Get Focus insights straight to your inbox

The compounding growth of the West is powered by business enterprises and savers share in the wealth created

Most of us will be familiar with the tale of ‘The Ugly Duckling’ by Hans Christian Andersen. It tells the story of a duckling who is initially scorned and bullied by all because of his odd appearance. After suffering so much rejection, the duckling grows into a beautiful adult cygnet. It’s a fable that teaches us about determination, staying true to oneself and looking beyond mere appearance.

It’s a story that springs to mind when reflecting on the performance of SA equities over the last few years. A couple of years ago, investors both domestically and abroad had seemingly written South Africa off as an investment destination. Everyone appeared to prefer the ‘racing greyhounds’ of the Nasdaq.

But then SA’s annual GDP growth for 2021 came out at 4.9%, some 2.8 percentage points higher than the consensus forecast of 2.1%, and the biggest consensus beat in the world at the time. This was down to the boom in commodity prices.

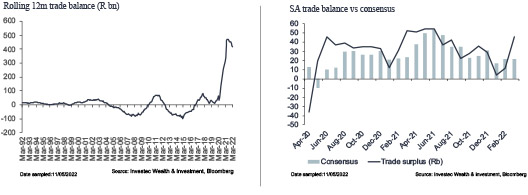

Surprise in 2021 GDP growth relative to expectation in June 2020

Date sampled: 11/05/2022

Source: Investec Wealth & Investment, Bloomberg

The chart below shows how our rolling 12-month trade balance peaked at almost R500 billion recently and the trade surplus has consistently been coming in higher than consensus expectations.

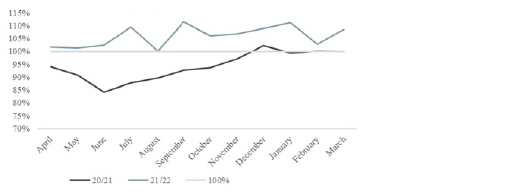

The commodity price boom has had a significant impact on the broader economy. Not only are personal tax receipts higher than they were in 2020, but they’re also higher than they were pre-Covid by 6%.

Monthly employee tax relative to 2019

Date sampled: 11/05/2022

Source: Investec Wealth & Investment, National Treasury

And commodity prices have been hugely beneficial to the fiscus, which helped the rand to strengthen. In just the first six months of 2021, mining companies’ payments to the fiscus were more than double those of any prior full-year period.

Demand and supply to keep commodity prices high

We think we’re going to see these high commodity prices sustained for two reasons: supply and demand. The supply of commodities will fall short of demand, thanks to years of underinvestment in capital spending (capex) while demand will rise because of the energy transition.

This is a very long-term story that we think will play out over at least a decade.

It’s well-known that we need to reduce carbon emissions to limit global warming. Specifically, to have a 50% chance of avoiding warming beyond 1.5OC, the world needs to halve its current emissions by 2030 and reduce them to net-zero by 2050.

Not only are there these pressing climate concerns, but with European energy security threatened by the Russia/Ukraine war, the need for the energy transition is even more urgent.

But a lower carbon world is going to be commodity-intensive. The chart below shows just how much ‘green’ metal is needed for various low-carbon technologies:

Minerals used in selected clean energy technologies

SA to benefit from increased green metal demand

In South Africa, we’re blessed with an abundance of many of these so-called green metals: platinum group metals (PGMs), chrome, manganese and high purity iron ore, to name a few, and the chart above shows just how necessary these are to the energy transition.

You can see that a substantial amount of manganese is used in the production of/powering of an electric car, especially when compared to the conventional combustion engine car – it’s essentially double the copper and double the manganese.

Optimism about SA stocks and the broader economy

We’ve been through a period of almost no growth – companies have struggled to grow revenue and inflation has caused input costs to rise, squeezing the bottom line and resulting in earnings declines. These companies have de-rated substantially.

But now there’s a potential situation where there’s a bit of top-line growth coming through as those personal tax receipts continue to rise, and this should help those companies re-rate going forward.

For these reasons, we are optimistic both about SA stocks – particularly those that are trading at depressed levels and stand to benefit from the demand deriving from the energy transition – and the broader economy. We see commodity prices remaining high thanks to the mismatch between greater demand from the energy transition and lower supply as a result of years of underinvestment.

While in the short term this outlook may seem less obvious given the increasing likelihood that the US Federal Reserve may trigger a global recession by raising rates sharply, the longer-term outlook for base metals, particularly those required for the renewable energy transition looks promising. This view is shared by research house BCA, which ranks the outlook for base and bulk metals over the next 10 years as a “strong overweight / very bullish”. All things being equal, this should bode well for SA equities as well.

In Hans Christian Andersen’s famous story, the ugly duckling goes through many episodes of hardship and rejection before discovering that he has matured into a beautiful adult, and is accepted by all. Applied to SA equities, we think the ugly duckling can win the beauty parade, it may just require a long-term view.

Get Focus insights straight to your inbox

Investec products you may be interested in

Wealth Management

We work with some of South Africa’s most successful individuals and families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

Wealth Management

We work with some of South Africa’s most successful individuals and families to preserve and grow their wealth. Let us do the same for you.

Portfolio Management

Whether you’re wanting to grow your wealth or generate income, tap into our expertise to help realise your investment goals.

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

Browse further in