2020 vision? A view of the global economy this year

After a turbulent 2019, businesses and investors start a new decade with a sense of cautious optimism. We forecast that global economic growth will strengthen this year, but the risks and uncertainties that curbed momentum last year will linger, threatening to derail the outlook once again. We analyse the key challenges and what they mean for the world’s major economies.

- Driven by emerging markets, global economic growth will increase to 3.3% this year after a post-crisis low of 2.9% in 2019.

- The strengthening in global activity is unlikely to be enough to trigger a mass reversal of 2019’s widespread interest rate cuts. Indeed, we expect further easing by various major central banks, including in the US, eurozone, Australia, and China.

- The US economy looks set to run against the grain, with growth slowing to 1.8% from 2.3%. We see the Federal Reserve cutting the fund's target range by 0.25% to 1.25%-1.50% in the first quarter and do not expect a hike until the end of 2021.

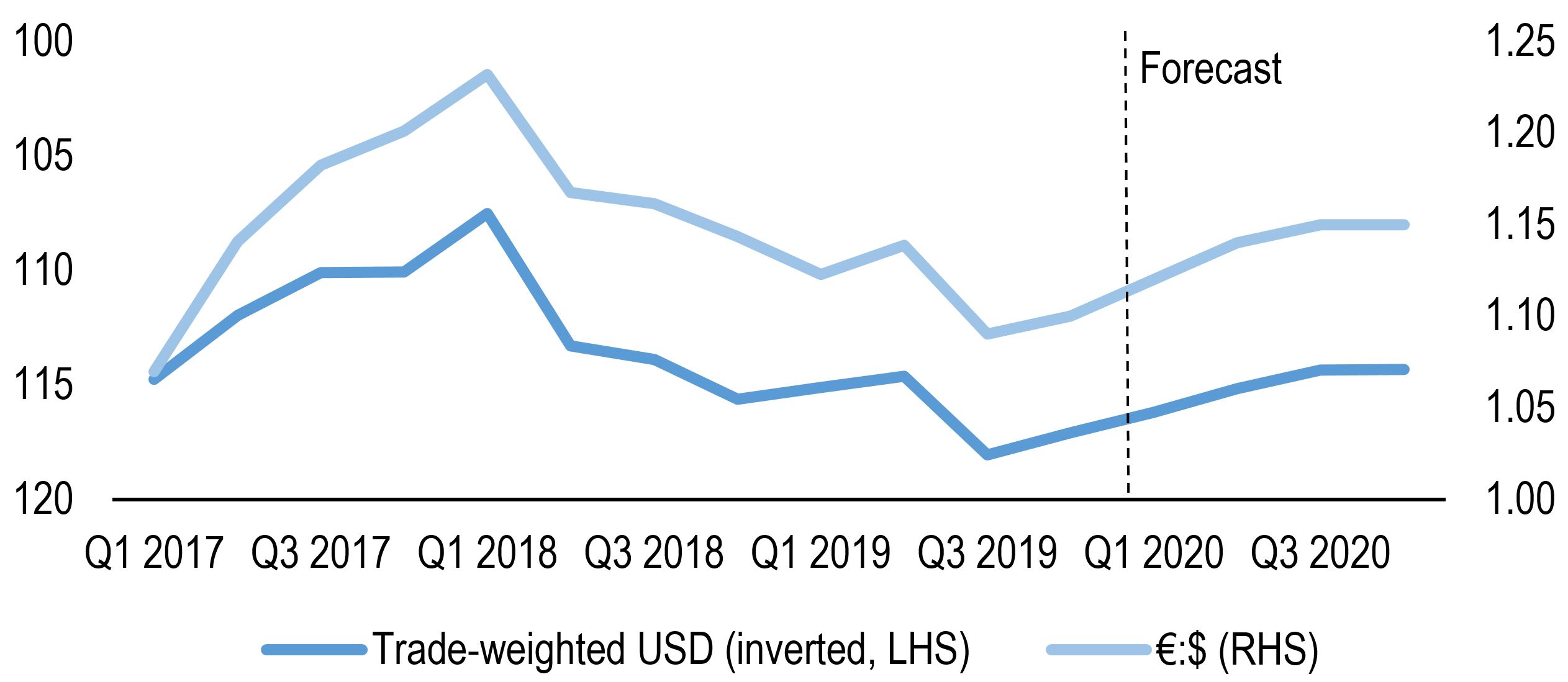

- While the weakness of manufacturing is having a dampening effect on eurozone economies, especially Germany, there are few signs yet of a spillover into services. Indeed, recent data hint that the sector may have bottomed out. While a 0.1% cut in the European Central Bank’s deposit rate to -0.60% looks likely in the first quarter, an increase in asset purchases beyond the current €20bn per month is doubtful. We expect the euro to make modest gains against the US dollar and end 2020 at $1.15.

- In the UK, the decisive win of Boris Johnson’s Conservative Party in December’s election means the government should be able to pass the legislation needed for the UK to leave the European Union on 31 January. Britain will then enter a transition period until at least the end of the year.

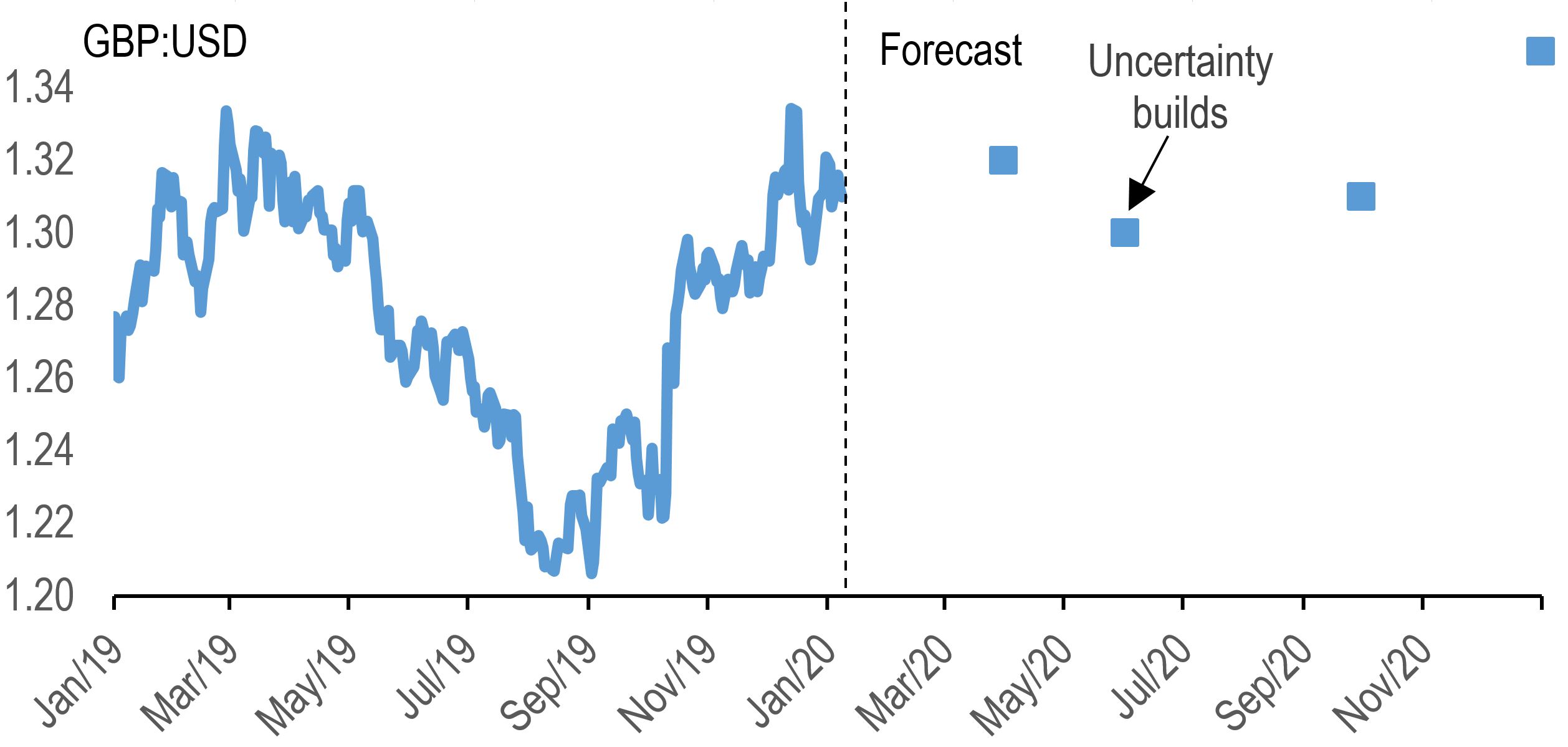

- But uncertainty over a UK-EU free-trade agreement may become a significant focus during the year as markets recognise that negotiating a deal by the end of 2020 is ambitious. We envisage sterling trading at $1.35 and 85 pence against the euro at the end of 2020, but expect some jitters in the meantime, perhaps around mid-year.

- Our 2020 UK economic growth forecast is 1.2%, weaker than 1.3% in 2019, but this is an arithmetic quirk. Average quarterly growth will be a touch firmer at 0.4%, supported by some strengthening in investment as Brexit uncertainties ease somewhat. In this scenario, we forecast the Bank of England’s keeping interest rates at 0.75% through 2020.

- Downside risk and uncertainties prevail though much of our global assessment, including surrounding the US-China trade talks.

Global upturn

After the world economy grew at the slowest rate since 2009 last year, we expect this year will see a recovery. This strengthening partly reflects the unwinding of weakness in specific emerging markets, namely India, Brazil, Russia, and Turkey. But there is also likely to be a modest pickup in underlying activity, driven by lower interest rates, a prospective easing of US-China trade tensions, and fiscal stimulus in countries such as Australia, the UK and (perhaps) Germany.

Still, that positive outlook will be jeopardised if US-China talks break down and more tariffs are imposed. There is an acute need for resolution on trade issues after commerce between the two countries suffered last year. The Chinese economy grew an estimated 6.2% in 2019. But this year looks more difficult, even with government support and the first phase of a trade deal with the US. We see China’s gross domestic product (GDP) increasing 5.9% in 2020, the first time in three decades that growth has dipped below 6%.

Central bank policymakers have cried for fiscal stimulus to mitigate the effects of the trade war. In particular, Germany has a budget surplus, giving it room for manoeuvre. But space for government stimulus elsewhere may be limited, so prospects of globally coordinated action in 2020 are probably optimistic.

In summary, our baseline view sees a pickup in growth, but nothing so robust to trigger a widespread reversal of 2019’s interest rate cuts. Indeed, we suspect that central banks such as the Fed, ECB, RBA, and PBoC will begin 2020 by easing further. Some may consider this a “Goldilocks” scenario. But downside risks may be pronounced for much of the year, with the recovery muted and the second phase of a trade deal between Washington and Beijing possibly not settled until after November’s US presidential elections. We see the environment supporting currencies such as the euro and the pound to make modest gains against the dollar.

Chart 1: Improving growth backdrop – euro-dollar and trade-weighted dollar forecasts

The United States cools

US economic growth slowed last year due to global trade tensions, with manufacturing and business investment notably weak, while fiscal policy has also acted as a drag. This year we expect a further slowing, with the subdued outlook evident in business survey indicators, such as the (composite) Leading Index. This gauge is now at just 0.3% year-on-year, only modestly in the black, sending an ominous signal. When it has turned negative in the past, it has almost always preceded a recession. For 2020, we expect GDP growth of just 1.8%, which would be the weakest since 2016, compared with an estimated 2.3% last year.

We see the key driver of the softer growth dynamic this year coming from the consumer sector. One reason is that gains in employment have moderated. Coupled with reasonably static pay growth, this implies a more moderate rise in household incomes this year. Furthermore, costs facing households will rise. Research suggests that rather than Chinese importers to the U.S. bearing the brunt of tariff rises via lower prices, U.S. wholesalers, retailers, manufacturers, and consumers are “left paying the tax”.

Although these factors imply weaker consumer spending, we expect the robustness of the housing market to cap any downside in 2020. This is because lower mortgage rates over 2019 have kicked applications into life. In 2020, we do not expect 30-year Treasury yields (which have driven mortgage rates lower) to rise rapidly, and so we see no sharp softening in housing activity.

Considering the outlook for interest rates more broadly, we do not see 2020 as a year in which the Fed will mark any clear shift in direction. We think Fed Chairman Jerome Powell favours policy that is slightly too loose rather than slightly too tight. As such, and given slowing US economic momentum, we expect 2020 will include very modest policy easing. We forecast a 0.25% cut in the Federal funds rate in the first quarter.

Will 2020 see a turnaround in the prospects for manufacturing and weak business investment? Without a dismantling of tariffs in place, we think not. But we do not expect further deterioration. One question is whether momentum to impeach President Donald Trump persuades him to give more ground in trade talks, raising the chance of a more overarching deal. The argument would be that Trump might choose to be more conciliatory in the hope that having an agreement would help him maintain his support among Republicans, which for now remains solid. While the Democrat-controlled House has voted to impeach Trump, support from his party will help his acquittal in any subsequent Senate trial.

The US economy looks set to run against the grain, with growth slowing to 1.8% in 2020 from 2.3% last year. We see the Federal Reserve cutting the funds target range by 0.25% to 1.25%-1.50% in the first quarter and do not expect a hike until the end of 2021.

The eurozone bottoms out

Recent evidence tentatively suggests the downturn in the euro area may be bottoming out. Notably, Germany avoided slipping into a technical recession in the third quarter, accompanied by signs of stabilisation in the industrial sector. By comparison, the services sector appears to have remained resilient. But though this divergence is due to the nature of the headwinds facing manufacturers (e.g. auto weakness, US-China trade dispute), there remains the risk that the persistent weakness of the sector could spread to the rest of the economy.

The labour market remains tight by historical standards, with the unemployment rate standing not far off its pre-crisis low. That should underpin household spending and reinforce 2020 growth prospects. Credit conditions also look set to remain favourable, with lending to both households and non-financial corporates having proved resilient relative to previous downturns. Fiscal policy also appears on course to play a more active role, possibly even in Germany given that the new SPD leadership is pushing for higher spending amid its efforts to renegotiate the “Grand Coalition.” Finally, we expect export-oriented sectors to benefit from a broad reflation in the global backdrop.

Based on these factors, we continue to look for a marginal pickup in growth from 1.2% to 1.3% in 2020. But the balance of risks remains firmly to the downside. Key among these remains the potential for a US-EU trade war, with the US threatening tariffs on French goods in retaliation to the latter’s Digital Services Tax.

We expect ECB policy will become more accommodative in 2020. We forecast a 0.1% cut in the deposit rate to -0.60% in the first quarter, alongside continuing quantitative easing (QE). But we suspect that this will represent the extent of additional measures. We see the ECB entering an extended pause period as it assesses the impact of stimulus measures now in place, considers its policy framework and also looks to fiscal authorities to do more heavy lifting in driving growth and inflation higher.

Still, we do not think 2020 will be the year in which inflation will robustly converging to target. In the absence of this, our long-term view is that the deposit rate is likely to remain at -0.60% until end-2022. In turn, we suspect that the current pace of QE purchases of €20bn per month will continue until the third quarter of 2022.

One factor that could influence the policy stance is a strategy review the ECB is undertaking this year. The last time the ECB conducted such a survey was in 2003, which created the central bank’s current policy target. This time the review will be broader, focusing on the ECB’s framework, its tools (QE, negative interest rates) and possibly even climate change. However, this may not finish until late 2020, so it is likely to have little impact on policy this year.

Chart 2: Sterling’s movements will continue to centre on Brexit

The United Kingdom takes stock

Following Boris Johnson’s decisive election win, the prime minister intends to pass the EU Withdrawal Agreement Bill (and other legislation) by the end of the month, enabling the UK to leave the EU and enter the transition period. During the transition, which will run until at least the end of the year, the government will negotiate a trade deal with the EU. The joint EU-UK Political Declaration envisages a free-trade agreement (FTA), a looser relationship than set out by former Prime Minister Theresa May.

Several risks surround these talks. Firstly, the time available to strike a deal is limited. The EU is unlikely to agree its collective negotiating position until early-March, leaving 10 months to negotiate. This year may end with “no-deal”, leaving the UK trading with the EU on World Trade Organisation terms.

Secondly, an agreed FTA may involve significant trade frictions if the UK does not subscribe to close regulatory alignment. And thirdly, the British Parliament may insist on scrutiny of the talks, implying a more complicated process. A decision to extend the UK's transition period beyond 2020 has to be made by the end of June.

Consequently, the risks are that the euphoria following the election result and the prospect of passing the Brexit deal could give way to concerns over numerous practicalities. PM Johnson may well be hoping to smooth over such worries with his pledge to lift spending on public services. Fiscal policy will turn more supportive for growth under the Conservatives, as should business investment as a degree of Brexit uncertainty dissipates. Therefore, we look for quarterly GDP growth to average 0.4% this year, double the estimated rate in 2019. However, we look for full-year growth to slip from 1.3% to 1.2% in 2020, owing to less favourable base effects.

Alongside this, we expect the BOE to keep interest rates steady at 0.75% this year with a hike to 1% in mid-2021. But we would not rule out a cut, with two MPC members advocating a 0.25% reduction in December. A key factor will be the policy leanings of Andrew Bailey, who replaces Mark Carney as BOE governor in March. However, we judge that Mr Bailey, who spent 30 years at the BOE, will not want to rock the boat so soon and will mostly follow the path laid out by Dr Carney through 2020.

Still, throughout 2020 there are significant opportunities for uncertainty to build as the Brexit transition deadline approaches.

Table 1: GDP growth forecasts (%)

Source: Investec forecasts, IMF, Macrobond

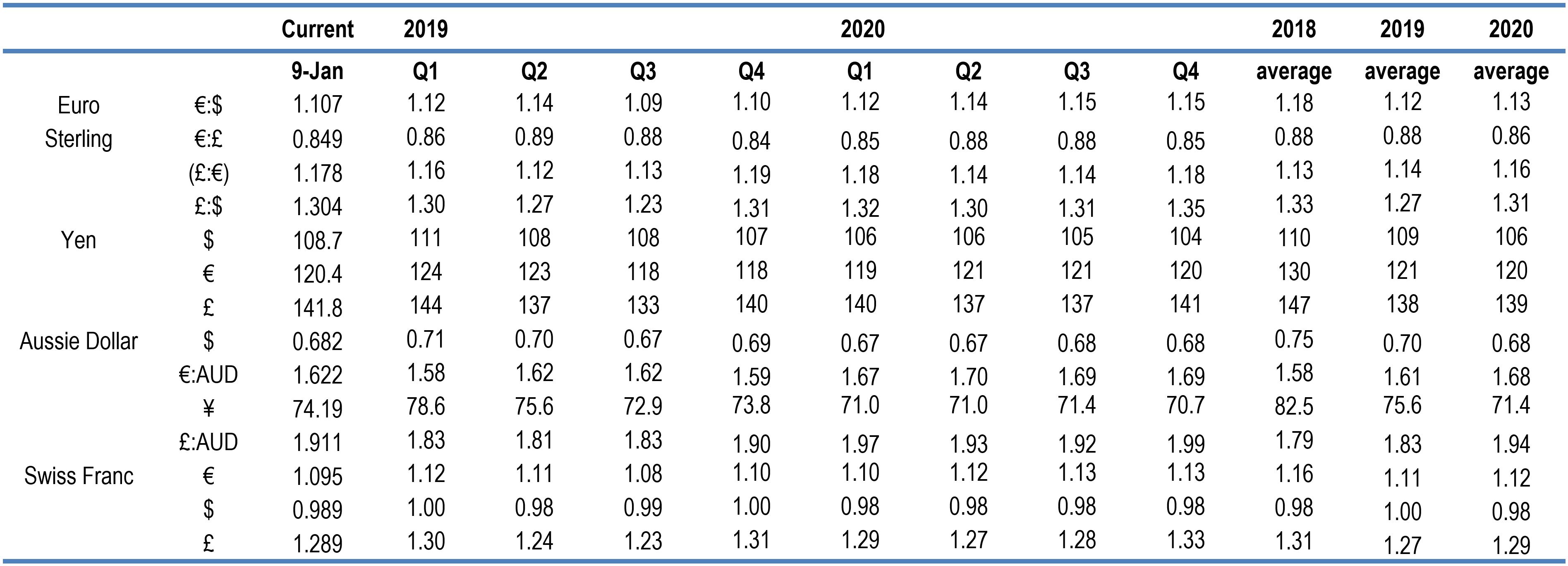

Table 2: FX rates forecasts (end quarter/annual averages)

Source: Investec forecasts, Refinitiv

Table 3: 10-year government bond yield forecasts (%, end quarter)

Source: Investec forecasts, Refinitiv

Investec products you may be interested in

Wealth management

Portfolio management

Offshore investments

Wealth management

Portfolio management

Offshore investments

Key topics in this article

Browse further in