We're all bond investors now

Government Bonds, especially US Treasuries, seem to be dominating financial markets. The recent rise in US Treasury yields has sent reverberations around the world from NASDAQ to the UK’s FTSE. Why and when did equities become so closely linked to the interest paid on a piece of US Government debt?

Get Roger Lee’s Equities delivered to your inbox

Government Bond Yields: historically tangential to equities

Occasionally, the stress in Government bond markets has flowed over into Equity markets. For example, the European Sovereign Debt crisis, had a profound effect on equity prices for several months until ECB President Mario Draghi’s famous July 2012 “whatever it takes” speech which effectively resolved the crisis and led to a sharp recovery in both equities and peripheral Eurozone debt.

While government bond yields are generally driven by growth and inflation expectations, the same principal drivers of equities, I never sensed it was bond yields themselves driving equities other than during those periods of stress.

Historically the impact of Government bond yields on equities has been more tangential. Bond yields were merely another coincident expression of those more powerful forces of growth and inflation.

Well not so anymore, as could be seen so clearly during the last week of February. A weaker than expected auction of US 7 yr Treasuries, triggered a major sell-off in the broader US Treasury market. The benchmark yield on 10 yr US Treasuries rose 0.16% in a day to over 1.6%.

But why did a 0.16% rise in the 10 yr US Treasury yield directly lead to a 4% sell-off in NASDAQ or even a 3.5% decline in our FTSE? How have equity markets gone from broadly ignoring government bond markets to being dictated by them?

I believe bond yields have become increasingly important in equity investing. I would even go so far as to say the recent repricing of US Treasuries since the Pfizer vaccine announcement has become the most dominant factor driving equity valuations and equity performance in the stock market.

Required return of equities: entwined with the risk-free rate

Investors when making any investment will have a return threshold or a “required rate of return”. On the face of it “required rate of return” is something most could answer intuitively based on personal circumstances. If our required return rises and nothing else about our investment changes, the value of that investment must fall so it can still meet our higher required return. Conversely, if our required return falls and the characteristics of our investment remain unchanged, then the price or value of that investment will rise if it is to meet our lower required return.

Again intuitively, most investors as part of their required return will reference what they can earn “risk-free”. So our required return is directly linked to what we can earn “risk-free”.

As the risk-free rate rises, our required return should rise and so asset prices should fall to reflect that higher required return. Equally, if the risk-free rate falls our required return falls and asset prices should rise if they are to meet that lower required return.

It is through this mechanism that an investor’s “required return” is entwined with the “risk-free rate”. The “risk-free rate” is usually expressed as the yield on the benchmark US 10 yr Treasury yields.

This is how Equity prices and valuations are directly linked to US Treasury yields.

The theory behind these concepts of “required return” can get very complicated very quickly and forms the basis of most practical and theoretical equity valuation models. This includes the “Dividend Discount Model”, the “Capital Asset Pricing Model (CAPM)” and at least one Nobel Prize.

For a more detailed discussion on why the risk-free rate is important to our required return and therefore equity valuation, click the link below to read a detailed summary.

Why is the risk-free rate so important to equity valuations? >

Recent moves in US Treasury yields: proportionately more impactful

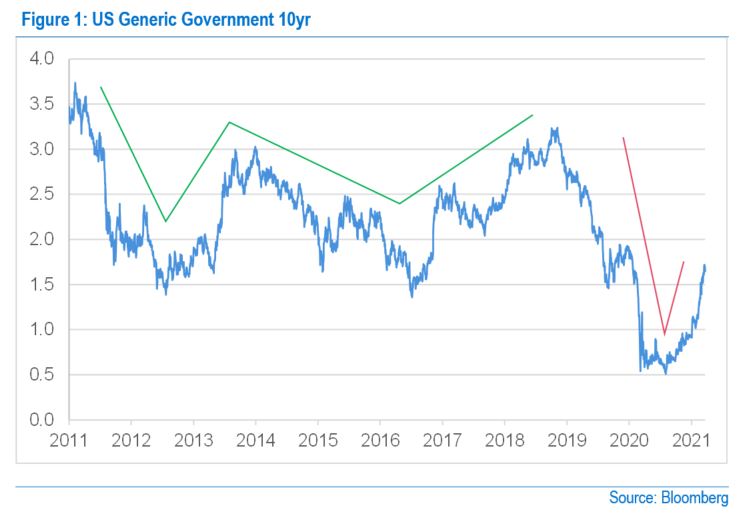

So now let’s look at how that risk-free rate as expressed by 10 yr US Treasury yields has changed over the last decade.

From the beginning of 2011 until almost the end of 2018, despite some significant swings, US Treasury yields did very little over those eight years (as can be seen in figure 1), even when the Federal Reserve gradually raised interest rates from December 2015 as the US economy recovered from the Financial Crisis.

However, towards the end of 2018, the market was becoming increasingly concerned that the Feds interest rate rises were too aggressive and were likely to have a detrimental effect on inflation and economic growth. As these concerns grew the Fed responded and started to reverse interest rate policy. US Treasury yields started to fall.

This was mirrored recently when fears over the pandemic escalated. Growth expectations were slashed and the Fed responded by cutting rates to effectively zero. By August 2020, US Treasury yields were now the lowest they had ever been - a touch over 0.5%. The yield on 10yr US Treasuries had fallen from 3.25% in October 2018 to 0.5% in just over 18 months. In effect, the “risk-free rate” had collapsed 85%.

So while in the distant past a fall in yields or the “risk-free rate” from say 3.5% to 3.25% as we saw from the start of 2011 to the end of 2018, may not have had a material impact on an investor’s required return, a change from 3.25% to 0.5% should proportionately be far more impactful. Likewise, a jump from 0.5% to 1.5% in the last few months should also have a far more disproportionate and amplified effect.

At least that is what the theory around “required return” would suggest.

This grip that bond yields have on equities at the moment can be frustrating, especially for company management teams. But it is equally frustrating for many seasoned institutional equity investors and must be truly perplexing to most retail investors.

Quality Growth: ironically predictable returns more exposed to bond yields

There are a group of stocks that are perceived to have predictable and growing future returns. The mega-cap tech names in the US are perhaps the best examples of companies that display these characteristics. Perhaps not surprisingly, this group of stocks are commonly referred to as “quality growth” companies.

Ironically, it is these quality growth companies that seem most exposed to falling and rising bond yields. As the “risk-free rate” started to fall towards the end of 2018, then fell dramatically during the pandemic, theoretically, the value of those future predictable returns should rise.

However, if the theory is correct, the reverse should also be the case. If the risk-free rate goes up then the value of those future returns must be worth less. Since the 0.5% low in US Treasury yields in August, yields have risen to around 1.5%. The concern is that they will rise even higher as economies reopen, especially if more direct stimulus is made available in the US.

So as yields fell 85%, these quality growth companies should significantly outperform the broader market. But more recently, as yields have almost tripled from their lows, we would expect to see these quality growth companies underperform the broader market.

A UK quality growth basket: theory tested by reality

To demonstrate the effect US Treasury yields have on UK-quality growth stocks, we have put together a basket of five companies that show the features of quality growth companies. This is subjective, but we have chosen: AstraZeneca PLC, Experian PLC, Ocado PLC, RELX PLC and Rentokill PLC.

We have then constructed an equally weighted basket of these stocks relative to the FTSE All-Share to demonstrate when these stocks are outperforming and underperforming the wider market. We then inverted this performance to see how closely their positive performance followed a decline in US Treasury yields. The results are shown to the right:

The relationship between US Treasury yields and the performance of this type of stock is remarkable as shown in figure 2. What we have seen over the last couple of months isn’t anything new. Except now the correlation is causing these sort of stocks to underperform.

Nothing has really fundamentally changed in how these companies are run, except the one factor that their management teams cannot predict or control: US Treasury yields. This has been especially true since the end of 2018 when US Treasury yields started their precipitous fall and then their steep rise over the last couple of months. These moves in yields since the end of 2018 have just been proportionately more impactful than in the past.

Fundamental drivers to US Treasury Yields: growth and inflation

If we accept that bond yields are a significant driving force in equity valuations and performance, as well as looking at company fundamentals, we now have to consider the direction of Sovereign Bond yields and what is driving US Treasury yields in particular. The two fundamental drivers to US Treasury yields are that familiar combination of economic growth and inflation expectations.

This brings us back to where we are today in our response to the pandemic. Since the Pfizer vaccine announcement in November, markets can see a path back to normality. As I write, we are at a pivotal moment waiting to see what the recovery looks like after the lockdown is lifted. This reopening of economies is posing some fundamental questions around the future trajectory of both growth and inflation:

- Will the cash balances built up because of “enforced saving” during lockdown for those who still have employment be translated into repressed demand and a consumer boom?

- Will the global supply chain be able to meet any surge in demand or will demand exceed short term supply and prices rise?

- Will those rising prices lead to a spike in inflation?

- Will another round of US stimulus add fuel to an already recovering US economy?

- Or will the recovery be more modest with job losses and rising unemployment after governmental support is removed, depressing future demand and wage growth?

- Instead of causing an inflation spike, will the latest US stimulus avoid a slide into an economic slump as the scarring of the pandemic becomes apparent?

Financial markets will continue to focus on the economic data in its attempt to reprice US Treasuries until there is a clearer answer to these profound questions of what growth and inflation look like post-pandemic.

US Treasury Yields: the most dominant factor driving equity valuations

The equity market will be especially fixated as any repricing of US Treasuries is effectively a repricing of the risk-free rate, fundamental to equity valuations. Any data point that moves the debate forward is likely to cause powerful, outsized market reactions, as we saw at the end of February following that disappointing US Treasury auction.

So having ignored bond yields for much of the first 20 years of my career, in the last few years I believe bond yields have become increasingly important in equity investing. I would even go so far as to say the recent repricing of US Treasuries since the Pfizer vaccine announcement has become the most dominant factor driving equity valuations and equity performance in the stock market.

This grip that bond yields have on equities at the moment can be frustrating, especially for company management teams. But it is equally frustrating for many seasoned institutional equity investors and must be truly perplexing to most retail investors. But from the equity market to the board room to main street - at least for the time being, whether we like it or not - we’re all bond investors now.

I would like to thank Investec Credit Analyst, Thabo Ndebele for his invaluable assistance in constructing the basket described in this article.

Get Roger Lee’s Equities delivered to your inbox

Disclaimer: The blog does not aim to give investment advice, but is designed to afford relevant longer-term context to investors, encouraging a broad perspective where uncertainty is high and a spirit of learning is important. The views expressed are those of the author, not those of Investec.

Browse articles in