Emerging markets add to global growth woes amid recovery signs

Just as many developed countries are re-opening their coronavirus-battered economies, some emerging-market nations face growing first-wave outbreaks. That has prompted the Investec economics team to cut their world growth forecasts in this month's Global Economic Overview, with the threat of "second waves" making the outlook even more uncertain.

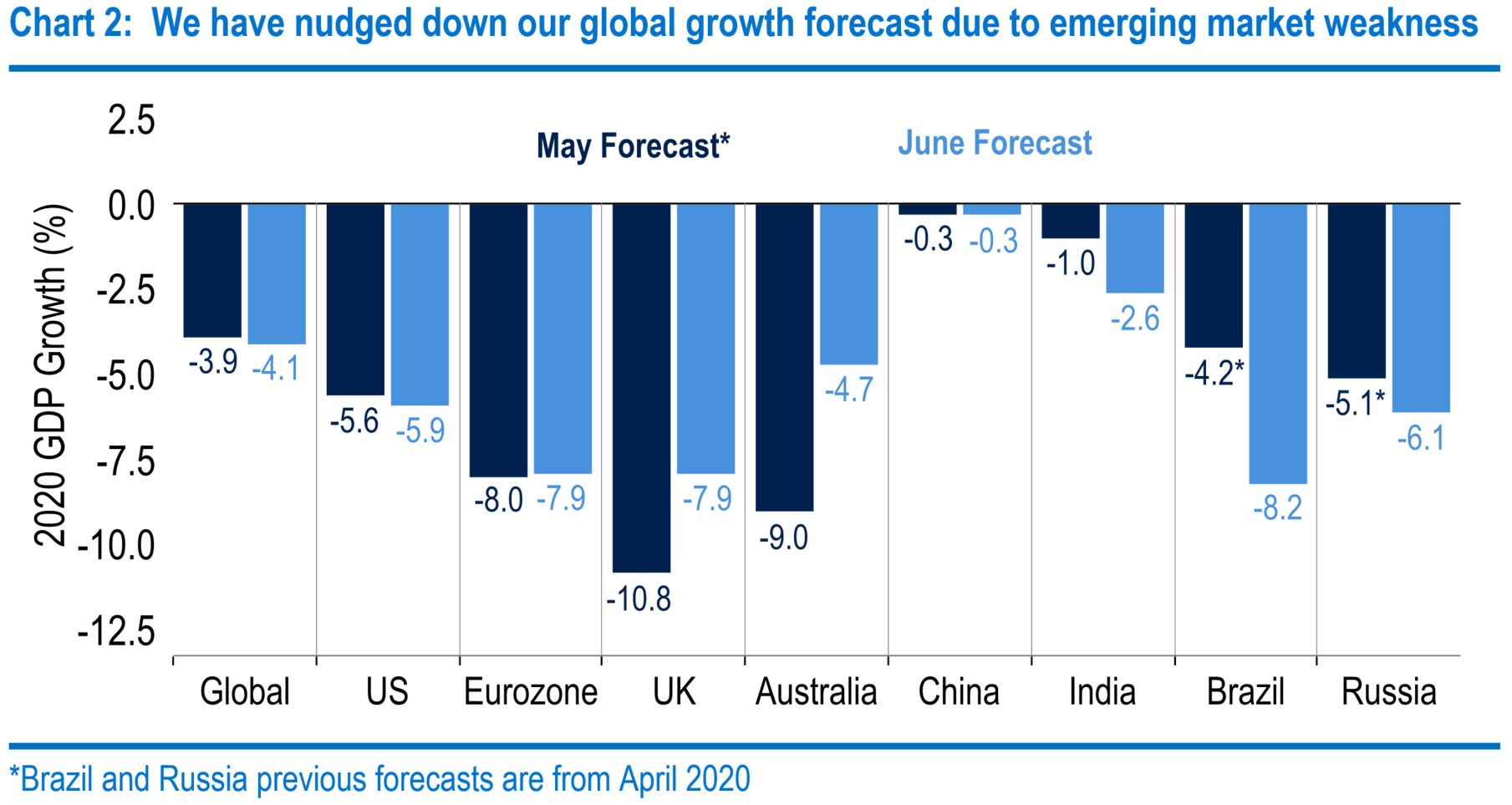

Differing approaches across countries to tackling the coronavirus pandemic have led to varying growth prospects globally. The US recovery looks well underway, albeit with a long way to go and with infections rising again. The Chinese economy is rebounding but looks subpar. Meanwhile, some emerging-market countries such as Brazil are of significant concern on both economic and health grounds. Most European economies, including the UK, are lagging behind the US, but anecdotal evidence points to a more robust economic performance recently. One feature here is that the second-quarter downturns look less severe than feared and although we suspect the second-half rebounds will be less punchy, this helps the 2020 gross domestic product (GDP) growth forecast. However, it also pushes 2021 estimates down. Driven by emerging-market downgrades, we have lowered our 2020 global GDP forecast to -4.1% from -3.9%, and that for 2021 to +5.3% from +6.8%.

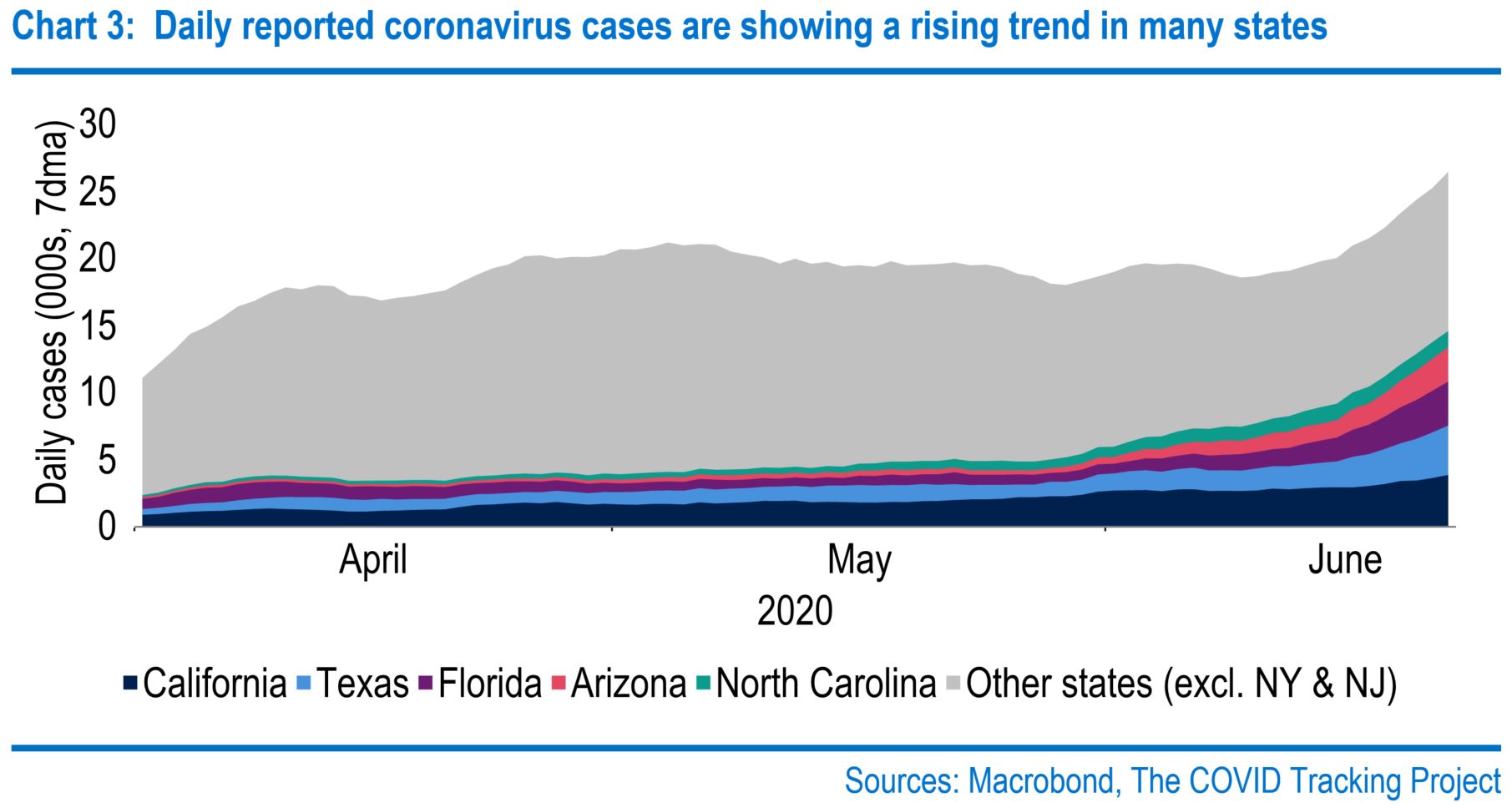

At the national level, reported daily coronavirus cases are rising rapidly. The picture across most southern and western states is very different from most northern states. Indeed, the significant case rises are typically in the former group, often where lockdowns were eased relatively early. What matters for the economy is whether material new lockdowns are put in place. Amid a taste of the economic rewards of re-opening, we think politicians will desperately try to avoid this. President Donald Trump is very keen to avoid this too, with recent polling suggesting his prospects for re-election are not good. Even if new lockdowns are not put in place, further recovery gains may be restricted if more re-opening is delayed. For now, we have made relatively modest adjustments to our GDP forecast and now look for -5.9% this year and +4.2% next year.

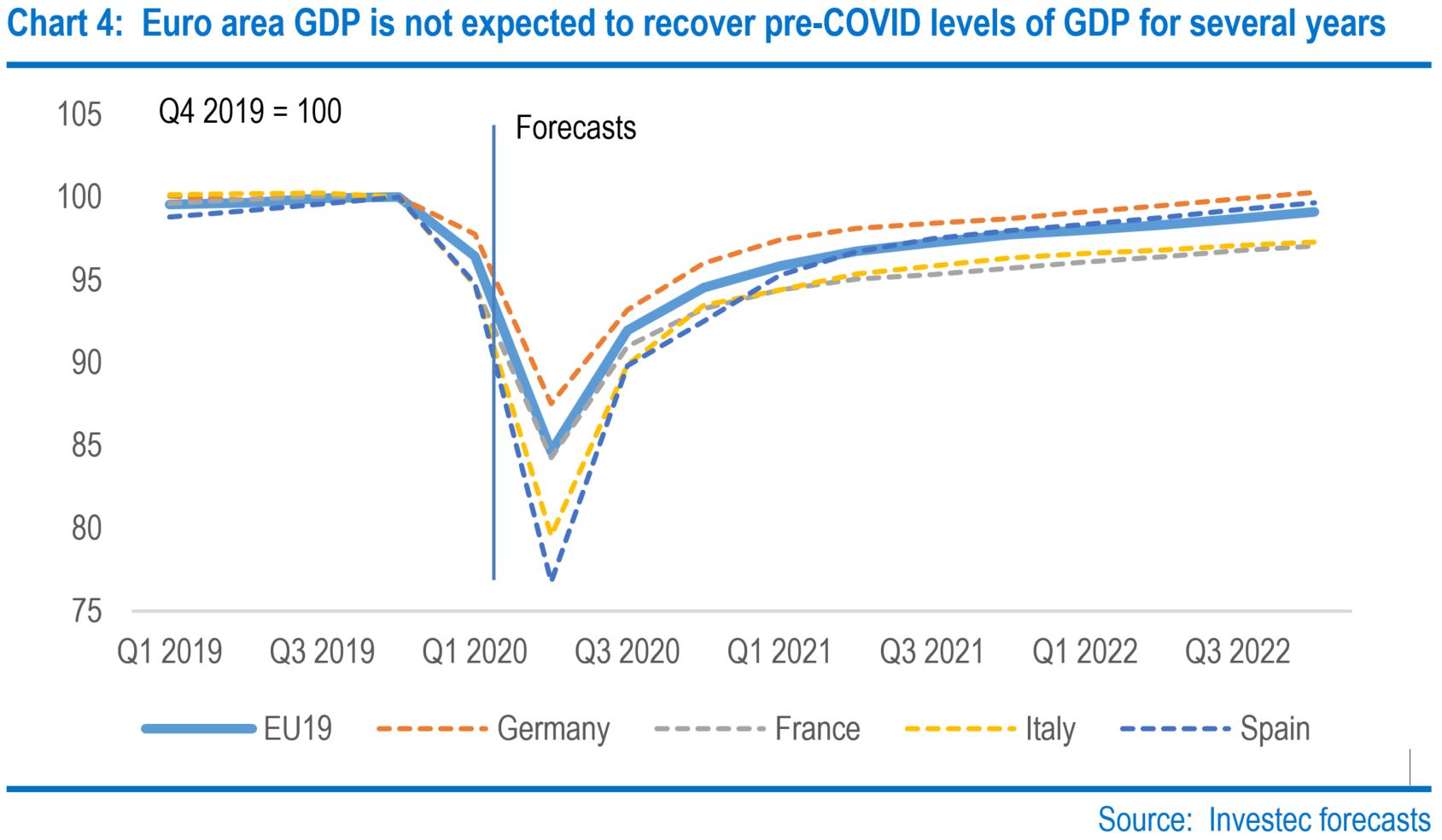

Signs of economic activity rebounding within the euro area have continued to coincide with the gradual relaxation of lockdown rules, with mobility now just 10-20% below pre-coronavirus levels, having been down more than 75%. We continue to envisage a strong rebound in GDP growth following what is expected to be a 12% fall in the second quarter, which puts our 2020 GDP estimate at -7.9%, a very marginal revision from the -8% forecast in May. Meanwhile, 2021 will see a rebound of 5.5%. Against this backdrop, the European Central Bank (ECB) continues to be active, introducing an additional €600 billion in asset purchases, which combined with significant drawings under the ECB's third series of targeted longer-term refinancing operations (TLTRO III), should help to ease financing conditions. But with the inflation outlook muted, we would not rule out further ECB action in the future.

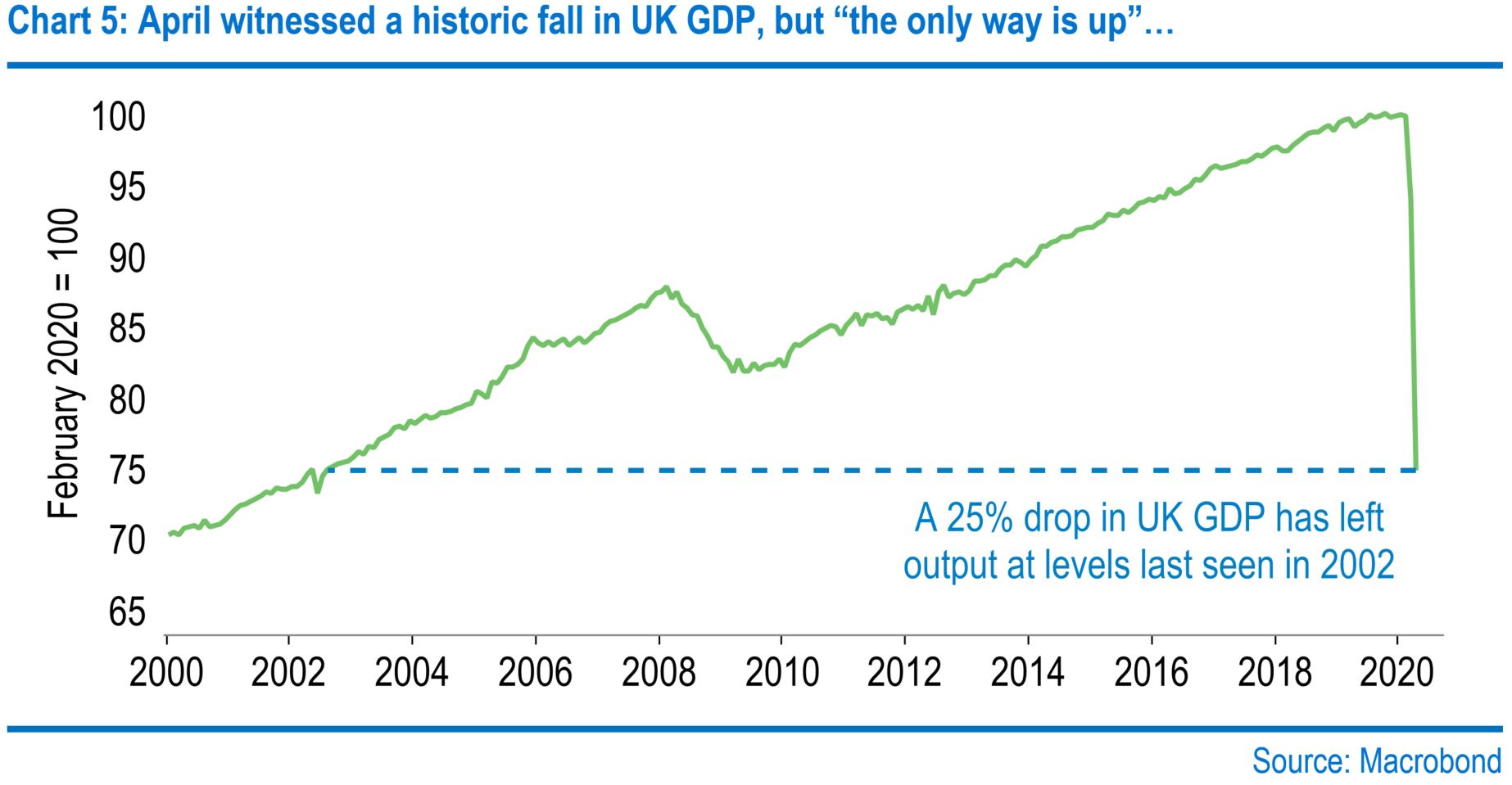

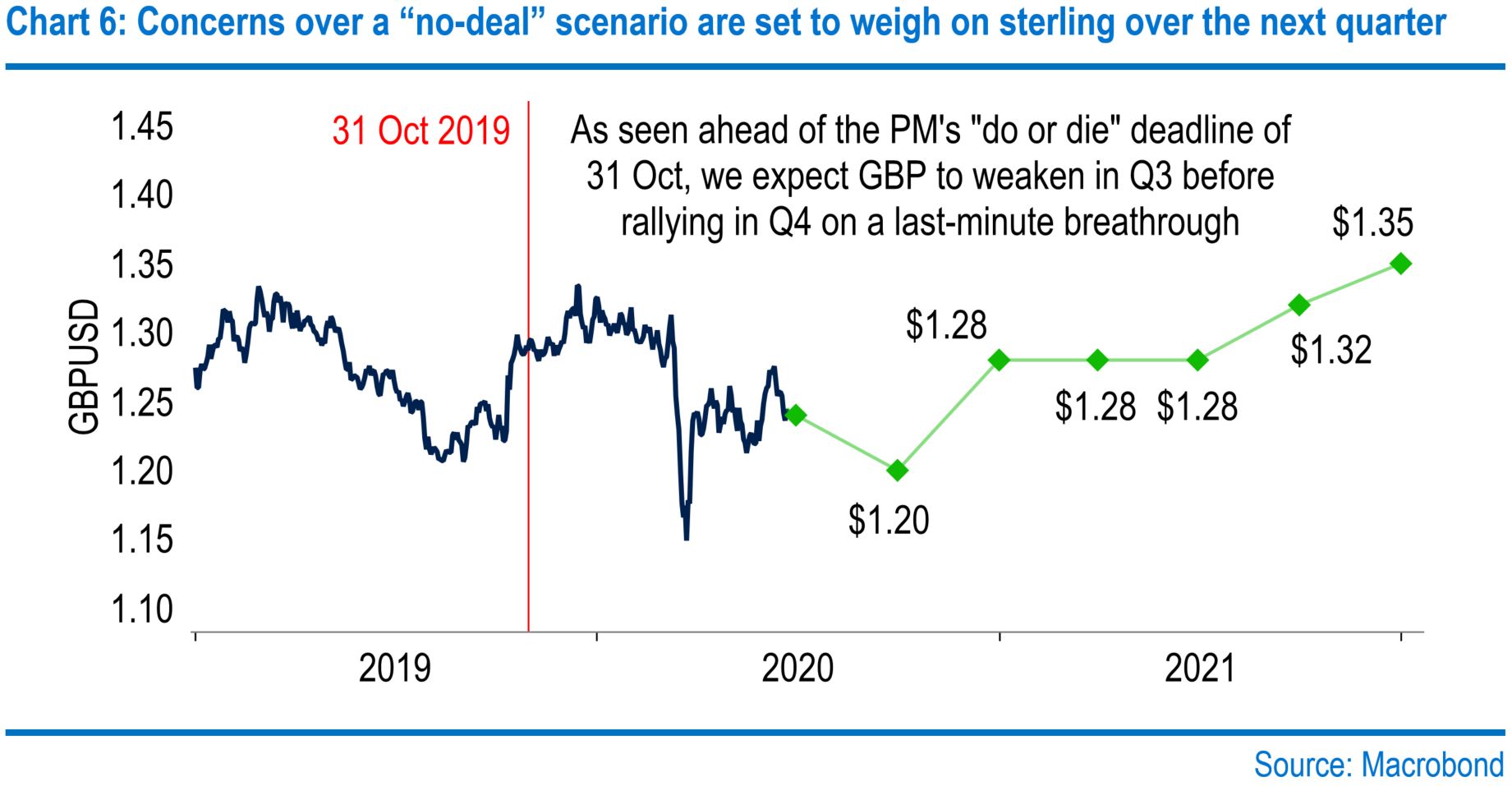

GDP plummeted by a record 20.4% in April during the first full month of lockdown. But this should mark the nadir of the downturn, with UK Purchasing Manager Indexes (PMIs) and other data indicating that activity has picked up across the remainder of the second quarter. This positive momentum should be sustained into the third quarter as the hospitality and tourism sectors are permitted to re-open, aided by the reduction in the 2-metre distancing rule. We now look for a GDP contraction of 7.9% in 2020 (previously 10.8%), followed by a rebound of 6.1% in 2021 (previously 9.7%). After Covid-19, UK-European Union trade negotiations pose the next most prominent risk to the outlook. While we suspect a last-minute agreement will be reached, the pound is likely to weaken as investors weigh up the risk of a disorderly "no-deal" outcome. We now look for sterling to finish the third quarter at $1.20 (previously $1.25) before rallying to $1.28 (previously $1.26) by the end of the year.

Global

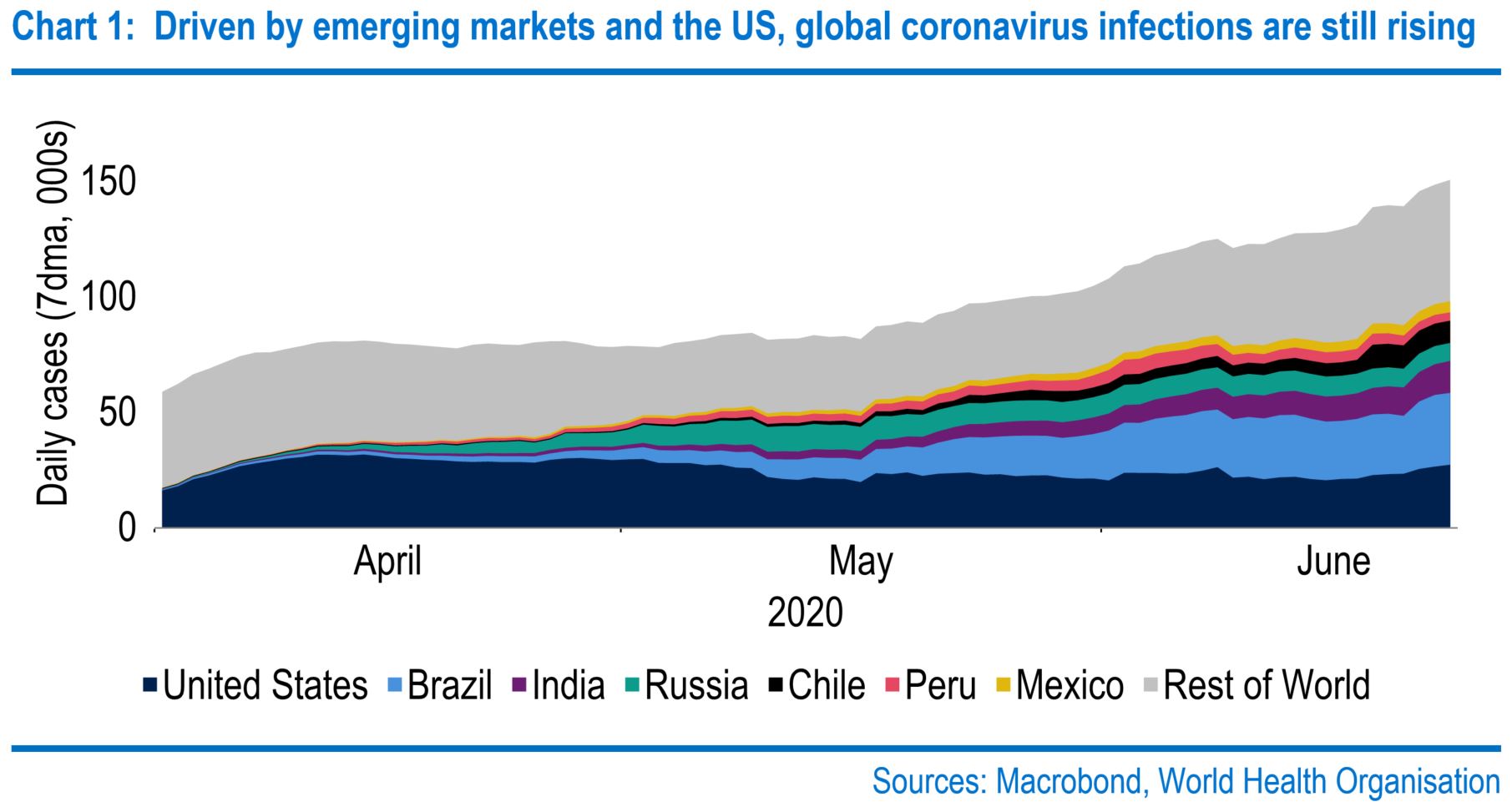

The evolution of the coronavirus, plus the responses by authorities, continue to be the primary drivers of global growth prospects and financial market sentiment. Broadly, countries can be divided into four main groups. First, Pacific Rim nations have dealt with the pandemic promptly. Second (most) European countries are unlocking their economies gradually as infections fall. Third, in the US, many states are unwinding lockdowns rapidly, even though new Covid-19 cases are rising, risking a second wave nationally. Lastly, some governments have not brought the pandemic under control at all and economic chaos beckons. That fits some emerging-market countries, such as Brazil.

The varying stages are reflected in a range of economic indicators across countries, including the Citi Economic Surprise Index. Globally, this has tracked back up close to the neutral level, but there are considerable disparities across geographies. The US economy has fared relatively well, as activity has responded to the easing of restrictions and stimulus measures. Meanwhile, the UK and the euro area are languishing. Recently, though, positive PMI surveys for June have driven the figures higher in both jurisdictions.

While the Chinese economy is recovering, question marks remain over the scope of the pick-up. May’s activity data fell short of expectations. Chinese annual industrial production growth firmed to 4.4%. But given current world economic conditions, the pace of factory growth is struggling to catch up with 2019’s 6%. Also, the recovery in Chinese retail sales is still tepid - May registered an annual decline of 2.8%. While the latest Covid-19 outbreaks in various Chinese regions may not have a direct material impact on total spending, they could contribute towards broader consumer caution. China's National Bureau of Statistics indicated some sluggishness in the rebound, hinting that the economy "might" return to growth in the second quarter depending on the strength in June. Our Chinese GDP forecast for this year remains a cautious -0.3%.

Globally, two principal factors have pulled our GDP forecasts in opposite directions. First, we are concerned about the outlook in emerging-market economies such as Brazil and India and have downgraded their outlooks. Second, anecdotal evidence in several developed economies points to the hit to GDP in the second quarter being less dramatic than we had expected. Although we have correspondingly moderated our view of the third-quarter upturns, the result is a more modest amount of lost output and therefore an upgrade to specific 2020 GDP forecasts, but down for 2021. The net effect in 2020 is a global downgrade to -4.1% (previously -3.9%), while our figure for 2021 is now +5.3% (previously +6.8%).

Although we have adjusted our forecasts to take account of the continued climb in Covid-19 infections in various emerging-market countries, we are not incorporating formal second waves in our numbers. Were this to happen to a significant degree, resulting lockdowns would have a material impact on growth prospects. The Organisation for Economic Co-operation and Development recently completed an exercise assessing the effect of such a "double hit" striking later this year, seven months after the initial impact. Its overall conclusion was that world growth could be a further 1.6 percentage points lower this year and 2.4 percentage points lower in 2021. The Eurozone would be notably vulnerable, "losing" 2.4 percentage points of growth this year and 3 percentage points in 2021.

Stocks have suffered from periodic jitters over the Covid-19 picture in emerging markets and fears of a second wave. But the net effect has been a further rally in risk assets as restrictions have been eased and more recent economic data have strengthened. The MSCI World Index is currently up 40% from its March low. US equity indexes have outperformed, with the S&P 500 now just 7.5% off its record high. Notably, the FTSE 100 and Stoxx 50 indexes have both underperformed the MSCI EM index. Also critical is vaccine development. Some 150 are currently in development, with two in Phase 3 trials. Perhaps boosted by the US "Warp Speed" programme, it is hoped that an effective vaccine could be available as early as this autumn.

United States

In April, we highlighted the lessons from the 1918 Spanish flu pandemic where US cities such as St Louis, which eased quarantines sooner, suffered a second wave of infections. While data show that infections are falling sharply in states such as New York and New Jersey, many southern and western states are seeing sharp rises in reported cases. Accordingly, at the national level, we see record daily increases. Although there has been a ramping up in testing, this does not explain away this rising trend. Furthermore, the most robust rises appear often in states such as Texas where the move to ease lockdown happened relatively early. What matters for the economy is whether more restrictions are re-introduced.

The federal administration insists they will not, though state governors will ultimately decide. More data and testing might allow for more tailored restrictions. The initial economic rewards of re-opening will likely reduce appetite for any further closures too. That is especially so with the presidential election due in five months, alongside 11 state gubernatorial races, 33 of 100 Senate seat races and the re-election of the whole House of Representatives. While pent-up consumer demand (and a need for cars amid worries over public transport) boosted headline retail sales in May, it is clear that shoppers are ready and willing to spend.

However, further recovery strides will require material steps in re-opening to recover lost ground. Indeed, the New York Fed's Weekly Economic Index, which combines ten daily and weekly indicators of real economic activity, shows the index still down at minus 8%. We expect the economy to stand about 13% below its pre-coronavirus peak at the end of June, recovering to 4.5% below by the end of the year.

Broadly, we have made relatively modest changes to our GDP forecasts; we look for -5.9% this year and +4.2% next (-5.6% and +4.5% previously). Amid recovering economic activity, the labour market showed surprising resilience in May with a 2.5 million rise in non-farm payrolls. However, job gains were likely boosted by re-hiring of laid-off staff following delayed Paycheck Protection Program loan approvals (and due to the scheme's design). Importantly, the US's U6 unemployment rate, which captures the "marginally attached" and those part-time for economic reasons, is still three times pre-coronavirus levels, rising from 7% to 21%. As Federal Reserve Chairman Jerome Powell said, it is "22 million additional people…. who've lost work in the economy". That is a lot of ground to recover and Mr Powell does not expect this to be reversed overnight.

President Donald Trump is prepping more stimulus, with reports pointing to a $1 trillion package.

The Fed has already embarked on an enormous stimulus package and has added to this by expanding the scope of its corporate bond buying, as well as now having launched a so-called main street lending programme. However, amid worries over the longevity of the jobs market impact, it is getting ready in case more is needed. Namely, it is considering yield curve control and more explicit forward guidance. However, it is not keen to leap in quickly with such initiatives. For now, the Fed favours using its "dots" to guide markets. The dots point to flat interest rates for the foreseeable future and no appetite for a negative Federal funds target rate.

President Donald Trump is also prepping more stimulus, with reports pointing to a $1 trillion package. His appetite for such a package has no doubt been spurred on by recent polling - Democratic presidential candidate Joe Biden has a firm lead in national polls. More importantly, recent state-level polling shows Mr Biden leading in key swing states Mr Trump won in 2016. For the president, there is worse news. Two very recent polls showing Mr Biden extending his gains in recent days following Black Lives Matter protests - one put Mr Biden ahead by 16 points in Michigan and President Trump just 1 point ahead in Iowa. Mr Trump won Iowa by 9 points in 2016, so this implies a large swing away from him.

Eurozone

The ECB's Governing Council meeting in June saw the central bank ramp up its response to the Covid-19 crisis, with a €600 billion rise in its Pandemic Emergency Purchase Programme (PEPP) to €1.35 trillion and an extension of its timeframe to June 2021. That marks a significant step up in its policy response, with May's asset purchases already outstripping the monthly pace of buying at the start of the year by seven to one, and highlights the Governing Council's concerns over the economic and inflation outlook. Some of the rationale for the move was to return inflation to its pre-coronavirus path. But it is worth noting that previous projections in March already envisaged an undershoot of the ECB's inflation target of below, but close to, 2%. The ECB projected inflation of 1.6% in the fourth quarter of 2022, a level which was deemed "unsatisfactory". Hence additional easing seems likely.

Interestingly, the ECB has also started publishing more granular data on its PEPP purchases, which highlights the flexibility in its approach, overbuying Italian bonds to the tune of €18 billion relative to the capital key since March. The detail also revealed that the ECB bought Greek government bonds for the first time. Additionally, the ECB has also sought to ease financing conditions through TLTRO III, where the latest drawdown saw banks borrow a vast €1.3 trillion, a net liquidity injection of €548 billion. Ultimately, this should support credit conditions and lower borrowing rates given that banks can borrow these funds at a rate as low as -1%.

However, the more critical determinant of the near-term economic rebound is the relaxation of lockdown rules. Here anecdotal evidence from sources such as Google's mobility reports has pointed to activity returning towards normal with mobility now 10%-20% down on pre-coronavirus levels in many euro area countries, having been down more than 75% during April. Economic indicators such as the PMIs have posted similar trends with June's PMI Composite Index surging to 47.5 One key focus of European nations has been to ease rules ahead of the crucial summer holiday season. For a number of countries, including Spain, Portugal and Greece, tourism exports represent more than 5% of GDP.

As such, travel restrictions have now been relaxed among Schengen countries. However, it remains to be seen to what degree individuals will be willing to travel abroad amid continued uncertainty. Indeed, beyond an initial rebound in economic activity post lockdown, questions remain over the subsequent speed of the recovery. A critical point here is the evolution of the labour market. Despite various schemes aimed at reducing permanent layoffs, the rate of unemployment is set to rise sharply, introducing a significant economic headwind and resulting in a long road to recovery. At the end of 2022, the ECB's forecasts see unemployment at 9.1%, still 2% higher than the 7.1% recorded in February.

Near-term, we expect the euro-dollar exchange rate to remain around current levels as the market awaits more concrete signs on the economy and ECB policy.

In this sense, fiscal policy will play a role in the long-term recovery, where the last month has seen Germany agree to a €130-billion stimulus package. Meanwhile, the European Commission has built on German and French proposals to set out a €750 billion EU Recovery Fund. Of this, €310 billion will be distributed as grants under a "Recovery and Resilience Facility", with Spain and Italy set to receive almost half. Still, an agreement between all 27 EU member states needs to reached and opposition remains. A specific gripe is over the formula which allocates funds. A feature here is average unemployment over 2015-19, which dissenters argue has no direct connection to the current crisis. This stimulus should help promote long-term recovery, but we do not envisage GDP returning to pre-coronavirus levels until the fourth quarter of 2022.

Despite the euro area's problems with coronavirus this year, the single currency is currently 4% higher year-to-date against a trade-weighted basket. It is now flat against the US dollar, following a 3% rally from late-May - at its peak earlier this month, the euro breached the $1.14 level. Supporting factors here include hopes over the economic recovery, easing lockdowns, and improving risk sentiment eroding some of the US dollar's haven demand. Near-term, we expect the euro-dollar exchange rate to remain around current levels as the market awaits more concrete signs on the economy and ECB policy. But longer-term, we remain of the view that the euro will strengthen and forecast $1.16 by the end of 2021.

United Kingdom

Recent GDP figures have laid bare the economic toll of the lockdown. Output slid by an eye-watering 20.4% month-on-month in April, easily surpassing March’s 5.8% drop as the sharpest contraction on record. Consequently, the UK economy is now 25% smaller than pre-pandemic levels, with GDP standing at a level last seen in 2002. But while the magnitude of the downturn is unprecedented in modern times, so is the speed at which it has come about. For comparison, the financial crisis incurred a peak-to-trough fall of 6.9% over the space of 13 months. Still, we suspect April will have marked the nadir of the downturn, with restrictions gradually eased from May onwards. Activity has picked up as a result, with the UK composite PMI rising off April’s record low of 13.8 to reach 30 in May and 47.6 in June.

Although this excludes retailing, official figures show that sales rebounded 12% in May and further gains are likely in the coming months amid the re-opening of non-essential retailers on 15 June. There has also been widespread improvement in less conventional data sources. Figures from the National Grid show electricity demand is down 10% on the year, having been as much as 25% lower in April. Also, the Automobile Association (AA), reports that traffic levels have doubled from their lockdown lows and are now similar to those seen in the early 1990s.

Next month should see another step-up in activity after the re-opening of the hospitality sector on 4 July and the reduction in the 2-metre distancing rule to "1-metre plus". There is also speculation that Chancellor Rishi Sunak is considering a temporary cut in Value-Added Tax (VAT) from its current rate of 20%. That would be expensive - the Treasury estimates that every 1 percentage point drop in VAT incurs an annual cost of £7 billion. But reports suggest such a move will be followed by deferred tax rises and lower spending in the autumn budget. We have not incorporated any explicit fiscal assumptions into our forecasts, but we have adjusted for April’s GDP drop being more modest than we had initially projected. We now look for a contraction of 7.9% in 2020 (previously 10.8%), followed by a rebound of 6.1% in 2021 (previously 9.7%).

Another source of surprise has been the labour market, with the unemployment rate steady at 3.9% in the three months to April. However, most other metrics have pointed to a deterioration in conditions. Employment plummeted by 429,000 in April alone, whereas the claimant count rose to a 15-year high of 7.8% in May. Also, a 342,000 quarterly drop in vacancies was the largest since the series began in 2001. One reason for this dichotomy may be the furlough scheme, but we suspect sampling variability in how the data is collected may be another factor. As such, we expect unemployment will rise gently until the end of the furlough scheme in October, before spiking to a peak of about 8% in the fourth quarter.

Brexit negotiations are set to weigh on the pound. We now look for sterling to finish the third quarter at $1.20, before rallying to $1.28 by the end of the year.

With the £200 billion of quantitative easing (QE) launched in March set to end next month, the Bank of England’s Monetary Policy Committee voted 8-1 for an additional £100 billion in June. Amid a stabilisation in liquidity conditions, the pace of purchases will roughly halve and adjusting for the replacement of redemptions, gilt purchases will be cut by 55% up until early-August. The new targeted stock of £745 billion will be achieved around the turn of the year. BOE Governor Andrew Bailey has suggested this stock is likely to shrink before any rate increases, a departure from his predecessor who indicated that the BOE's main interest rate - Bank Rate - would be raised to 1.5% before any unwinding of QE. However, we don’t expect to see this happen any time soon given our expectation that Bank Rate will not be raised to 0.25% until late-2023.

For the meantime, Brexit negotiations are set to weigh on the pound. 10 Downing Street formally rejected an extension to the Brexit transition period ahead of this month’s deadline, meaning it will expire on 31 December. It has also announced relaxed controls will apply to goods arriving from the EU in the first half of 2021 whether a free-trade agreement is agreed or not. As things stand, the two sides remain far apart on several crucial issues, but we suspect a last-minute agreement will be reached. However, this brinkmanship means that sterling is likely to weaken as investors weigh up the risk of a "no-deal" outcome. We now look for sterling to finish the third quarter at $1.20 (previously $1.25), before rallying to $1.28 (previously $1.26) by the end of the year.

If you would like to discuss how the coronavirus impacts your exposure to risk, get in contact with us

Browse articles in