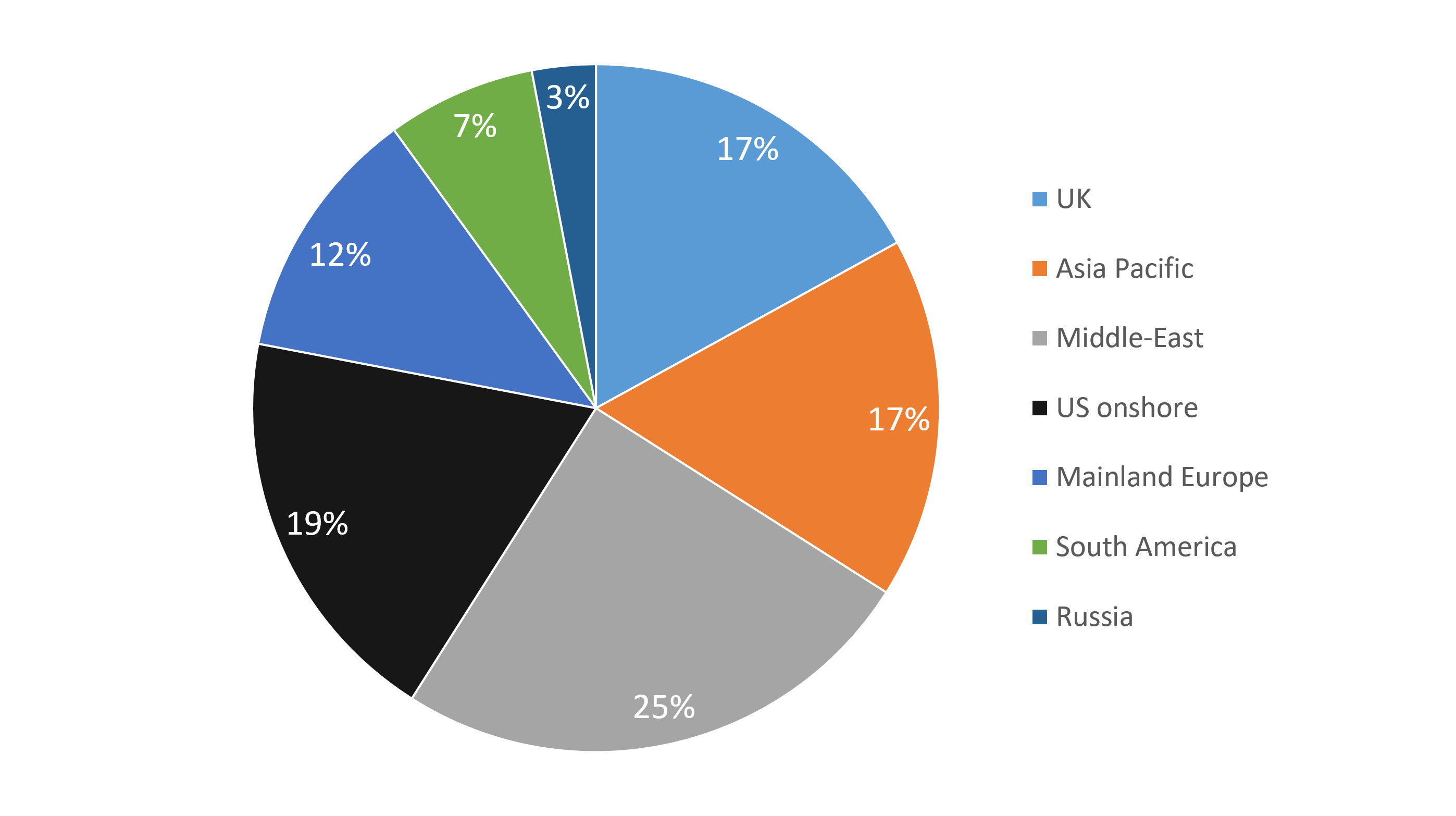

From the results, the UK remains a key market, but the surge in optimism towards US onshore and the Middle-East pulls these geographies into priority markets. Surprisingly, despite the abundance of natural resources in Africa, it appears to be less of a priority.

However, the general feeling is one of optimism for the Middle-East region. ADIPEC (Abu Dhabi International Exhibition & Conference), the largest oil & gas trade show, enjoyed an attendance of 145,000, demonstrating the growing appetite for growth in the region.

Priority countries for business expansion

Talent and succession

The results revealed ‘recruitment, especially young talent’ and ‘leadership succession planning’ ranked highly when asked what is ‘critical for your business.’ (ranked at an average of 4/5 for top priority, 5 being top priority). This is a particular issue within the oil and gas industry, as sentiment and tangible work switches towards a more renewable centric future. Accompanied with this, the attitude generated from the qualitative data again singled out “talent” as a key concern.

While this is an existing issue in all sectors and industries, the widening skills gap between the generations continues to press on the executives' minds, as reflected by the qualitative data. A lack of interest from emerging candidates in the energy sector, in general, contributes to overall concern in the next generation of talent.

It is important to note that 50% of the overall workforce is made up of contingent workers, by embracing “total talent” companies, especially in oil and gas, steps towards a solid workforce in the future will be made. Employers also need to understand the expectations and desires of the incoming workforce – a pivotal factor for building towards the future of energy, which will experience consistent change.

The finance behind it all

Of course, linked to all the main themes already outlined, is the financing required to facilitate expansion or recruitment. Our survey revealed a couple of further concerns, of which most of the concerns originated from Managing Director level from mid-size corporates. These included:

- Length of putting finance in place or the depth of detail appears to be a hindrance

- Can finance help growth for businesses and markets or develop new business

- Financial activities are controlled by family owners

- Access to internal finance for acquisition and organic growth

It could be inferred that businesses in the Energy sector are lacking the suitable finance to build business growth. Interestingly, this links closely to another question within the survey, which revealed 49% of respondents consider ‘developing new business/markets’ as their top priority for the next two years and 42% of the same pool wanting to ‘grow existing business/markets’ over the next two years.

Throughout our content series we will be exploring these topics in more detail, starting with the opportunities and challenges linked with expansion in the Middle-East, before moving on to the recruitment prospects of those operating in the energy sector.

*Investec Corporate and Investment Banking are the financial partner of the Energy Industry Council.

Get in touch with our energy experts

Find out more about the EIC

Browse articles in