Covid-19 and the future of UK Commercial Property - Investec for Intermediaries

29 October 2020

WFH and flexible working continue to upend commercial property expectations.

6 min read

View our infographic summarising the key points we’ve seen identified in the property market.

Desire for proximity to nature is creating a surge in buyers seeking to escape the city. But an increased desire for country living isn’t necessarily a ‘new’ trend - nor an end to the desirability of London prime.

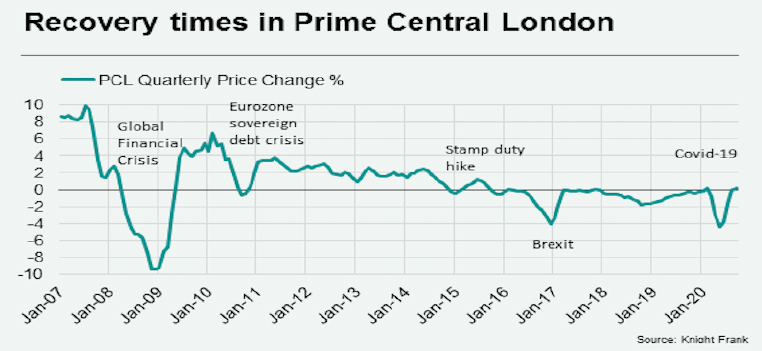

Demand for London’s prime homes has recovered since the first national lockdown, but more slowly than regions outside of the Capital. The Royal Institution of Chartered Surveyors found that, in September, house price growth was continuing to accelerate in all regions, but noted that “the rate of house price inflation appears to be more modest in London.”

It’s also important to consider the impact of a possible economic downturn expected in 2021. Already there are signs that the economic bounceback witnessed after lockdown is slowing.

Brexit has played a part in fuelling the state of the market today and it will also shape the trajectory of the coming months. Meanwhile, albeit further afield, the results of November’s US presidential election, although likely to be more of a short term effect, may impact buyers holding US dollars and looking for UK property.

Desire for proximity to nature is creating a surge in buyers seeking to escape the city. Laura Conduit, a specialist residential property solicitor at Farrer & Co., notes a surge in rural interest, saying: “We’ve seen an explosion in the country house market.”

But an increased desire for country living isn’t necessarily a ‘new’ trend – nor an end to the desirability of London prime. Back in 2018, Investec’s England’s Prime Property Hotspots pointed to the migration to the countryside as a growing trend amongst high net worth buyers, thanks to interest stoked by improved transport links, civic investments and emerging business clusters.

Paddy Dring, Knight Frank’s Global Head of Prime Sales, agrees. “People have realised they don’t need to be in the city all the time,” he says. “So what we’re seeing is an accelerated shift that was already happening anyway.”

Experts also recognise that the health of the rural market represents, in part, a booming second home market. “As you move to the top end of the market, clients are investing additionally in the country, and keeping both properties,” says Tom Bill, Head of UK Residential Research at Knight Frank.

Additionally, experts point out the need to avoid a short-term approach.

"I would urge caution. In the longer term the boom in the countryside market will have less of a marked impact than we might expect when looking at today's data."

- Tom Bill, Knight Frank

Demand for London’s prime homes has recovered since the first national lockdown, but more slowly than regions outside of the capital. The Royal Institution of Chartered Surveyors found that house price growth was continuing to accelerate in all regions in September, but noted that “the rate of house price inflation appears to be more modest in London.”

Experts attribute London’s slower recovery to the reduction in overseas purchasers. Jeremy McGivern, Founder of Mercury Homesearch, comments: “There are two very distinct markets, the domestic and the international. You can walk down King’s Road and it's very busy, but you cross into Belgravia and it's very quiet, because international buyers haven’t been able to come to London due to travel restrictions.”

However, Paddy Dring of Knight Frank highlights that restrictions haven’t deterred all international buyers. “If an overseas buyer knows that purchasing property in London is in their plan for the future, for example, because a child is due to attend school or university in the city, they’re more willing to buy remotely rather than waiting to view in person.”

Indeed, despite the drop in overseas buyers, some areas of prime London real estate have remained buoyant. Prime outer-London locations – especially the leafy London ‘villages’ –are seeing high demand from purchasers, investors, renters and home-sharers. SpareRoom says it has seen demand for gardens, patios and balconies almost double over the summer. Experts note this as a key consideration for buy-to-let landlords and those looking to extend their portfolio.

“Desire to find family homes with gardens and an area to work from in village-y neighbourhoods are off-the-charts,” says Andrew Weir, Chief Executive of London Central Portfolio.

The danger is that it is very easy to generalise. A lot of the movement has been due to pent up demand that has built up over four years due to Brexit and ongoing political uncertainty. But London has infrastructure that is hard to replicate. Businesses will continue to gravitate to the city, as will people seeking the best jobs, entertainment and social events. Would it be unreasonable to say that once a vaccine is discovered and London is open that it will continue to be one of the most vibrant cities in the world?

Recently, we helped a broker with the purchase of a second home in the country for a client. Speed was required and their income included salary, a cash bonus and vesting stock elements, with the bonus making up a large amount of the annual compensation. Through our understanding of such diverse income, the lending we provided meant the broker could secure the deal, at the required loan to value, within their client’s timeframe.

"Thanks to the pandemic we’ve got a more severe economic environment than anyone expected, on top of extremely significant political events. Investors need to be prepared for anything."

Phil Shaw, Chief Economist, Investec

It’s also important to consider the impact of a possible economic downturn expected in 2021. Already there are signs that the economic bounceback witnessed after lockdown is slowing. According to the ONS, monthly GDP grew by 6.6% in July as lockdown measures continued to ease, following growth of 8.7% in June. However, growth was slower than expected in August, with GDP increasing 2.1% from July, compared to its 4.6% forecast.

The Job Support Scheme will come to an end in the future so we can expect unemployment to rise. Alongside uncertainty over the impact of the second wave, it’s possible that the next six months will be more unpredictable than the last. There are however four significant calls to action which should not be overlooked. Firstly, the stamp duty holiday ending in March 2021; then there is the anticipated 2% additional surcharge for overseas buyers; the current discounted prices in the market compared to its peak in 2016; and, lastly, the added appeal of attractive sterling exchange rates.

Brexit has played a part in fuelling the state of the market today and it will also shape the trajectory of the coming months. Analysis from the London School of Economics shows that, if measured in terms of the impact on the present value of UK GDP, the effect of a no-deal Brexit could be two to three times greater than that of the COVID-19 pandemic.

Meanwhile, albeit further afield, the results of November’s US presidential election, although likely to be more of a short-term effect, may impact buyers holding US dollars and looking for UK property.

If your client has an existing mortgage with us or is ready to switch their mortgage to Investec, you can ask our dedicated team of private bankers for help and guidance. Either click on the button to arrange a call back or call us directly on 020 7597 4096.

So what conclusions can we draw as to where the market goes from here? While it is impossible to make any concrete predictions – we remain, after all, in a period of incredible upheaval and uncertainty – our experts point to some of the key considerations for buyers, sellers and investors to be aware of.

Thanks to pent-up demand and a range of ‘mini-booms’ in leafy London villages, London prime property remains buoyant. Furthermore, experts express confidence in the resilience of the capital’s prime market. “London property still retains its enviable status as a safe haven for tangible alternative investment,” says Andrew Weir of London Central Portfolio. “The attraction of GMT time zone, the global business language, rule of law, world-class education institutions and a liberal culture continues to appeal to a global audience of high net worth individuals.” General consensus though, is that we should expect to see a new balance of rural and urban living for some time to come.

A broker came to us with a client who wanted to secure their family home in London on a tight timeline. Their income appeared limited because they retained the majority in their business, but this is something we’re comfortable with and by looking closely at the client's business, we were able to find a solution on an interest-only basis, coinciding annual capital reductions with anticipated liquidity events, allowing them to complete against the necessary deadlines.

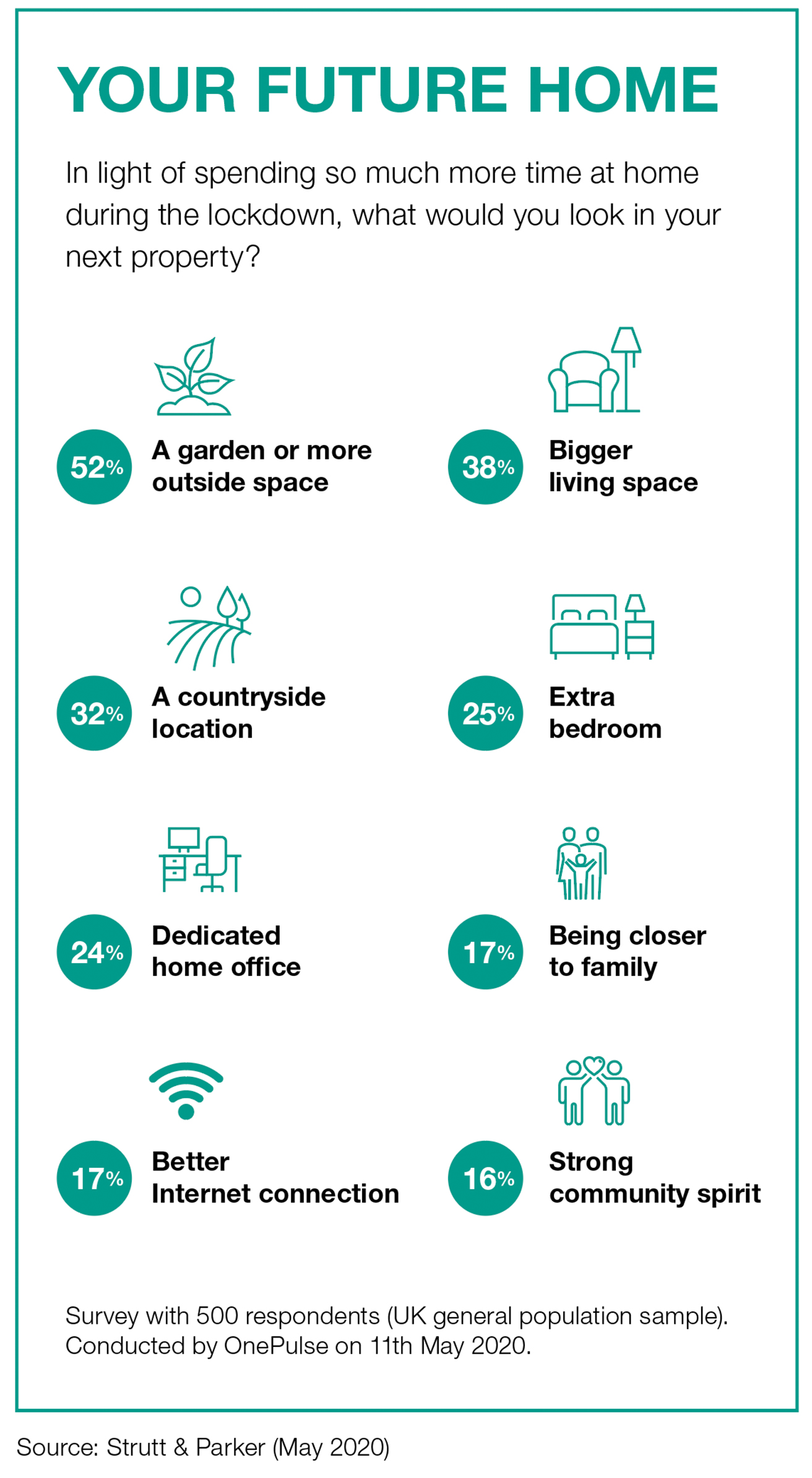

For long-term value, buyers and investors may want to consider what makes a future-proof property, in order to avoid taking a short-termist approach. This could mean ensuring a residence offers green space and a home office for flexible workers, while also retaining proximity to transport links to maintain easy access to the city.

Desirable characteristics of properties for prime buyers following the pandemic, according to Strutt & Parker’s Future Home survey with OnePulse. May 2020.

When it comes to wider political events, volatility may be unavoidable but experts are certain that opportunities will emerge. While lockdown may have created a competitive advantage for domestic buyers, due to travel restrictions stymying international interest, overseas purchasers may benefit from currency fluctuations.

“The event of a no-deal Brexit may weaken the pound, meaning there would be greater investment opportunity for international buyers,” says Hannah Aykroyd, Managing Director of Aykroyd & Co.

Despite the uncertainty posed by the political landscape, our experts note the continued perception of the UK property market as a relatively stable investment. As Knight Frank’s Paddy Dring, says: “Even taking into account the effects of COVID-19, and the risk of a second lockdown, the confidence in property as a safe asset class is still very much a reality.”

However, director at mortgage brokerage Coreco, Andrew Montlake notes: “Many lenders lack the capacity and willingness to lend right now. They’re ultra-cautious – but there’s a lot more business to be done.”

Join the conversation we’re having on Social Media.

Be the first to the invited to a range of our online webinars and networking events.

Browse articles in