Get Focus insights straight to your inbox

‘Mars ain’t the kind of place to raise your kids, in fact it’s cold as hell’. - Rocket Man, Elton John and Bernie Taupin

Is man-made climate change happening?

In the 1970s, there was concern that sun-blocking aerosols might lead to future global cooling. A 1974 Time article Another Ice Age? reported that ‘Climatological Cassandras are becoming increasingly apprehensive, for the weather aberrations they are studying may be the harbinger of another ice age’.1 For a northern-hemisphere public, this message was troubling – a previous great ice age had buried much of North America and Europe under three kilometres of ice.

Nearly 50 years later, the evidence points to the opposite threat – global warming – in part caused by man’s influence on the earth’s natural ‘greenhouse effect’,2 mostly associated with rising greenhouse gas (GHG) concentrations in the atmosphere since the Industrial Revolution. The earth’s surface temperature has increased by approximately 10C since 1850, although not in a smooth manner, and with over half the increase occurring since the mid-1970s. The trend is robust both for land and sea observations, and for northern and southern hemisphere measurements.

Behind the headline 10C figure, there are other important changes happening to the climate.3 Since the early 1990s, Greenland has lost an average of over 200Gts a year (billions of tonnes per annum) of ice, and Antarctica around 150Gts a year over the same period. The vast permafrost from Alaska to Russia is thawing. Glaciers are retreating everywhere. Melting ice and warming oceans are leading to rising sea-levels across much of the globe, threatening island states and coastal communities, including large cities.

Further, ecosystems within the biosphere are being disturbed. Coral reefs are being destroyed by bleaching related to rising temperatures while deforestation ravages areas such as the Amazon rainforest, one of our largest natural carbon sinks. Ongoing climate change may become the single biggest cause of biodiversity loss in the coming decades.

Without change, average surface temperature will probably continue to rise by 0.1-0.20C per decade, pushing us to over 20C warming this century.

It is notable that recent weather patterns4 show increased occurrence of extreme events – hurricanes, floods, high tides, droughts, heatwaves, and wildfires. Not all are directly related to GHG concentrations, but equally this evidence supports the theories that global warming will also lead to alterations in the frequency, intensity, spatial extent, duration, and timing of weather and climate extremes.

Overall, the Intergovernmental Panel on Climate Change (IPCC), a group of 1,300 scientists from over the world under the auspices of the United Nations, concluded there is a more than 95% probability that human activities over the past 50 years have contributed significantly to observed global warming. Without change, average surface temperature will probably continue to rise by 0.1-0.20C per decade5, pushing us to over 20C warming this century. That is the inconvenient science.6

The policy response – too much hot air

At the original Earth Summit, a United Nations Framework Convention on Climate Change (UNFCCC) held in Rio de Janeiro in 1992, more than 150 countries pledged to take actions to avert dangerous, man-induced climate change. Since then, two differing although complementary narratives can be distinguished in the policy debate in terms of the urgency of required action.

The mainstream view is focused on levels of the earth’s temperature. Most recently, it has been enshrined in the 2015 Paris Agreement ‘to do everything possible to keep global average temperature increases well below 20C and to pursue efforts to limit the increase to no more than 1.50C’. Moreover, this approach aims to ensure the global economy reaches a ‘net zero’7 position in terms of greenhouse gas emissions sometime in the second half of this century, which is designed to be consistent with the temperature objective.

Specific decarbonisation pathways consistent with meeting the 20C (or 1.50C) threshold span an enormous body of literature. An approximate aide-memoire is that to limit global warming to 20C, CO2 emissions must be limited to a cumulative budget since the Industrial Revolution of one trillion tonnes of carbon,8 of which nearly 60% has already been released, and net global CO2 emissions must reach zero before we hit the 20C threshold.

Nobel prize winner Joseph Stiglitz has likened the climate emergency to the Third World War, driven by the fear that ‘net zero’ may be too little too late.

An alternative perspective argues that unanticipated changes, not levels, in climate variables, including temperature, are what is most important for humanity. The climate is a complex system, with primary effects and secondary feedback loops. Time-series data from such systems (including temperature) are non-stationary.9 Complex systems do not change in predictable linear ways. Sometimes, a small change can result in large unanticipated effects, popularised in ‘butterfly effects’ and ‘tipping points’,10 the latter raising the spectre of irreversible climate change.

An important corollary of this alternative view is that forecasting future climate becomes more difficult.11 Given the uncertainties and dangers, this proposes a simple ethical rule, the precautionary principle,12 as a guide to how we should respond to climate change. Unsurprisingly, such an outlook is associated with calls for urgent action to stem rising CO2 concentrations in the atmosphere. Nobel Prize winner Joseph Stiglitz has likened the climate emergency to the Third World War, driven by the fear that ‘net zero’ may be too little, too late.13

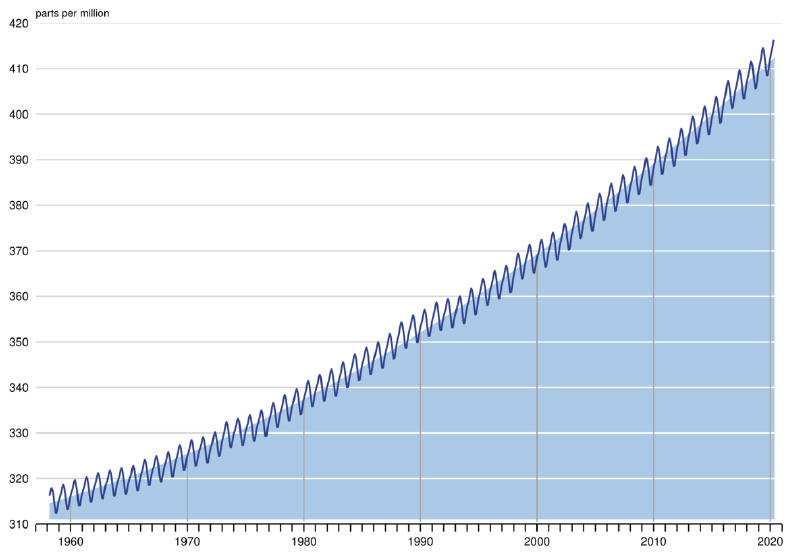

The main problem associated with either viewpoint is that the global policy response has been impotent in practice. Nearly 30 years on from the Earth Summit, and despite the subsequent milestone agreements at Kyoto (1997) and Paris (2015),14 greenhouse gas emissions continue to rise inexorably in the atmosphere, currently over 410ppm15 and rising on average at 2-3ppm a year.

We are on track to run out of our carbon budget during the second half of this century. That is not reassuring and suggests deep fault lines in policy formation. If we are relying on big government, we may be doomed to the frying pan.

Bottom-up momentum from voters, shareholders, and Gen Z

In light of the impotence of the international community to stem the growth in CO2 emissions through the UNFCCC process, at least to date, the epicentres for decarbonisation of the global economy are shifting.

Firstly, some regions and states within larger nations are taking unilateral action to tighten environmental legislation beyond national and international mandates. Scotland is just one example, aiming to be net zero five years ahead of the UK’s 2050 net-zero commitment.

Secondly, large cities everywhere are taking action beyond national mandates, reflecting local environmental concerns on both climate and pollution. The C4016 group of cities has committed to setting out policies by the end of this year, consistent with constraining global warming to no more than 1.50C.

Some regions and states within larger nations are taking unilateral action to tighten environmental legislation beyond national and international mandates.

Thirdly, corporates are setting their own net-zero goals pre-emptively, often under direct shareholder pressure, testimony to the importance of ESG17 as capitalism embraces sustainability. Examples abound, including Amazon, which has pledged to be net zero across its business by 2040, and BP, which recently committed to be net zero on its oil and gas production by 2050, if not sooner. ENI has pledged to plant or restore an area of forest approximately equal to the size of Wales by 2050.

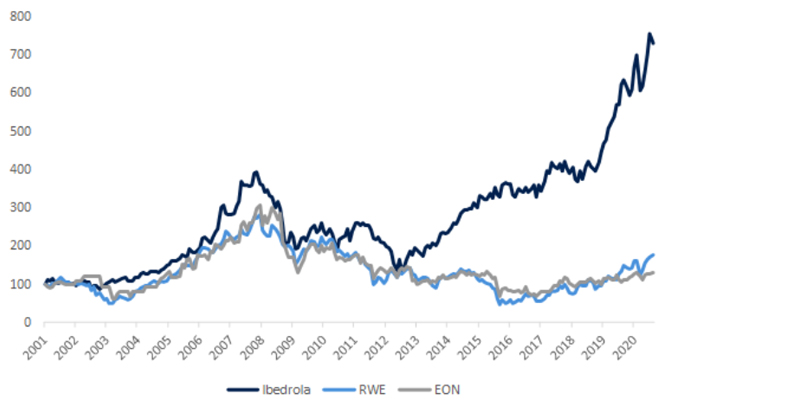

Often, the motivation is self-interest, not altruism. Oil majors have seen the German utility giants, E.ON and RWE, suffer many-billion euro write-downs, decimated share prices, lost renewables opportunities, and forced restructurings, on the back of slow adaptation to the German environmental agenda. Meanwhile, Spanish utility Iberdrola, owner of the UK’s ScottishPower, stole a global renewables lead.

Finally, lying beneath city states and corporate governance, individual action groups are championing climate issues, spurred on by Millennials and Gen Z. In a recent high-profile Dutch case, the government lost in the Supreme Court to an environmental group which argued the country had an obligation to go well beyond EU emissions limits, in order to protect its citizens.

All in all, shareholder pressure and the arm of the law may end up being Nature’s best friends, and potent catalysts for climate change action in the decades ahead.

Battlegrounds – transport and the race against time

Can industry restructure quickly enough to meet the demands of shareholders, voters, and the law? The key is the pace at which carbon-free electrification can substitute for fossil-fuel-driven CO2 emissions, in a world where energy consumption might grow 50% by 2050. Shell’s Sky scenario, an energy pathway compatible with the Paris 20C target, requires a five-fold increase in the electricity sector by 2070. That implies tripling the annual growth rate in electrification relative to the last fifty years.18

One of the key battlegrounds is in the transport sector19 where legislation across the globe is tightening. Technological innovation is accelerating. Spectacular declines in battery pack costs and the superior energy efficiency of BEVs20 versus traditional ICEVs mean incumbents including BMW and Volkswagen are warranting competitive market offerings in the early 2020s, to challenge Tesla.

Alignment of government policies with manufacturers remains a hurdle for EV growth acceleration.21 Even on optimistic scenarios, all modes of EVs22 will have only 30% of the global market by 2030, thirty times above today’s levels. That implies rapid change, but it is not certain it will be fast enough.23

Overall, decarbonisation of transport is a race against the clock, with technological innovation driving progress, but no guarantees that a transition from fossil fuels can happen fast enough. In the end, the consumer will have a critical role to play in dictating the pace of change. That involves all of us, our attitudes towards everything from using public transport to the amount we fly,25 to the food we eat26 (which has a carbon footprint that is heavily dependent on how it is transported). The message is that carbon abatement is ultimately about carbon consumption. Changes in our individual consumer lifestyles are inevitable, every bit as much as supply-side change, if potentially dangerous increases in global temperature are to be avoided. The transport sector is just one example.

Portfolio investment and stock selection

The eyes of hardened investors may glaze over on the proposition that the biosphere and biodiversity are at the heart of corporate profitability. Yet this is a dangerous slumber. We have seen the demise of the traditional German utility industry. Oil & gas companies are now impairing billions of dollars of fossil-fuel assets. Conversely, valuations of new-generation energy companies show the opposite trend.27

At heart, this is an issue about discount rates and the cost of capital. Critical issues include the market’s required return on equity, and how it feeds through to individual sectors and stocks in terms of their equity and debt costs.

The market’s required return on equity will ultimately be determined by our response to climate change – an example of the inescapable mutuality between corporates, consumers and voters that we have seen play out clearly in recent months after the coronavirus outbreak. The extent of ‘non-diversifiable’ risk28 in the equity market in future is likely to depend critically on this alliance. In the absence of strong, agreed social action, traditional statistical inference based on the assumption of well-understood stationary distributions of equity returns will become less reliable.

Rapid permafrost melting, migrations on the back of crop-failures and famine, plus disease escalation as a result of the lack of water availability, all represent serious threats to the required social cohesion. One eventuality that cannot be ruled out is escalating uncertainty, an increased number of ‘tail events’,29 the flight to safety of private insurance, debt and equity finance, and eventually, the re-emergence of the state as provider of capital of last resort.30

The market’s required return on equity will ultimately be determined by our response to climate change – an example of the inescapable mutuality between corporates, consumers and voters that we have seen play out clearly in recent months after the coronavirus outbreak.

The path towards any such eventuality would certainly complicate risk management overall, based on increasingly meaningless measures of the market risk premium. In turn, that would make a nonsense of corporate risk/return estimates founded on underlying beta estimates. Specifically, it would undermine passive equity funds, whose justification depends on risk being properly summarised as a function of the equity market premium and beta.31 It is unsurprising that such funds are becoming champions of a strong global climate response. Without it, they may become a market irrelevance, a new ‘irrelevance theorem’ for finance theory to complement Modigliani and Miller.

More generally, most sectors of the economy in both agriculture and industry are weather-and-climate dependent, as are their supply chains. Insurance markets and short-term bank debt offer hedging against such risks, but that is dependent on reliable risk measures to allow fair premiums and loan pricing. Change the climate radically, and all bets are off. Liquidity in financial markets and the risk estimates that underpin financial services ultimately depend on environmental stability.

What does all this add up to for the golden rule of finance – diversification? In sustainability-focussed portfolios, a logic for diversification32 remains, but with the proviso that old correlations will be increasingly irrelevant in future, failing to capture ‘smart beta’. Future risk management through diversification will involve diverging from traditional market portfolio benchmarks and imposing greater shareholder influence on corporate strategy as risk management tools.33 This should reduce stock ‘crash risk’. The point has not been lost on the global hedge fund industry.

Various other cost of capital issues are already playing out in financial markets at sector and stock level, in both the equity and debt markets. Debt pricing is moving to reflect the carbon ambition of companies in terms of incentive-linked ‘green’ bonds. Interest costs are being tied to environmental goals, acting as an incentive for strategic change in sectors challenged by decarbonisation, including heavy industry, airlines and mining. Bondholders are increasingly using refinancing as leverage to push through such ESG goals.

The flip side is that a growing set of institutional investors is refusing to invest at all in companies considered to be at serious risk because of their climate policies. In future, delinquent companies may see themselves black-balled out of public equity markets, raising the cost at which they can access equity by pushing them into specialist hands. Admittedly, there are still some investors such as Warren Buffett who prefer companies not to be moral arbiters, but the tide is turning.

I may, perhaps, be allowed to finish with one personal reflection on investment in the new world which we confront. It is human nature that investors want to find the next winner. Perhaps the clue lies in the word nature. The greatest scope for future investment returns may well lie in unlikely stocks and emergent sectors, including natural capital.

This theme, in itself, could run to several volumes. For our purposes, consider simply this. Ecosystems are assets. They are very special assets - they grow if left alone. Forestry and fisheries as just two examples. Investment can simply involve waiting.

Today, own rates of return on key ecosystems in the earth’s biosphere are far in excess of the recurrent market yields on equity, using the proxy of a market dividend yield (3-4%), or long-term government bonds (close to 0%!). In fact, on some estimates they are almost 20%. Despite this, we continue to destroy ecosystems in our thirst for greater physical capital. That is unsustainable and bad economics.

The conclusion? A huge pool of undervalued assets lies in nature. I know where I’m putting my money!

Assessment

To summarise, climate change is for real. It is redefining the meaning of capital and reshaping economies and corporates in the process. It is rewriting politics, with no respect for national boundaries or policies. Our global policy response to it has, to date, been weak. We have to hope that a combination of human adaptability, technological innovation, and the law, can make up for that.

For markets, climate change forces us to rethink profitability, valuation, correlations and diversification strategies. It promises a rather bumpy ride. With respect to Elon Musk, colonising Mars may not be that pleasant, as Elton John reminded us many years ago. Our pale blue dot34 might just be all we’ve got. To ensure its and our own future, well-informed investment and wealth management will become more important than ever.

Relative Performance of Iberdrola, EON, and RWE shares since 2001

Source: Bloomberg, Investec Wealth & Investment

Monthly Carbon Dioxide Concentration

Source: National Oceanic and Atmospheric Administration (NOAA)

https://scrippsco2.ucsd.edu/graphics_gallery/mauna_loa_record/mauna_loa_record_color.html

1 We live in an inter-glacial period referred to as the Holocene, which started some 10,000 years ago, involving an increase of average global temperatures from the last ice age of 5-60C, and a 120m rise in sea-levels.

2 The natural ‘greenhouse effect’ refers to the higher average temperature on earth caused by a set of atmospheric ‘green-house gases’ (GHGs), including water vapour, CO2 (carbon dioxide) and CH4 (methane).

3 To reflect the broader context of the impact of greenhouse gases, the general term used today is the threat of ‘climate change’ rather than a unique focus on ‘global warming’.

4 We may think of ‘climate’ as the long-term average, variance and other statistical moments of daily ‘weather’ patterns, as measured by variables including temperature, rainfall and wind-speed.

5 Based on an assumed log-linear relationship of atmospheric CO2 concentrations and temperature increase, with a doubling of concentrations from the pre-Industrial Revolution era implying 20C approx. warming later this century. For calculations, assume 50% approx. of emissions linger in the atmosphere long-term.

6 Disagreements remain of course, in part because climate is a complex system defying easy predictions (later).

7 Net zero emissions implies any residual emissions must be offset by carbon-removal, whether through technology (such as carbon capture and storage) or nature (through reforestation, for example).

8 Care is needed with measurements. Carbon mass is sometimes quoted in terms of carbon, and at other times in terms of CO2. The conversion rate is 1 tonne carbon = 3.67 tonnes CO2.

9 A non-stationary statistical distribution is one where averages and variances evolve over time, rather than being fixed. A time series dataset that is stationary is thus ‘ahistorical’, unlike a non-stationary one.

10 The butterfly effect is the idea that a butterfly’s wings flapping at one place in the globe could cumulate into a violent storm somewhere else. Tipping points refer to collapses in key parts of the climate system.

11 A useful rule of thumb in a complex non-stationary system is that the longer the attempted forecast period, the greater the potential error.

12 The principle prioritizes strategies based on extreme caution in situations of great uncertainty but potentially catastrophic effects.

13 Moreover, ‘net zero’ potentially raises a moral hazard. Carbon capture technologies may encourage the world to act in a way that does not properly reflect the underlying risks of climate change.

14 The US failed to ratify Kyoto. It has announced its withdrawal from the Paris Agreement also.

15 Ppm stands for parts per million, another metric commonly used to measure atmospheric CO2 levels. The conversion is as follows: 1 ppm of atmospheric CO2 is equivalent to 2.13Gts carbon, or 7.82Gts CO2.

16 C40 is a network of the world’s megacities committed to addressing climate change. The C40 represents over 700m citizens and nearly 25% of the global economy.

17 ESG stands for Environmental, Social, and Governance issues.

18 Even then, Sky still relies heavily on methane and hydrogen to meet its ambition. It would require 10,000 large CCS plants to be built globally, compared to around 50 in service today, and hydrogen to grow as a major energy carrier post 2040, reaching 800m tonnes p.a. capacity by 2070 (around 10x today).

19 Transport and heat (industrial, commercial, and domestic) are the largest areas of the economy needing to be decarbonised. Heat raises some of the most difficult issues of all. A promising route may be to use greater energy efficiency and a hydrogen pathway, using parts of existing gas infrastructure.

20 BEV stands for Battery Electric Vehicle. ICEV is Internal Combustion Engine Vehicle. An alternative route to a green vehicle is to use hydrogen in a fuel cell (FCEV or Fuel Cell Electric Vehicle), an option that has attractive qualities, but where a core issue is the pace at which a hydrogen infrastructure can be rolled out.

21 One example relates to making charging infrastructure widely available, with governments preferring inter-operability between charging networks, whereas some innovators prefer specialised solutions.

22 Defined not just as BEVs but as plug-in hybrid models also (PHEVs).

23 Heavy-duty vehicles, trains, ships and aeroplanes raise more difficult decarbonisation challenges, although a ‘green’ hydrogen route holds the realistic prospect of making an important longer-term contribution.

24 Especially in high-impact urban areas. Here there is an urgent need both for ‘grey’ adaptation in terms of transport infrastructure (cycle lanes, electric bus and train fleets), and ‘green’ adaptation (parklands etc.).

25 One transatlantic flight per year causes about 3 tonnes of CO2 equivalent emissions per person.

26 For example, air transportation across food chains. An apple transported by ship has a different carbon footprint to one transported by air. In fact, as decarbonisation of industry happens, the greatest risks to climate change will be food and agriculture, another case where fundamental consumer change is a necessity

27 Examples abound, but include giants like Iberdrola and Tesla in the large-cap world, and ITM Power and Ceres Power in the mid-cap world.

28 Non-diversifiable risk is traditionally associated with factors to which all stocks are exposed. This provides the rationale for the equity market offering an expected return in excess of bonds.

29 This common term needs handled with care. It refers to low probability events within defined statistical distributions. However, the issue is that, with climate change, those very distributions may become ill-defined.

30 i.e. re-nationalisation. It is important to understand that this does not imply the disappearance of equity risk. It simply means it is passed (some would say hospital-passed) back to voters and the state.

31 In CAPM, beta is a measure of the covariance of a share with the market. If the variance of the underlying market is unstable, that in turn implies that company risk measured by beta will also be unreliable.

32 Investors may interpret this in an axiomatic framework such as the Capital Asset Pricing Model (CAPM). However, the simple maxim ‘do not put all your eggs in one basket’ will suffice just as well, in our context.

33 Traditional ratios and measures of profitability are currently under the microscope of ESG, with a range of alternative measures starting to emerge, designed to capture items including environmental risk.

34 The phrase refers to a picture of planet Earth taken from Voyager 1.

Responsible Investing and Sustainability at Investec Wealth & Investment

As Sustainability is core to our fundamental investment approach, we have integrated ESG considerations into our investment decision making and broader investment process.

Investec products you may be interested in

Wealth management

Offshore investments

Investments

Wealth management

Offshore investments

Investments

Browse further in