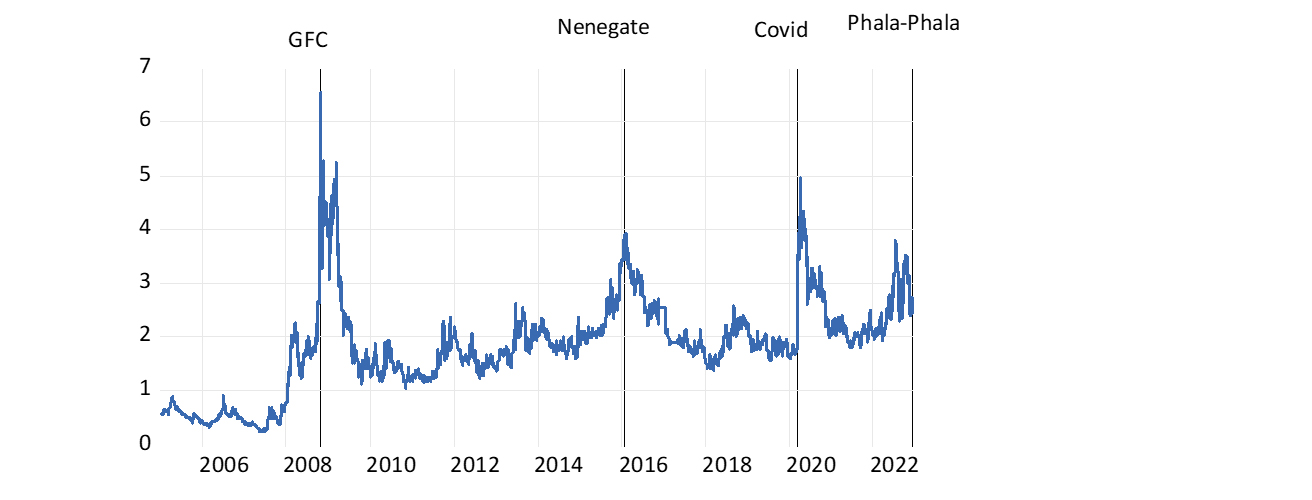

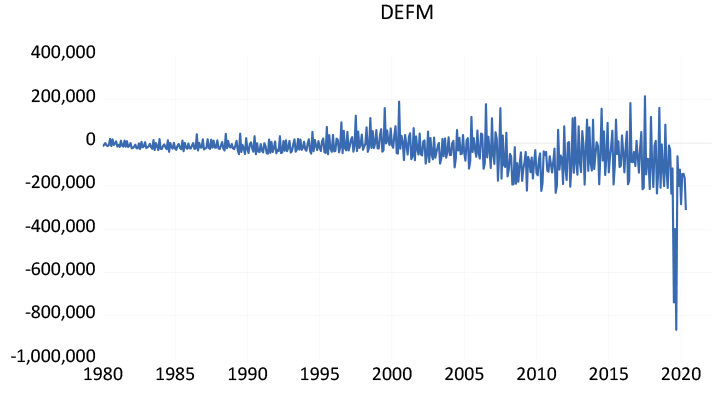

Among the periodic shocks to the SA economy and its financial markets, Phala Phala does not measure severely. It’s more a case of strong tremors rather than an earthquake. The shocks to the economy and its financial markets delivered by the Global Financial Crisis of 2008, the Nenegate crisis of late 2015, and the crisis caused by Covid-19 registered far more strongly and dramatically.

The most appropriate measure of an economy’s status is its credit rating. This can be indicated objectively by the interest rate spread between its debt issues that are payable in US dollars (known as Yankee bonds), and the interest offered by the US Treasury for its debt of the same time to maturity (typically five years). This risk premium is arguably the most reliable measure of sovereign risk – the risk that South Africa will default on its obligation to pay back its dollar debt, or may inflate its way out of its obligations to rand creditors. Between 30 November and the morning of 1 December, when the highly critical report requested by Parliament on President Cyril Ramaphosa was released, this risk spread immediately widened by 46 basis points, from 2.17% to 2.63%. By 7 December, this yield spread had fallen back to 2.5% - about the long-term average.

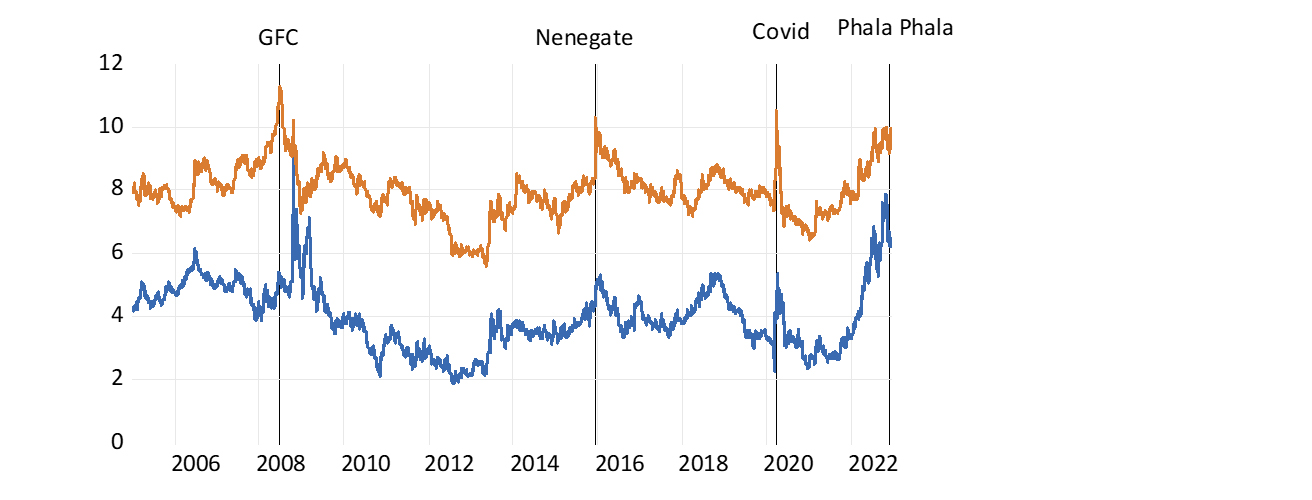

On 1 December the interest yield on the five-year RSA Yankee debt rose from 5.91% to 6.29% overnight, while that on a five-year US Treasury fell from 3.74% to 3.66%. The yield on a five-year, rand-denominated bond rose overnight in predictable sympathy, from 9.34% to 9.96%, more than 60 bps higher.

To compare previous episodes, in early October 2008, before the Global Financial Crisis broke, the SA risk premium was a similar 2%. But by 24 October that month, the risk premium had risen devastatingly to 6.5%. By the end of that tumultuous year, the risk premium had declined to a still elevated and expensive 4%. On 19 October 2015, the sovereign risk premium before Nenegate was an average of 2.4%. But by 20 January 2016, the risk premium had topped out at 3.89%, a 150 bps increase. This declined after the Ministry of Finance had been restored to what was regarded as safer hands.

These events of late 2015 and this year could be described as highly specific to South Africa. They did not have their origin in suddenly more risk-conscious global capital markets spreading greater anxiety about riskier borrowers generally (of which South Africa is one). The next crisis for South Africa was again decidedly global in origin. It came with the Covid-19 pandemic and the lockdowns that followed. In early March 2020, the RSA risk premium stood at 1.79%. By early April it had risen to 4.97% – a more than 400 bps increase before it fell gain. By early 2021, this risk premium had declined and came back to hover at about the 2% level.

The SA economy has been punished both absolutely, but also relative to other emerging markets, by international crises not of its own making. During the crises of 2008 and 2020, long-term interest rates tended to rise further than in other emerging markets, while the rand weakened markedly vs other emerging market exchange rates. From these, rapid absolute and relative recoveries have then ensued.

The RSA sovereign risk premium, 2005 to 2022

Source: Bloomberg and Investec Wealth & Investment, 8/12/2022

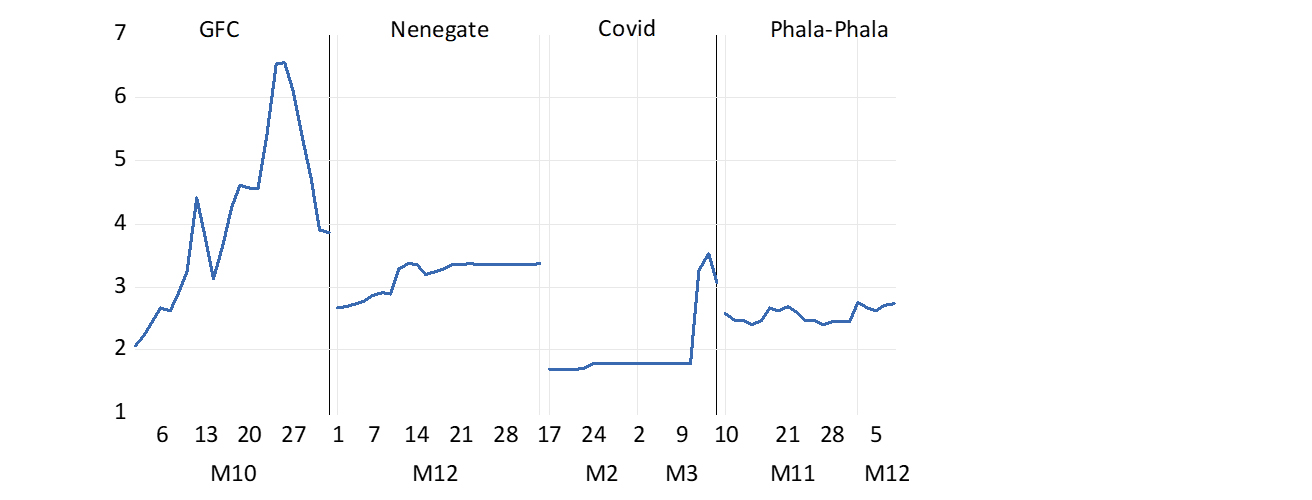

Sovereign risk spread during crises

Source: Bloomberg and Investec Wealth & Investment, 8/12/2022

RSA five-year bond yields; rand and US dollar-denominated, 2005 to 2022

Source: Bloomberg and Investec Wealth & Investment, 8/12/2022

South African risks remain elevated, as are long-term interest rates generally, and the cost of servicing our national and private debt remains a permanent danger to our solvency and growth prospects. It’s essential to address our fiscal policy issues. To this end, I was struck by these remarks that were perhaps influential:

“Finance minister Enoch Godongwana said on Friday (2 December) he expects President Cyril Ramaphosa to remain in the job but if he does quit it will not affect economic policy.….. Economic measures that will be announced in the February budget will follow on from the budget update in October.” Bloomberg, 02/12/2022

About the author

Prof. Brian Kantor

Economist

Brian Kantor is a member of Investec's Global Investment Strategy Group. He was Head of Strategy at Investec Securities SA 2001-2008 and until recently, Head of Investment Strategy at Investec Wealth & Investment South Africa. Brian is Professor Emeritus of Economics at the University of Cape Town. He holds a B.Com and a B.A. (Hons), both from UCT.

Receive Focus insights straight to your inbox

You may be interested in the following Investec products

Wealth Management

Portfolio Management

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

Wealth Management

Portfolio Management

Offshore Investments

Global diversification is a must. Investec’s offshore investments give you access to the world’s leading companies and fund managers.

PREVIOUS WEEKS' INVESTMENT INSIGHTS:

17 Nov 2022

Why the Fed needs to act to avoid recession

The market reaction to the release of US CPI data shows the extent to which the inflation dynamics have changed. Central banks should take note.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

New York on 10 November was one of those days that will be fondly remembered by those with skin in the game, in the form of investments in the equity and fixed-income markets. This was the day that the key S&P 500 index added 5.54% to its value by the close of trading and the more IT-exposed Nasdaq added even more, 7.35%. These moves were the largest on any one day since the world came to realistic terms with the damage caused to their economies by the lockdowns of 2020.

Government bonds, which typically make up 40% of any conservatively managed portfolio, also became significantly more valuable as longer-term interest rates receded sharply. The yield on the benchmark 10-year Treasury fell from 4.14% to 3.82, on the same day, the largest such daily move since 2009 (the dollar value of bonds moves higher as yields decline). On the following day, as an illustration, the JSE All Share Index had gained 3.2% by 11h15, while the rand was up 2. 7% against the US dollar by mid-morning.

The source of all the good news was unusually obvious. US inflation for October reported that day was surprisingly low. Simply put, the (new) expectation of less inflation implied less aggressive Federal Reserve policies and lower-than-previously-expected short-term interest rates. Furthermore, the higher probability of the US avoiding recession added present value to stocks and bonds. The trend to lower inflation was further confirmed later, with similarly favourable market reactions: producer prices also surprised on the downside with prices rising by a month-on-month 0.2% in October, half the rate expected by the market.

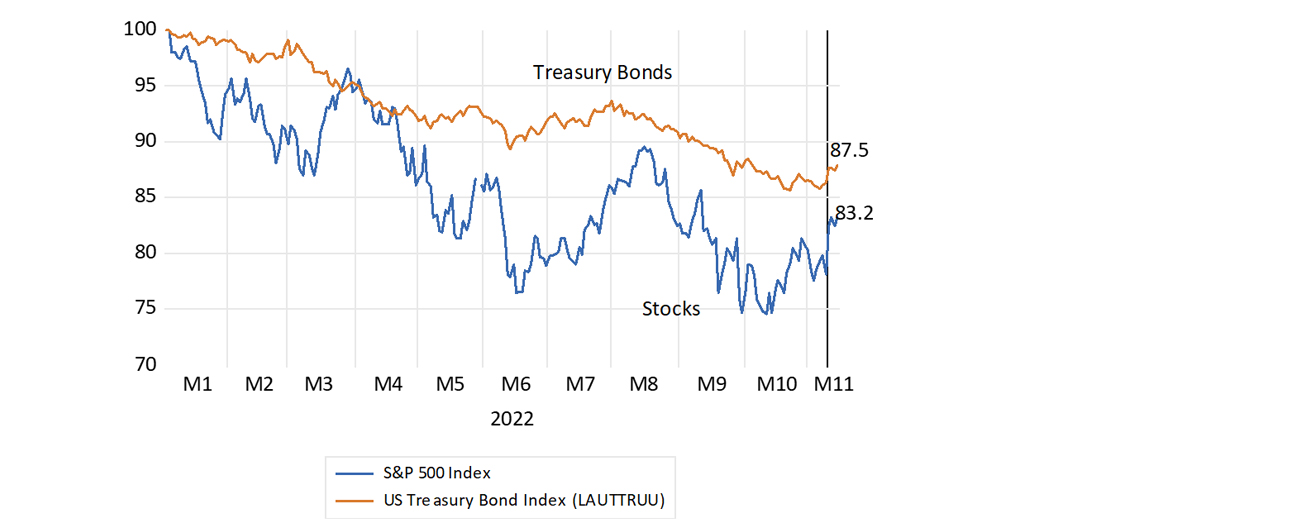

The Fed, having been so completely surprised by the surge in inflation in 2021, seems determined to march the US economy into recession to eliminate an inflation that they seemed unable to forecast with any degree of confidence. Monetary policy has become data-driven, guided by the view through the rear window. This has been accompanied by the fear that persistently high inflation could become a self-fulfilling tragedy for the US economy. The approach of the Fed seemed to be that, if a recession was the price to pay for avoiding permanently higher inflation, then recession it would have to be, much to the discomfort of the US share and bond markets. For the year to 15 November, the S&P 500 is down by 17% and the benchmark bond index is about 12% lower.

US stocks and bonds in 2022. (1 January 2022 = 100)

Source: Bloomberg and Investec Wealth & Investment, 16/11/2022

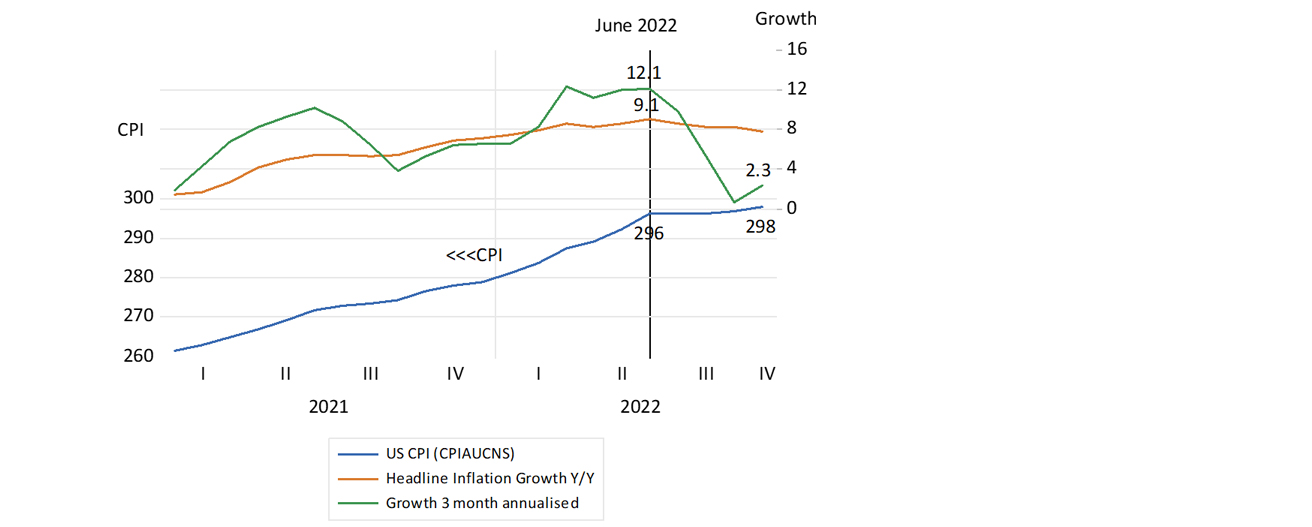

But should the Fed and the market have been so surprised? Surely not – if it had been closely following recent trends in inflation and spending by households and firms, then it would have appreciated why inflation had come to a screeching halt since its peak of 9.1% in June 2022. A year can be a very long time for an economy. The consumer price index (CPI), which was 9% higher in June 2022 than a year before, has flat-lined since June 2022. Consumer prices had stopped increasing in June and the increase over a rolling three-month period has slowed to a 2.3% annualised rate. If this trend in the CPI continues, then the inflation rate will still be a high 6.9% at year-end, but will then fall away sharply to less than 1% by June next year. US headline inflation is apparently on a path to zero.

Inflation in the US

Source: Federal Reserve Bank of St.Louis and Investec Wealth & Investment, 16/11/2022

The Fed should be acting accordingly, by recognising that aggregate spending in the US by households and firms has already slowed down markedly and does not threaten higher prices to come. The weakness of aggregate demand is restraining price increases. Higher prices to date have largely absorbed the spending power that was so boosted by vastly extra money supply and Treasury handouts provided in response to the lockdowns. Higher prices have their demand and supply side causes, but higher prices have their negative effects on spending power. Higher prices absorb disposable incomes and spending power. Higher wages – even given full employment in the US – have not fully kept up with higher prices, further restraining spending.

Inflation cannot perpetuate itself unless it’s accompanied by continuous increases in the demand for goods, which has not been the case in the US or Europe. The notion, endorsed by the Fed and many other central bankers (including the SA Reserve Bank), that higher prices and wages can simply perpetuate themselves, is a false notion. Inflation expectations soon run aground on the rock of deficient demand and unintended excess inventories. This theory of self-perpetuating inflation will not pass the test of evidence. The Fed and the market should be following the weak trends in spending closely. Ever higher interest rates could in these circumstances turn minimal growth in spending into spending declines – truly the stuff of recessions.

The Fed and the market would also be well advised to pay close attention to the trends in money supply growth. Inflation may be defined as a continuous increase in prices caused by an increase in the supply of money over the willingness to hold that extra money. All inflation is associated with excess supplies of money and the recent inflation in the US is no exception to this well-established rule.

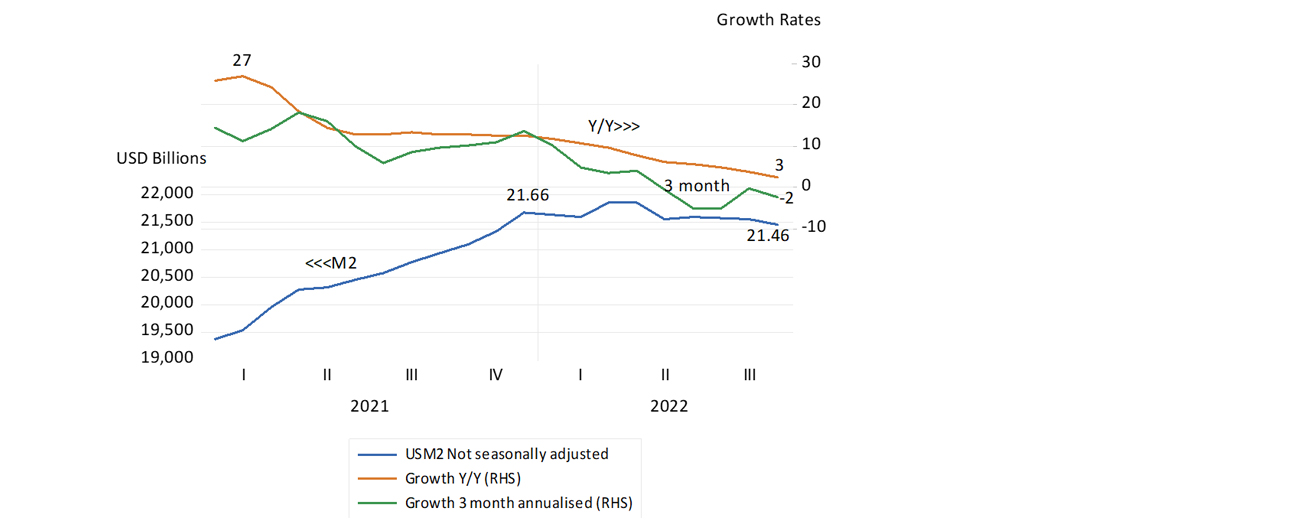

A money supply explanation of the weakness of aggregate spending in the US also helps to explain why the demand for goods and services is growing so slowly. The important monetary facts are that money supply, broadly defined as M2 in the US, is now no larger than it was at the beginning of 2022. M2 amounted to US$21.62 trillion in January. By September, M2 had declined to US$21.46 trillion. The year-on-year growth in M2 that had peaked at an extraordinary 27% in early 2021 has slowed to a barely positive 3%, with the three-month growth rates now negative. Growth in commercial bank credit has also slowed down markedly. Year-on-year growth in bank credit was 7.6% in October 2022 while growth in bank credit provided has slowed to an annualised 1.6% over the past there months. The monetary, credit and price trends are pointing strongly to deflation rather than inflation by the end of next year. The market hopes that the Fed will recognise this in good enough time and avoid recession.

Money supply in the US (M2)

Source: Federal Reserve Bank of St.Louis and Investec Wealth & Investment, 16/11/2022

07 Jul 2022

Equities, volatility and an important lesson in risk

Equity market and volatility moves over the last few months have reminded us that managing risk is as important as seeking return.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

From its record heights of January 2022, the benchmark S&P 500 Index has fallen into bear market territory, defined as down by 20% from its most recent peak. The market has not gone quietly into the night. It has lurched across the street, in a series of wide daily moves – mostly down.

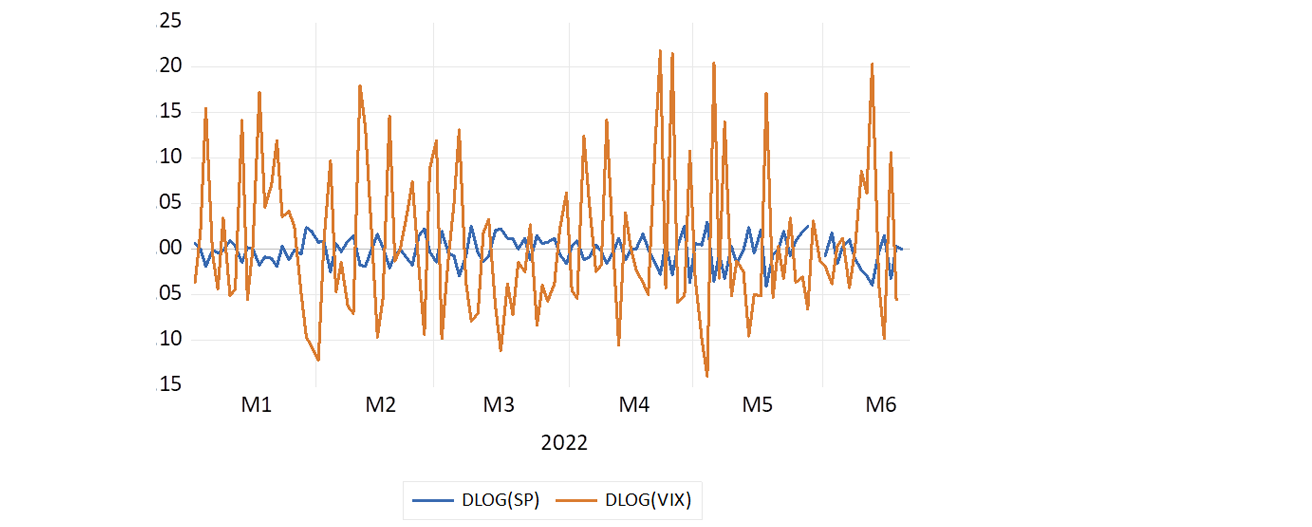

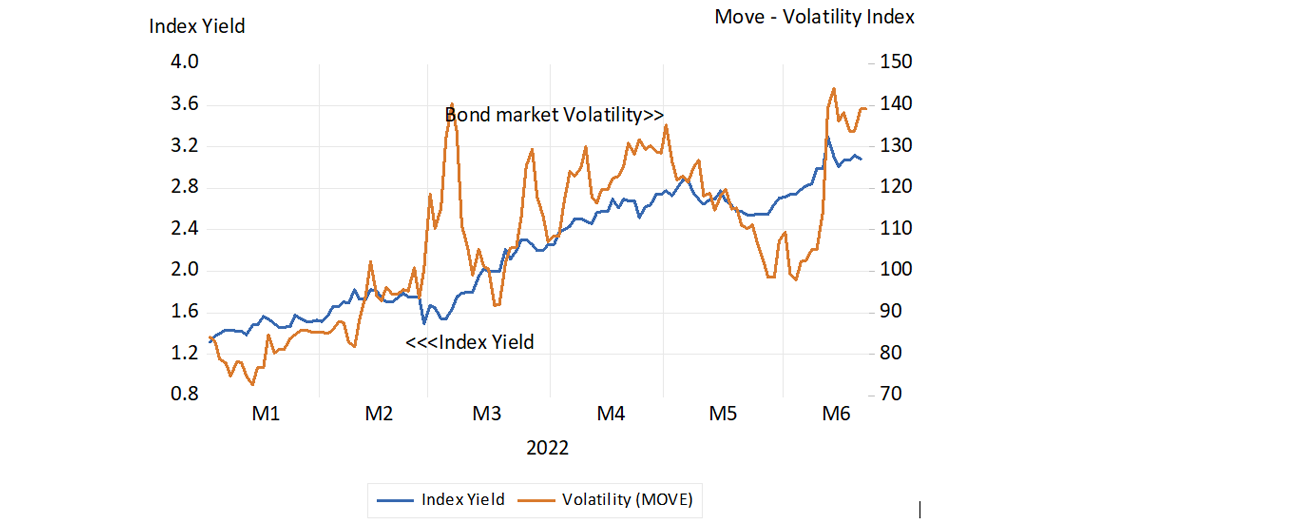

Not only has the market declined, but it has also become riskier and more volatile. The difficulty of predicting its value has raised the cost of insuring against such market risks, dramatically so. The closely followed Cboe Volatility Index, known as the VIX for short, which reflects the cost of an option to buy or sell the S&P 500 at current values, has more than doubled. From a below-average 16.6 in early January when the S&P Index stood at 4796, it reached 34 on 13 June (though it was at 36.5 in early March, soon after the Russian invasion of Ukraine), before ending the month of June at 28.7. The S&P 500 ended June at 3785 – down by 21%.

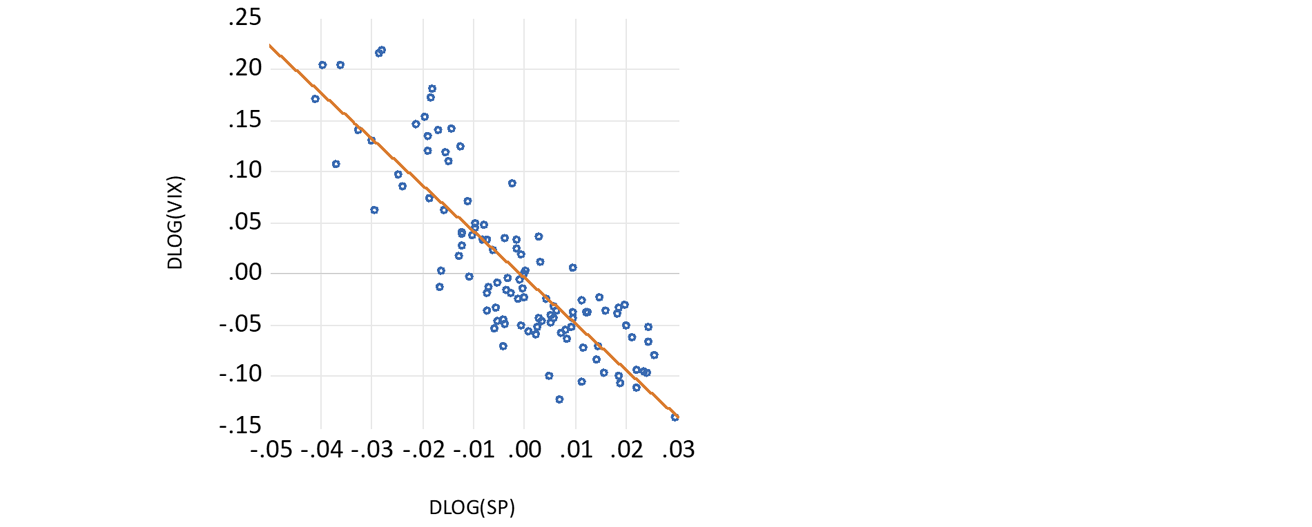

Since 2000, the average daily value of the VIX has been strongly mean-reverting, with a long-term average of 19. This is encouraging for those hoping for a return to something like a normal level of risk aversion. An increasingly risky environment has led rather than followed the share and bond markets. The negative relationship between changes in share market risk, as measured by daily moves in the VIX, and daily changes in the S&P 500 is statistically significant. The simple correlation has been close to a one-to-one (R = -0.85) in 2022. Trading the VIX or the market in 2022 will have given close to equivalent results. Taking on more risk of course demands more expected return, which is then assisted by lower market valuations. Hence, when risks rise, share and bond prices are likely to decline, so as to offer improved expected returns.

The S&P 500 and the Volatility Index (VIX) Daily percentage movements in 2022

Source: Bloomberg and Investec Wealth & Investment, 21 June 2022

The relationship between daily moves in volatility (VIX) and the S&P 500 in 2022

Source: Bloomberg and Investec Wealth & Investment, 21 June 2022

The volatility of the usually less risky market in US Treasuries has also increased dramatically and bond values have declined sharply in 2022. Long-term US bond yields have more than doubled in 2022 and bond values have declined in similar proportion. Bond market volatility is calculated off option prices on bonds in an index known as the Move Index. The Move Index has risen from 83 to 139 this year. Its long-term average is about 80.

US Treasury bond yields and volatility in 2022

Source: ICE Move Index and Investec Wealth & Investment, 21 June 2022

The origin of these highly elevated market risks is clear. It lies in the way that the Fed and other central banks seem to be going from bad (allowing too much inflation) to worse – a recession that could follow aggressive interest rate increases and a consequently overly sharp reduction in spending. This is a danger that has been intensified by the post-Covid shortages of labour in the sectors of the economy most devastated by the lockdowns, which are recovering strongly. The ‘help wanted’ signs for waiters and airport baggage handlers will not be coming down soon and the unemployment rate in the US is likely to remain very low.

A full employment recession is not in the Fed playbook. However, it perhaps should be in these unusual times that have seen extraordinary stimulus followed by inflation (that could well prove to ultimately be transitory should the right policies be adopted). The optimists in global equity markets must hope that the perceived dangers of Fed errors will decline. If they do, daily volatility will decline and share prices will trend higher.

The relationship between risk and return is easily ignored after the event because the risks assumed have often turned out to be overestimated. When returns are measured and have exceeded the returns provided by an objectively better-diversified and less risky portfolio, the fee-charging, risk-conscious investment adviser is unlikely to be appreciated. But managing risk is as important as searching for returns – you never know for certain what will happen and avoiding risk can be a valuable exercise. The risks taken to achieve the returns realised should be well recognised when evaluating investment performance – as should market risk – given that some markets are riskier than others.

11 Oct 2021

Global inflation – South Africa is not a typical case

While inflation rises across the globe, South Africa’s monetary and fiscal authorities should take note of the weak state of demand locally.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

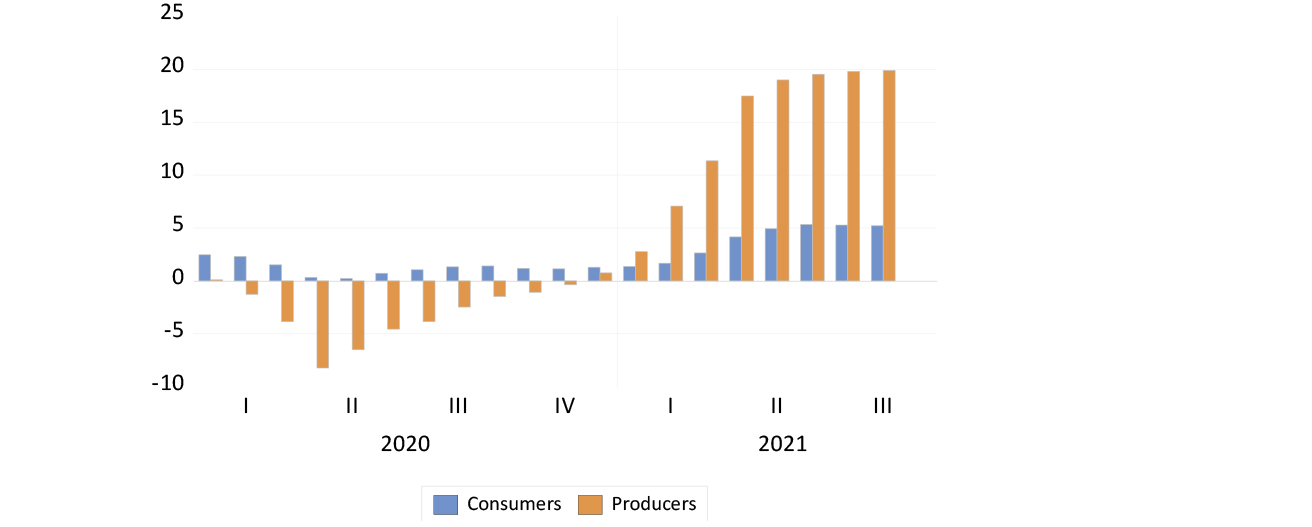

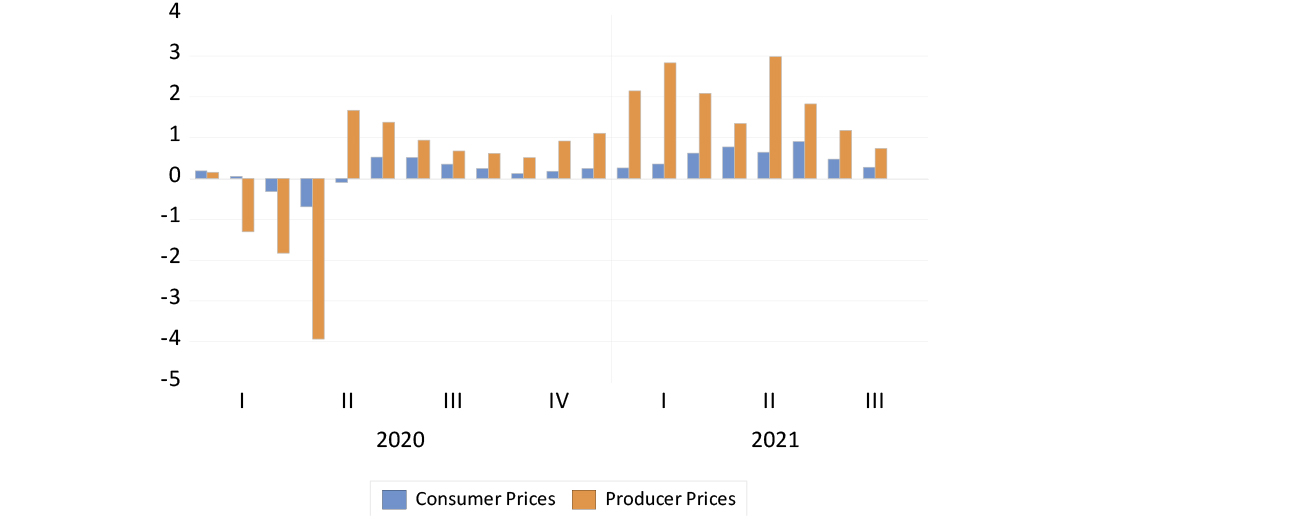

Prices are busting out all over the world. Prices charged by all US producers are 20% higher than they were a year before. Consumer prices were up by a ‘mere’ 5% in August, and that was before the recent tripling of natural gas prices.

US headline inflation rates (annual percentage growth in consumer and producer prices)

Source: Federal Reserve Bank of St Louis, Investec Wealth & Investment, 6 October 2021

US headline inflation rates (monthly percentage growth in consumer and producer prices)

Source: Federal Reserve Bank of St Louis, Investec Wealth & Investment, 6 October 2021

The cause of higher prices is clear enough. They are a response to buoyant demands stimulated by Covid-inspired extra government spending and central bank funding of much larger fiscal deficits that have dramatically increased the supply of money (bank deposits) held by households and firms. In the US, these savings have also reduced the incentive for people to get a job – of which there is an unusual abundance, as firms struggle to match surprising strength in demand with extra output and willing workers.

This mixture of strong demand with constrained supply has caused prices to rise. The effect of higher prices is also predictable. Higher prices reduce demand while they serve to encourage extra output. They also act as a drain on disposable incomes and spending power. Higher prices, particularly when they respond to supply side shocks, can therefore lead to slower growth as these higher charges work their way through the economy.

What is critical therefore for the control of longer-term inflation trends is how the monetary and fiscal authorities react to this slower growth. Should they attempt to mitigate the impact of higher prices on growth by stimulating demand for goods, services and labour, then the temporary surge in inflation can become longer lasting. Firms and trade unions will then budget for expected and uncertain inflation.

Central bankers believe that inflation depends on inflation expected, modified by the state of the economy. Independent central banks accept responsibility for the state of demand, but they hope that inflation expectations are anchored at low rates, to make their task of containing inflation an easier one. The markets, to date, have largely believed that the observed rise in inflation is a temporary one. But the markets will be watching the reactions of the fiscal and monetary authorities closely for signs of the policy errors that can turn a temporary supply side shock into enduringly higher inflation.

South Africa – not a typical case

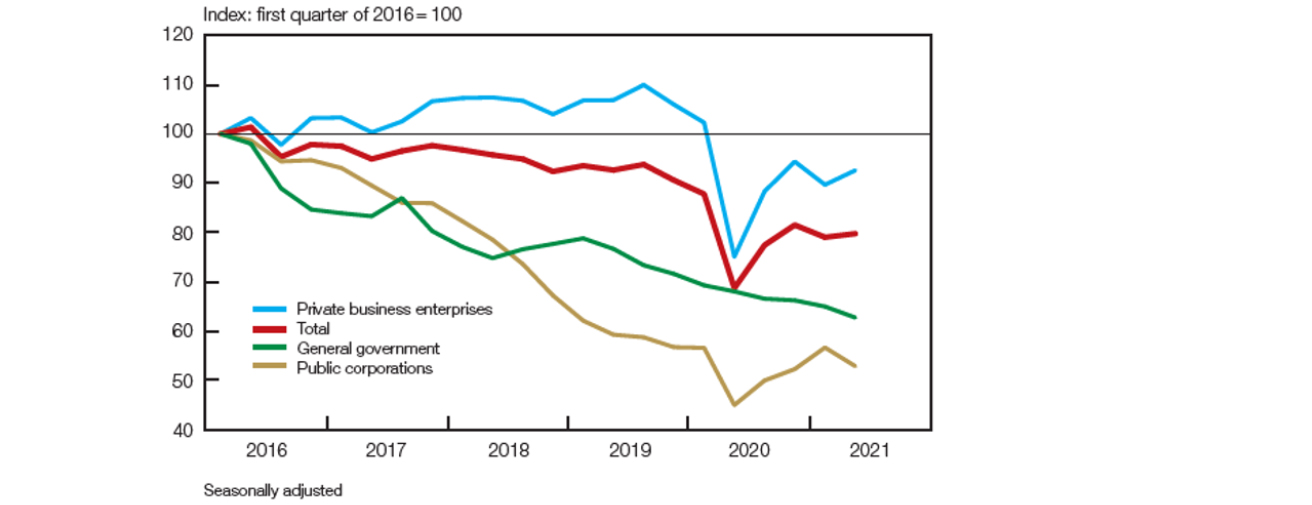

It is striking how the South African economic circumstances have not been typical. We too will have to deal with an energy price shock that will depress demand. But demand already remains depressed. Particularly depressed since 2016 have been the demands of firms, including the public corporations, for plant, equipment, workers and credit.

Real gross fixed capital formation by type of organisation

Source: Stats SA, SA Reserve Bank, 28 September 2021

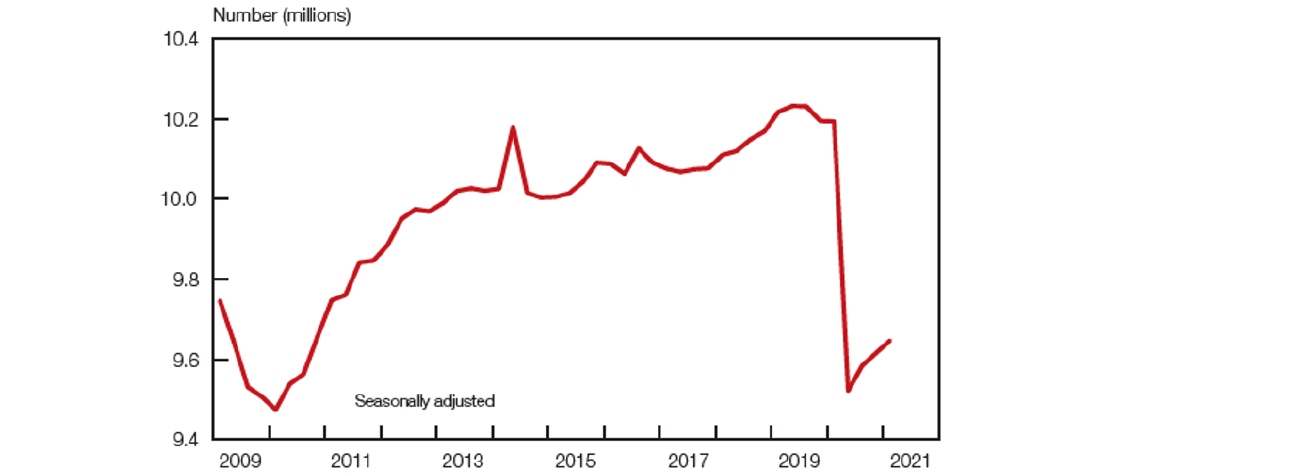

Households have helped to sustain spending, but only a little. Total spending by households grew by 1% in the first quarter of this year, but only by half as much in the second quarter. Those in jobs have earned more, yet many more (over a million) have lost their jobs since the lock downs. Formal employment outside agriculture is now below 2009 levels.

Formal non-agricultural employment

Source: Stats SA, SA Reserve Bank, 28 September 2021

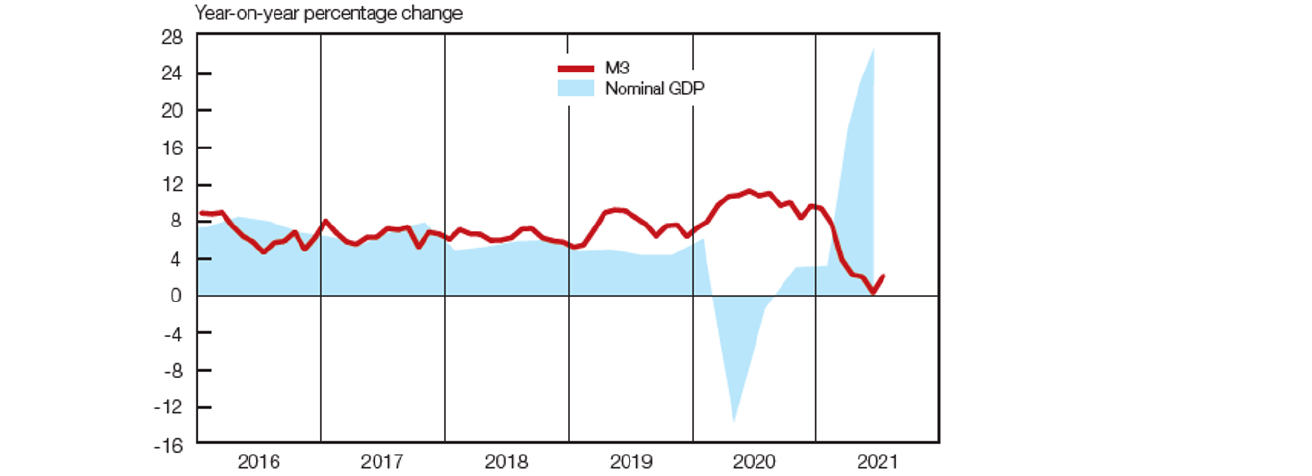

The money supply has flat lined as nominal GDP has grown strongly. The closely watched government debt-to-GDP ratio has been further reduced by extraordinary growth in government revenues. Tax receipts have accelerated in response to the global inflation of metal prices that make up the bulk of South Africa’s exports; so much so that the total borrowing requirement of the government in all its forms has declined from 13.5% of GDP in the first quarter of last year to as little as 1.8% of GDP in the second quarter of this year. Fiscal austerity has been practised in Covid-ravaged South Africa. And monetary policy, judged by its effects on money and credit supply, has not been accommodating enough.

Money supply and gross domestic product

Source: Stats SA, SA Reserve Bank, 28 September 2021

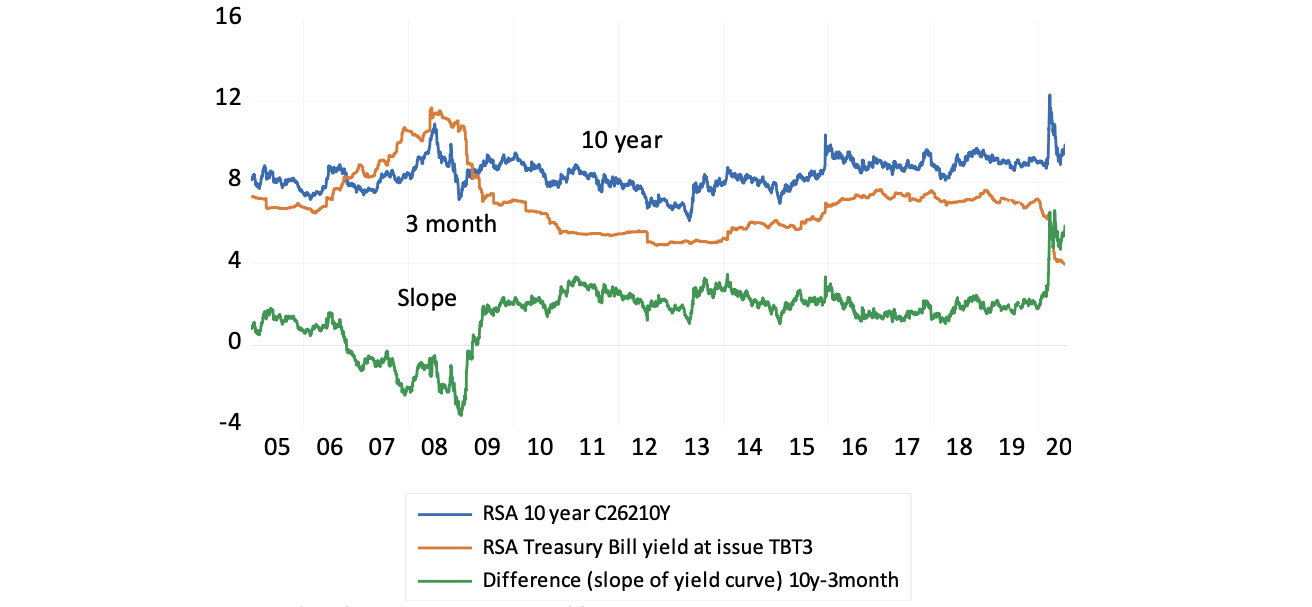

The output gap – the potential supply exceeding realised spending – is likely to remain persistently wide. Inflation expectations therefore remain unaltered. The case for higher interest rates to further depress demand seems weak in the circumstances. Yet the gap between short- and long-term interest rates has widened further in recent days. This implies an expected doubling of policy determined rates over the next three years.

The slope of the SA yield curve (SA 10-year yields minus money market rates)

Source: Bloomberg, Investec Wealth & Investment, 6 October 2021

The bond market indicates that any improvement in South Africa’s fiscal circumstances is sadly expected to be temporary rather than permanent. It can prove otherwise with fiscal discipline and sympathetic monetary policy.

8 July 2021

GDP and balance of payments: less encouraging than it appears

Encouraging capital expenditure is the key to increasing economic growth.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

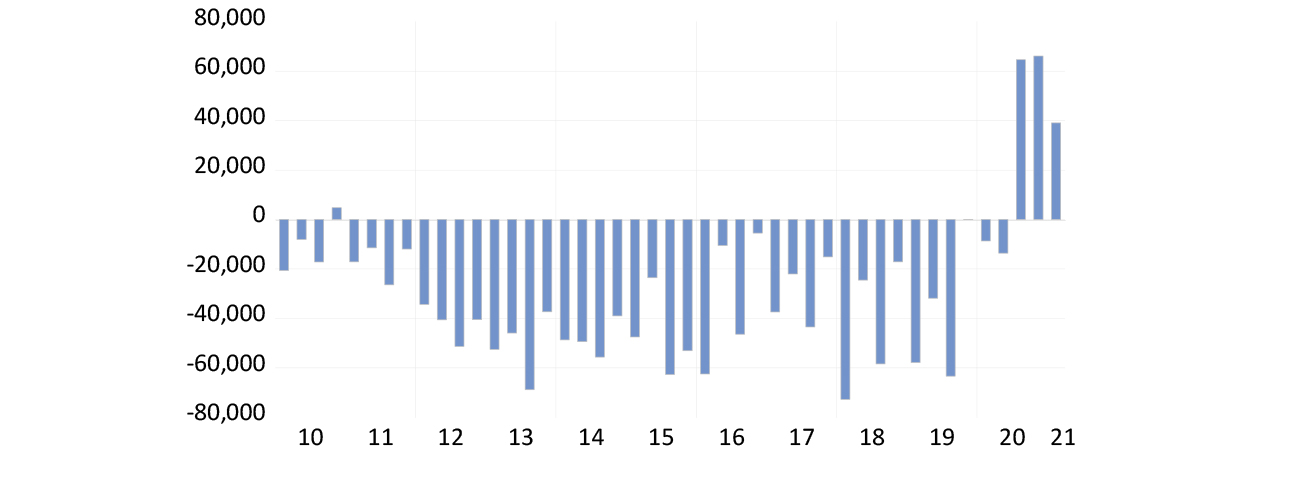

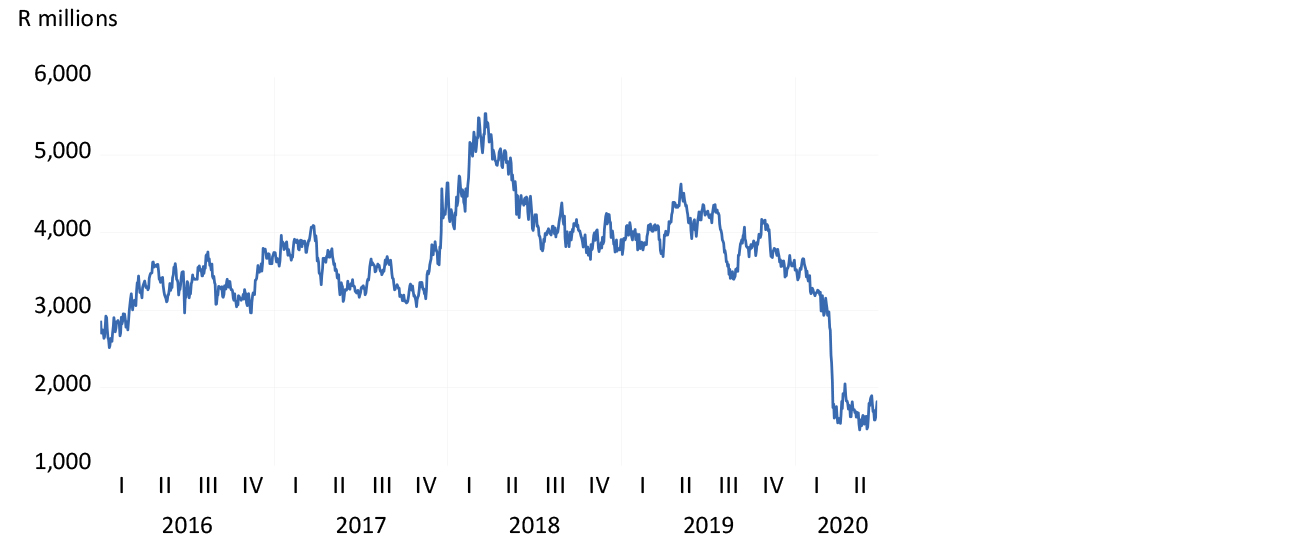

South Africans have become large contributors to the global savings pool, contributing R169.7bn (US$10.7bn) in investment abroad over the past three quarters, equivalent to an average 4.3% of GDP. Over the extended period of 2010 to 2019, SA raised an average R35.7bn or US$3.25bn of foreign capital each quarter, equivalent to -3.6% of GDP. We are now less dependent on foreign capital, with only one deficit, a fiscal deficit. However, this is not the good news story that it might appear at first to be.

Figure 1: SA’s net quarterly borrowing and lending (R millions)

Source: SA Reserve Bank and Investec Wealth & Investment, 30/06/2021

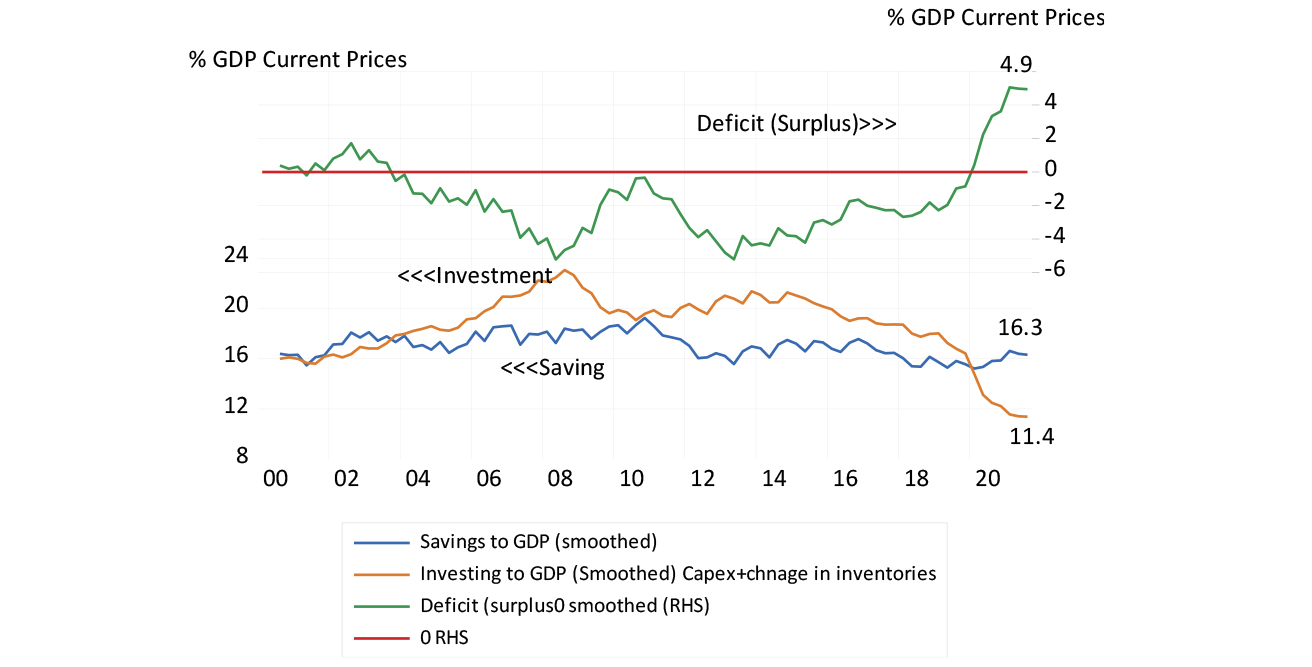

These flows abroad have come at the expense of expenditure on capital goods, which are now equivalent to only 15% of GDP. The savings rate to GDP, 17.3 % in Q1 2021, has held up much better than the investment rate. The difference between savings and capital expenditure is equal to the current account surplus on the balance of payments, which is equal to the capital outflows and now strongly positive. Since 2000, the quarterly savings rate has averaged 17% of GDP and the investment rate 18.6% of GDP, including changes in inventories and all capital expenditure. Savings are defined as the difference between gross national income and household, and government consumption expenditure.

Both the savings and investment ratios are unsatisfactorily low and not helpful for long-term growth. But it is a case of chicken and egg. If we succeeded in growing faster, by adding more vigorously to the capital stock, the government and business would have no difficulty in attracting capital from foreign and domestic sources on more attractive terms, to fund a higher rate of profitable and growth in income-inspiring investments. The constraint on growth is not a lack of savings but a lack of capital expenditure. There is no lack of global savings, only a lack of incentives to put more capital to work in SA.

Figure 2: Savings and investment to GDP ratios in SA

Source: SA Reserve Bank and Investec Wealth and Investment, 30/06/2021

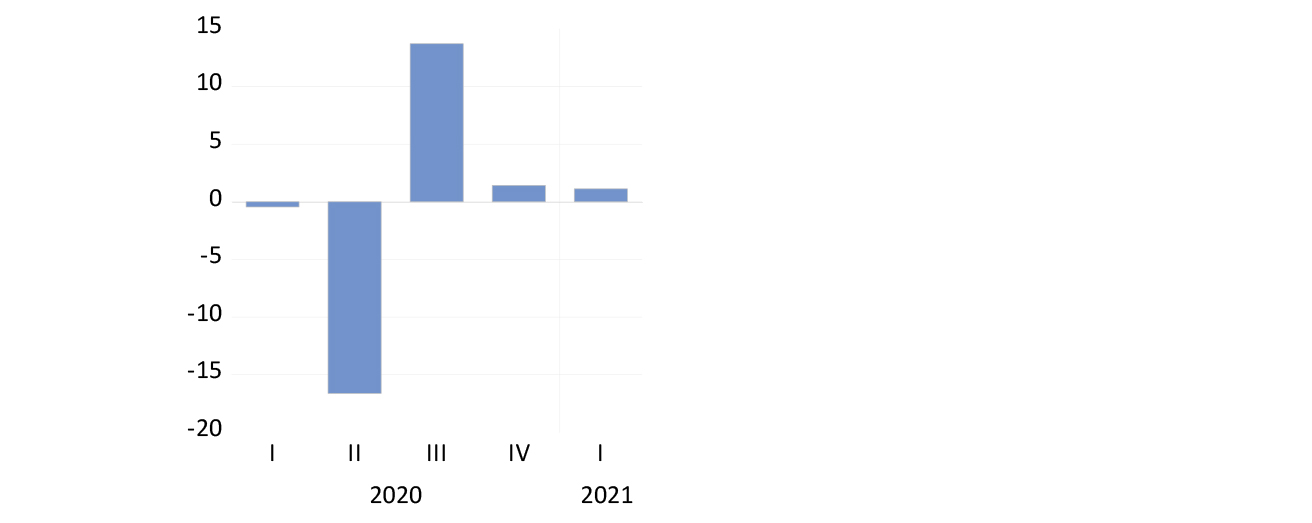

The latest economic growth news released late last month was not encouraging. The pace of the recovery of the economy has slowed down: real GDP grew by 13.7% in Q3 when recovering from the 16.6% decline registered in Q2. However, it grew by a minimal 1.43% in Q4 and has slowed further, to 1.13% in Q1 this year.

Figure 3: Growth in Real GDP (seasonally adjusted, quarter-on-quarter)

Source: SA Reserve Bank and Investec Wealth & Investment, 30/06/2021

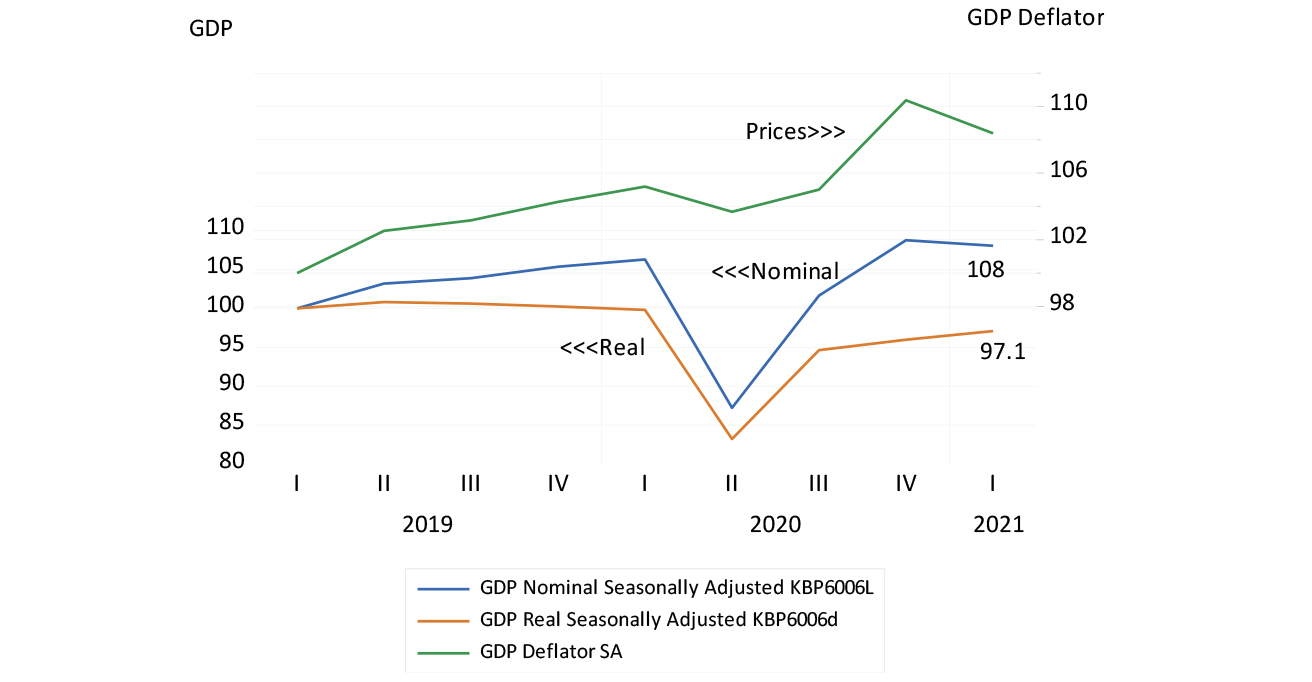

In the chart below, we compare quarterly GDP at current prices with real GDP, both seasonally adjusted and converted into an annual equivalent amount, with Q1 2019 taken to have the value of 100 as the base. Nominal GDP declined in Q1 even as real GDP grew slowly. This implies that prices as represented by the GDP deflator, calculated quarterly, fell in Q1, which is indeed the case for the prices included in the GDP number, when seasonally adjusted. Seasonal adjustments based on a long time series may not apply as normal after lockdowns.

Figure 4: GDP – nominal, real and prices (2019 = 100)

Source: SA Reserve Bank and Investec Wealth & Investment, 30/06/2021

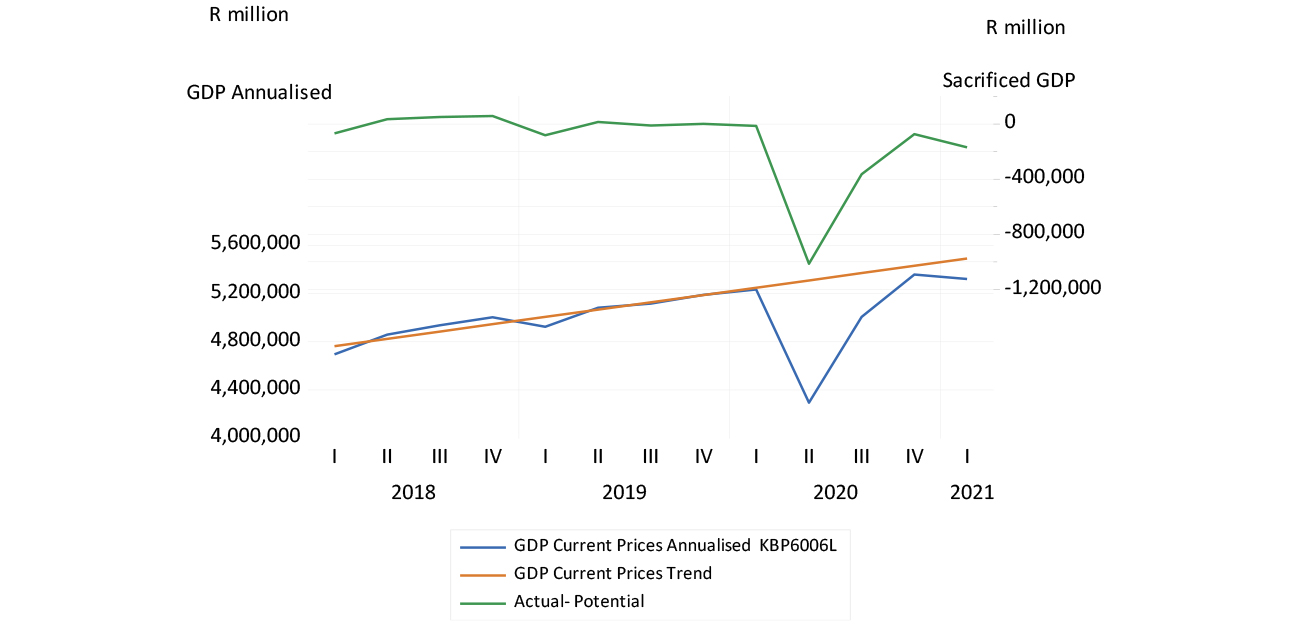

The slower growth has widened the gap between what the economy might have produced without the lockdowns, and what has been produced. And the latest lockdown will have added to the enormous sacrifices of income made so far. The losses of output and incomes – the difference between actual and pre-covid potential output – could be the equivalent of 25% or more of the potential GDP in 2021, or R1 trillion in money of the day.

Figure 5: Annualised growth in nominal GDP – potential and actual growth (annualised)

Source: SA Reserve Bank and Investec Wealth & Investment, 30/06/2021

M3 money supply (bank deposits) was up by a mere 1.26% in May 2021 on the year before and bank credit supplied to the private sector has declined by 0.42% year-on-year. This has been a strong headwind for the economy. The economy cannot realise anything but tepid growth in such monetary circumstances. Yet interest rates are currently expected to add to the strength of these head winds. Money market rates are expected to increase by over one percentage point over the next six months, and the term structure of interest rates indicates that the interest rate on a one-year loan to the government will nearly double over the next three years, from 4.64% to 8.2%.

The Reserve Bank, on the occasion of its centenary, appealed to the government to lower its debt-service costs, by doing the right things, a sentiment we fully share. Without lower long-term interest rates, other government spending is sacrificed to pay the interest bill, as the Bank warns. But more importantly, the incentive to add to the capital stock will remain as restricted as it is, given high long-term interest rates. An average SA firm contemplating adding to its plant and equipment is required to return about a demanding 9% real return on its capex. That is a return at least equal to the government bond yield of 10% plus 5% for equity risk, less inflation expected of 6%. This real cost of capital needs to come down if we are to grow faster.

The Reserve Bank would do well to reflect on what it might do now to promote the growth necessary to reduce SA risks and long-term interest rates. The answer, we argue, is that the Bank should not allow short-term rates to rise and do what they can do to increase the supply of money and credit, without which growth in spending and output cannot materialise.

24 June 2021

A monetary tale of two economies

SA’s monetary authorities could learn something from their US counterparts when it comes to dealing with the destruction of incomes caused by the pandemic.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

The steps taken in the US to counter the destruction of incomes and output caused by the lockdowns of economic activity can be regarded as a resounding success. Real US output is now ahead of pre-covid levels. By the end of 2021, GDP could well surpass the GDP that might have been expected absent the lock downs. It took a great deal of income relief in the form of cheques in the post from Uncle Sam, supplemented by generous unemployment benefits and relief for businesses.

The extra income means an increase in deposits, in other words money placed with the US banks, to be spent later or exchanged for other financial assets.

Deposits held by banks with the Federal Reserve System have increased by 85%, and deposits at the commercial banks have grown by 26% since March 2020. The source of the extra cash, the deposits at the commercial banks and the Fed, has been additional purchases of government bonds and mortgage-backed securities in the debt markets from the banks and their clients, which are being maintained at the rate of US$120bn a month.

The assets and the liabilities of the Fed have increased by 36% over that period. This is money creation on an awe-inspiring scale and it has worked, as intended, to promote demand for goods and services. Providers of goods and services are struggling to keep up with demand, while also struggling to add to payrolls, leading to upward pressure on prices. The US CPI was up by 5% in May – a rate of inflation not seen since 2008 and before then only in the 1990s.

Inflation in the US – annual percentage changes in CPI

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment, 15/06/2021

However, the outlook for inflation in the US is less obvious than usual. The Fed has been surprised by the pick-up in the inflation rate, as was indicated by the Federal Open Market Committee and Fed chief Jerome Powell’s press conference on 16 June. Powell remains confident that the increase in inflation is transitory and the Fed does not intend raising interest rates any time soon, at least not until the economy has returned to full employment, which is judged to be some way off.

(It should be noted that full employment may mean a lower number than previously estimated, given that two million potential workers have withdrawn from the labour market since the lockdowns. They may however wish to return to employment should the opportunities to do so present themselves; this is one of the uncertainties the Fed is trying to deal with as it looks to understand the post-Covid world.)

A number of Fed officials however have brought forward the time when they think the Fed will first raise its key interest rates, to the first quarter of 2023, a revision that surprised the market and moved long-term interest rates higher. The bond market nonetheless remains of the view that inflation in the US over the next 10 years will remain no higher than the 2% average rate targeted by the Fed. The Fed will be alert to the prospect that more inflation than this will arise.

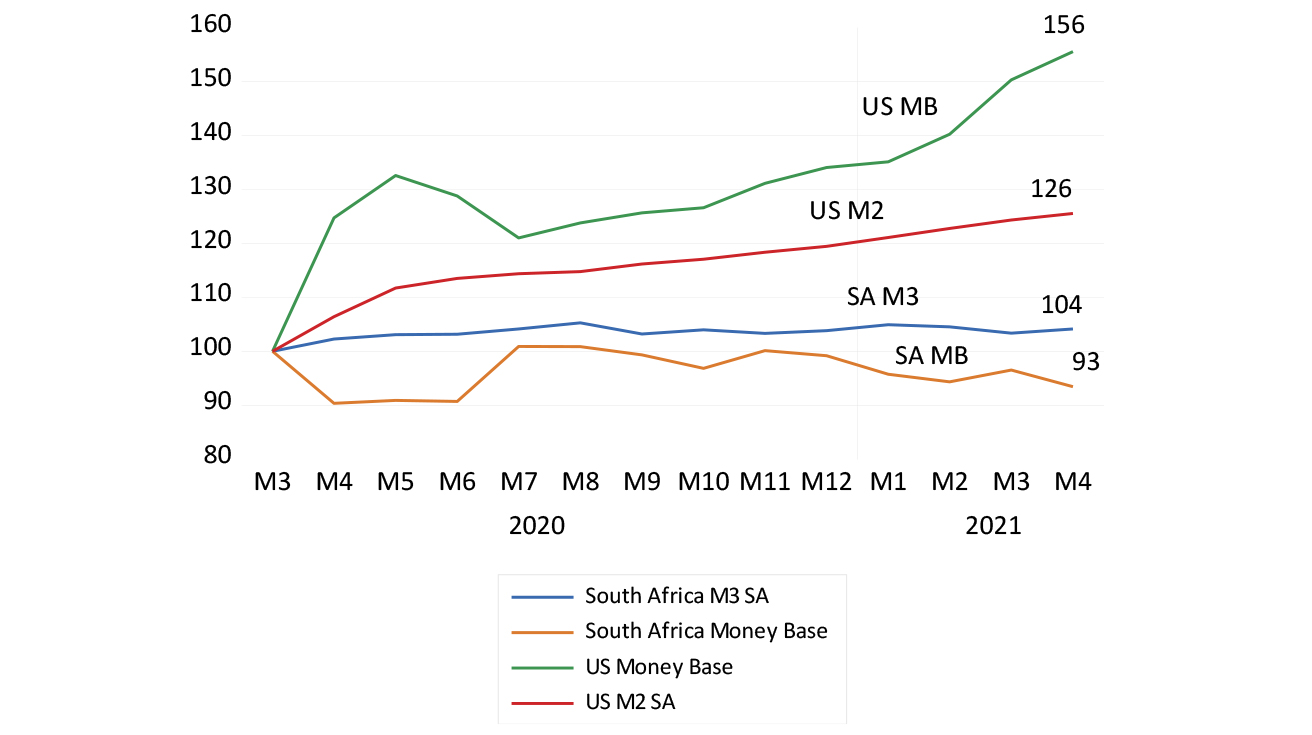

A tale of two central banks

The contrast of the actions of the Fed with those of the South African Reserve Bank (SARB) is striking. The SARB balance sheet contracted by R115bn, 10.8%, between March 2020 and May 2021. Since January 2020, the sum of notes issued plus deposits of the banks with the SARB (the money base) has declined by 6%, the supply of bank deposits (M3) has grown by a paltry 4% and bank credit by 2%. These are shocking figures for an economy struggling to escape a deep recession.

The SARB may be of the view that money and credit are less important for the economy, and that changes in interest rates are the only instrument they have to influence the economy.

Monetary comparisons between SA and the US (March 2020 = 100)

Source: SA Reserve Bank, Federal Reserve Bank of St Louis and Investec Wealth & Investment, 15/06/2021

The SARB seems to believe their lower interest rate settings have been accommodative and helpful to the economy. Higher interest rates would, of course, have been unhelpful and lower rates were certainly called for. However, the money and credit numbers indicate deeply depressing influences on the economy, influences that the SARB could and should have done much more to relieve, following the US example. There is more to monetary policy and its influence on the economy than movements in interest rates.

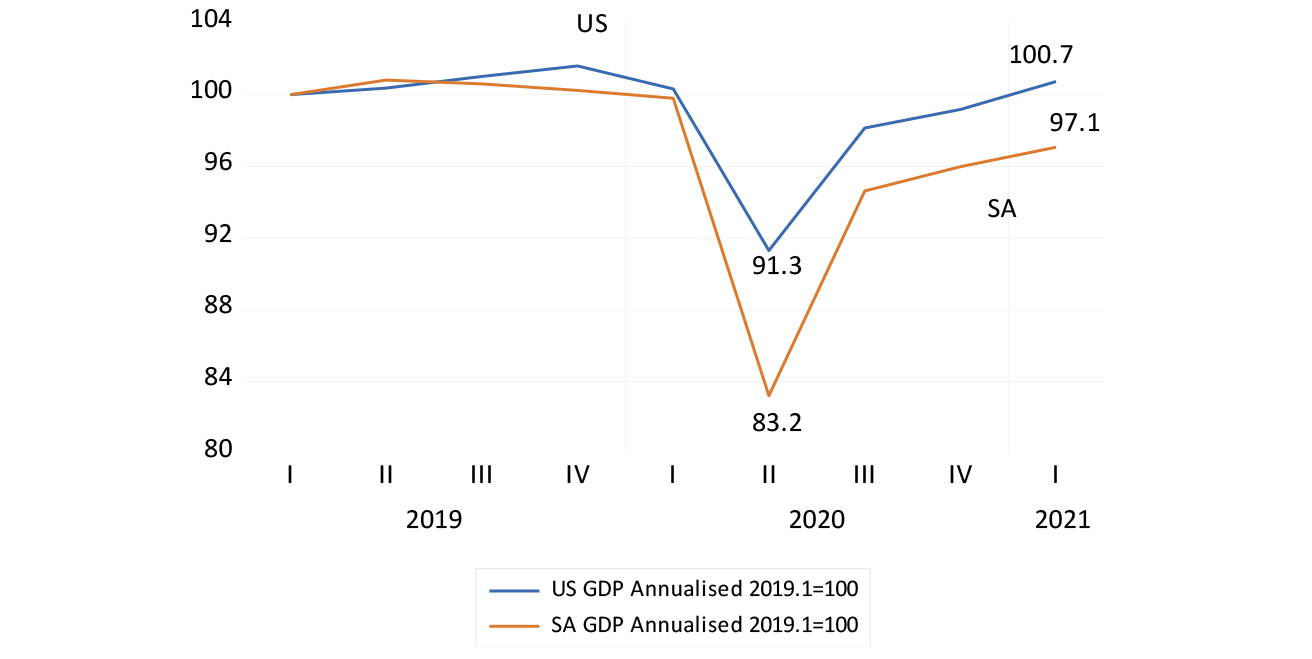

GDP in the US and SA (March 2000 = 100)

Source: SA Reserve Bank, Federal Reserve Bank of St Louis and Investec Wealth & Investment, 15/06/2021

It would be easy to despair of the prospects for the SA economy given the current, discouraging trends in the supply of money and credit. However, we can draw hope from the possibility that the US cavalry (with some Chinese assistance) will rescue us, in the form of rising prices for metals and minerals that are very much part of the inflation process currently under way in the US.

Metal prices have always led the SA business cycle, in both directions. They may well lead us out of the current morass, after which the supply of money and credit will then pick up momentum to reinforce the recovery, as they have always done in a pro-cyclical way. The responses to the lockdowns have made it clear how our monetary policy reacts to the real economy. A favourable wind from offshore may lift the money supply and bank credit, without which faster growth is not possible.

13 April 2021

Why property rights matter

Property rights underpin wealth creation and are essential for attracting investment and helping communities to escape deprivation.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

I once asked a meeting of law students if they knew why we have laws to protect our wealth and enforce the sanctity of contracts. They appeared to have little idea why, other than that it was morally wrong to steal, to perpetuate a fraud or not to be true to your word. Nobody had told them that protecting the rights to wealth was essential if wealth was to be created in the first instance.

If you saved and invested in a home, farm, mine or business enterprise, and somebody, stronger than you, could simply take it away, there would be no reason to save and invest in productive, long-lasting assets. Protection of wealth to encourage wealth creation is essential if any community is to become more productive and escape deprivation.

The power of a government to take what might be yours, gained fairly in exchange, is one of the obvious dangers to be averted in the public interest of increasing saving and capital expenditure. While there might be good cause for a compulsory purchase to advance a broad public interest, it should be facilitated by offering the market value of the asset as compensation. No compulsory expropriation without compensation is enshrined in our Constitution and legal practice, for good, income-enhancing reasons.

Having to offer full compensation to any owner is something of a deterrent to exercising any compulsory purchase order. The taxpayer, who also has political influence, will have to pay up for the assets. It’s an influence that is resented by those who have ambitions to change the world for what they believe will be the better and are frustrated by the lack of the means to do so. Just pay for what you wish to take, is the principle we should defend and honour.

South Africans are not just reluctant taxpayers. We are reluctant savers and maintain an unsatisfactory rate of capital accumulation. We still have to rely on foreign savings on a significant scale. We are dependent on capital that can be freely invested anywhere and is easily frightened off by threats to its being taken away by expropriation, or by changes in regulations affecting its market value.

The mere hint of expropriation of land and real estate, without compensation, makes foreign capital more expensive. Foreign investors command high expected returns to compensate for the risk of our taking it away or interfering with it. Hence our low rate of capital formation. An on-average risky JSE-listed company, to justify any addition to its plant and equipment, would have to offer a return of over 15% a year, or about at least a real 9% after expected inflation of about 6%. These are returns that few companies can confidently budget for.

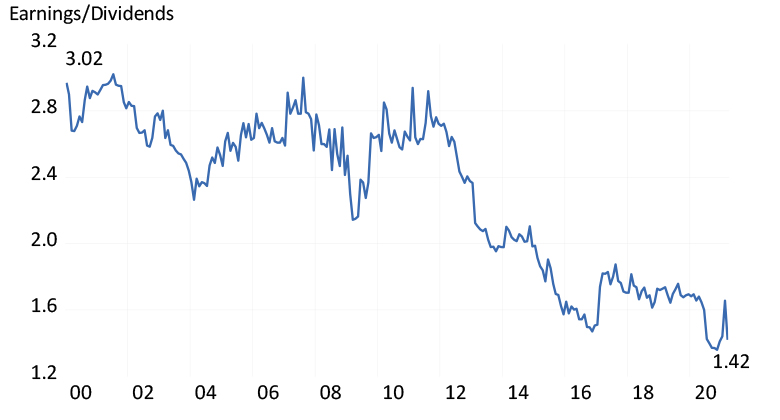

Hence businesses are investing less, and saving less, by paying out more of their earnings in dividends. The ratio of JSE earnings to dividends has halved since 2010. They are retaining less because they are investing less in capex, for understandable reasons.

Figure 1: Ratio of JSE All Share Index earnings per share to dividends per share

Source: Iress and Investec Wealth & Investment, 12/04/2021

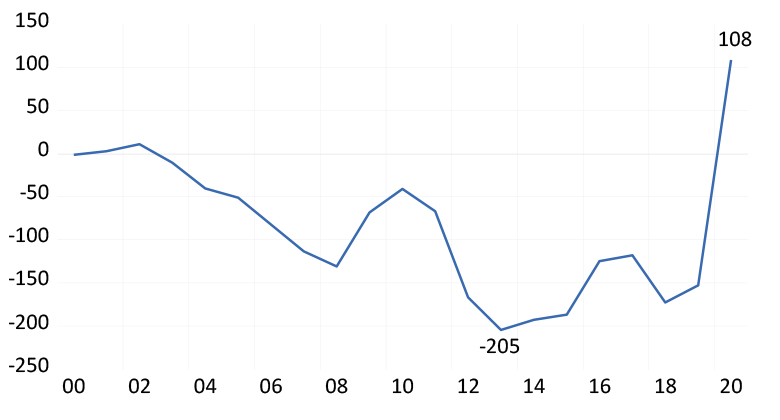

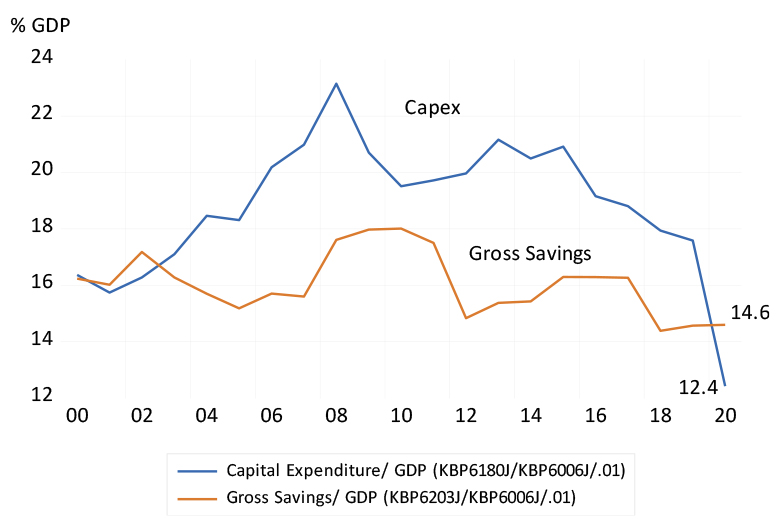

It has taken Covid-19 to bring the low rate at which South Africa saves above the dismal rate at which we are currently adding to plant and equipment, adding capital at the rate only of 12% of GDP in 2020. Accordingly, we have become a net lender to the world.

Reducing the risks of investing in SA will encourage more capital expenditure and savings in the form of earnings retained by business. We could then attract the necessary foreign capital at a lower cost than we are paying now. Reducing risks means sensibly reducing the threat of taking, not adding to it.

Figure 2: South African annual net foreign borrowing (-) or lending (+), 2000-2020 (R billion)

Source: SA Reserve Bank and Investec Wealth & Investment, 12/04/2021

Figure 3: South African ratio of annual capital expenditure and gross savings to GDP, 2000-2020

Source: SA Reserve Bank and Investec Wealth & Investment, 12/04/2021

29 March 2021

Inflation expectations will determine the success of the US stimulus package

Thanks largely to low interest rates, the US’s stimulus package is fiscally manageable. Fiscal restraint will be required however, to ensure it remains so.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

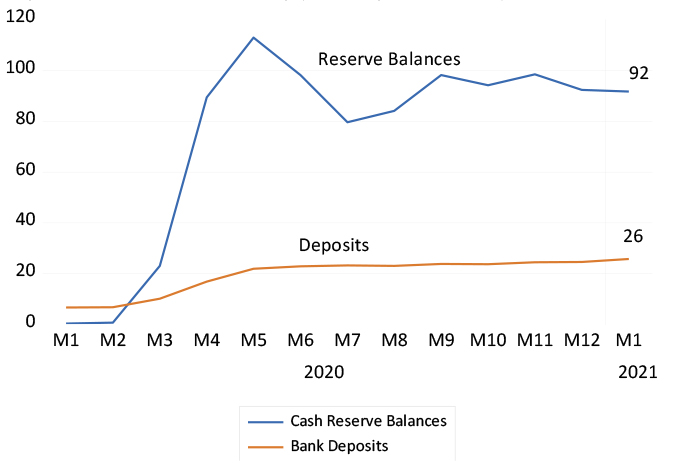

The US not only has old-fashioned cheques (checks), but checks in the post (mail) nogal. No fewer than 90 million cheques worth $1,400 each have been mailed so far to Americans earning less than $400,000, with more to come. The dollars will find their way out of the Federal Reserve Bank (Fed) into individual banking accounts, or cashed in, which will add to both bank deposits and the cash reserves of the banks with the Fed. Deposits with US banks are up by 26% since January 2020 and the cash reserves of US banks are up by 92%. Both represent huge firepower for additional spending on goods and services, and bank lending over the next year.

US growth in cash reserves of the banking system and growth in bank deposits

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment

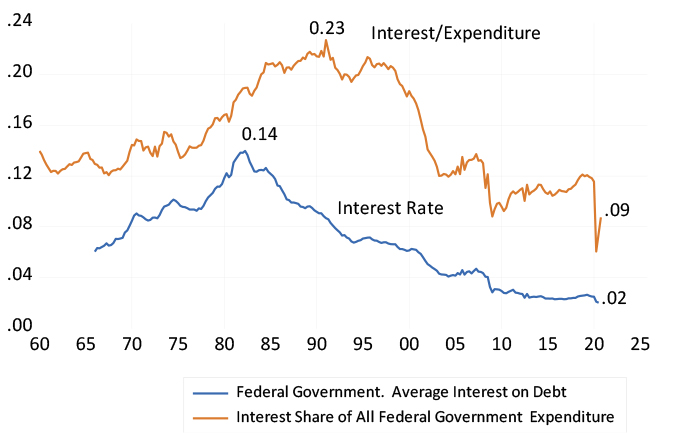

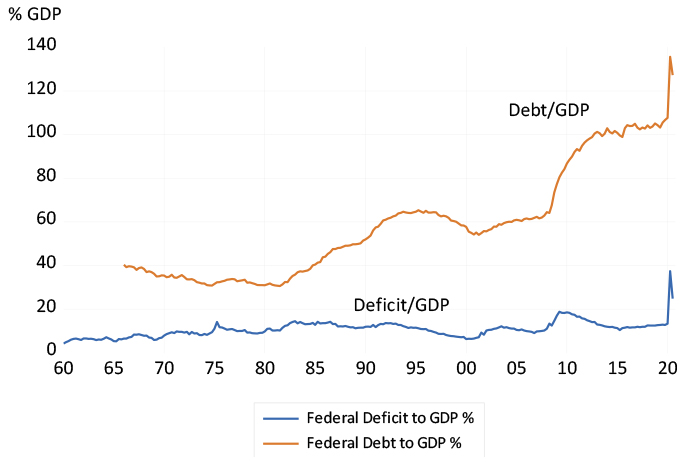

The debt-to-GDP ratio will rise to over 130% and the fiscal deficit will soon approach 30% of current GDP. But interest rates remain exceptionally low – the average interest paid on all US debt is only 2% a year and interest payments account for 9% of all federal spending. In 1990, interest payments accounted for 23% of the federal budget at an average interest rate on the debt of about 10%. In short, these are now comfortable fiscal conditions. These ratios improved appreciably in the 1990s, thanks to lower deficits. The borrowing requirements of governments can and indeed have to be restrained by some mixture of spending less and taxing more – both hard to do. Another $3 trillion of US government spending on so-called infrastructure is coming down the pike. There will be no fiscal crisis for the US on the horizon, if US borrowing costs remain low. But can they?

Average interest paid on US debt and Interest paid as a percentage of all Federal government spending

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment

It will depend on how much inflation is expected over the next 10 years. The higher the expectation of inflation, the higher the cost of raising government debt will be. Interest rates rise with higher inflation expectations in an almost lockstep way. The expected annual inflation rate over the next 10 years in the bond market is of the order of an unthreatening 2.2%. The higher the cost of borrowing, the more likely governments may resort to printing more money to fund their spending, which in turn will reinforce spending and increase the rate of inflation (and raise expectations of inflation).

All will depend on the scale of US borrowing expected over the next 10 years. It will have to slow down to something like normal to prevent the US Budget from being overwhelmed by higher interest rates. Janet Yellen, the Treasury Secretary, told Congress that taxes will have to rise to pay for the extra $3 trillion. Will they, or will the unpopular prospect of higher taxes restrain spending ambition? It will take more than taxing the rich to pay the piper.

US ratio of Federal government debt and fiscal deficits to GDP

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment

US Federal government deficits

Source: Federal Reserve Bank of St Louis and Investec Wealth & Investment

Fed Chairman Jerome Powell is relaxed about inflation for now and he remains determined to help the US economy get back to full employment. He is waiting to see what will happen and he believes he has the tools to dial inflation back should it rise temporarily – as is widely expected.

So what are these tools? Mainly, it is the power to control short-term interest rates by adding or taking away dollars from the system. He does not however control how much the government spends, how much it taxes and how much it will have to borrow. The higher he sets short-term interest rates, of course, the less popular he will become. His political independence should not be taken as a permanent given.

Powell is confident that inflation is well anchored around the current 2% annual rate, the Fed target for inflation. Actual inflation however depends on expected inflation and on the difference between actual GDP and potential GDP – the output gap. Powell believes the Fed has this gap under control. But without active co-operation from fiscal policy to restrain government spending over the long run, this inflation anchor could easily slip away. As with the Fed, we will wait and watch.

11 March 2021

National Treasury’s tax epiphany

There is more to tax than what appears on the surface – ask National Treasury and South African homeowners.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

National Treasury has had an epiphany. It has acknowledged that higher taxes can lead to slower growth and that lower taxes can lead to faster growth. Hence the decision to forgo R40bn of planned income tax increases and to propose a reduction in the corporate tax rate to 27%. All in the interests of faster growth. Hallelujah.

The Budget Review recognises that taxes have complicated feedback effects. It recognises that the burden of higher corporate taxes ends up being passed on to consumers of goods and services, in the form of higher prices and lower incomes for those who provide labour and other services to the corporation. The supply of capital to the SA enterprise and hence the supply of goods, services and the demand for labour and land, is determined by the required after-tax returns of investors. Higher taxes will reduce expected returns and so the supply of capital, goods, services and the demand for labour. The supply of capital for SA is sourced globally and the required returns are determined in the global market, as the Review recognises.

The Review could have added that personal income tax rates have supply side effects. It is the after-tax benefits provided to taxpayers by governments that establish the standard of living, which in turn determines the willingness to supply labour to an economy. The more internationally mobile the providers of labour services are, the more of a global market South African firms have to compete in for the supply of indispensable skills. Raising income tax rates at the margin drives the emigration of human capital and leads to higher prices to cover higher after-tax costs of inputs. Lower taxes could help do the opposite, that is increase supply of capital and skills. Faster growth becomes possible with a lower tax burden.

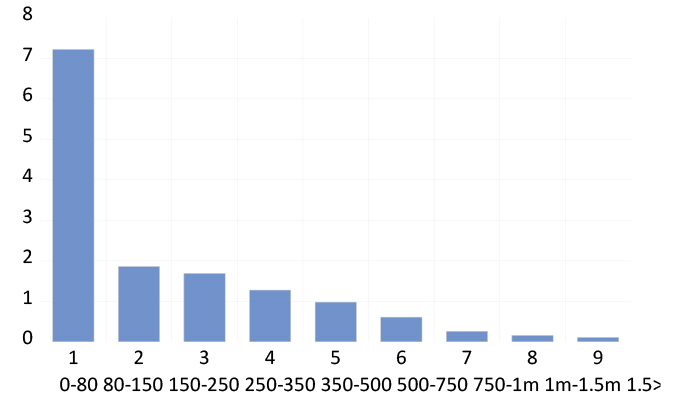

The share of income of those who will report taxable income of more than R1.5m in 2021-02 (a mere 113,192 taxpayers) are in the highest of nine tax brackets. They report 12% of all income and will pay over 26% of all personal income tax. Only when annual incomes are above R500,000 does the share of income taxes paid exceed the share of incomes earned. The numbers of high earners and taxpayers in SA have been stagnating. We need more of them to help grow the economy and provide for the relief of poverty.

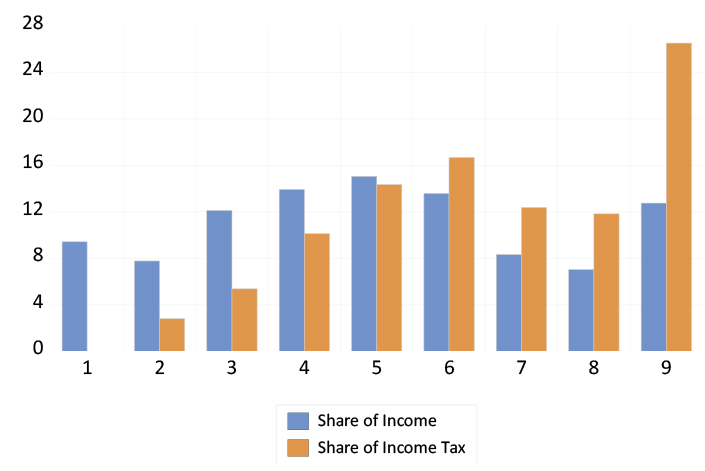

It is the mix of taxes and the benefits supplied by governments that determines the standard of living and that drives the migration of labour and capital. The burden of income taxes in South Africa is highly progressive, as are the benefits of government spending. Higher income earners in South African pay much of the personal income tax and draw very little on government benefits provided.

Figure 1: Population by the nine income tax brackets (millions)

Source: Budget Review 2021-2020, Chapter 4 Table 4.5, Investec Wealth & Investment, 24/02/2021

Figure 2: Share of income and income tax paid of the nine income tax brackets (percent)

Source: Budget Review 2021-2020, Chapter 4 Table 4.5, Investec Wealth & Investment, 24/02/2021

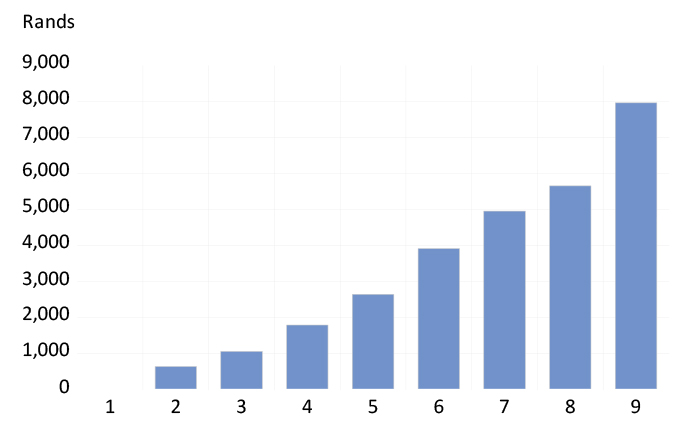

Figure 3: Average income tax saved (rand per annum) per member of each tax bracket (total income tax saving = R51bn)

Source: Budget Review 2021-2020, Chapter 4 Table 4.5, Investec Wealth & Investment, 24/02/2021

For evidence of the relationship between taxes paid and benefits provided by government, one need only compare residential property prices in Cape Town with those in the other cities and towns. They can watch the business television channels, to be aware that magnificent homes in Johannesburg or Durban can be had for the price of a small two-bedroomed apartment in Cape Town. This is because of the more favourable mix of higher property taxes (not necessarily higher wealth tax rates) that are paid in return for comparatively good services provided by the local government.

Homeowners should be aware that higher taxes can more than pay for themselves when there is good government. And higher taxes will destroy their wealth when the service is inadequate for the taxes paid.

11 February 2021

What higher global inflation could mean for South Africa

Higher commodity prices could bring about higher global inflation. That would not necessarily be bad news for South Africa.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

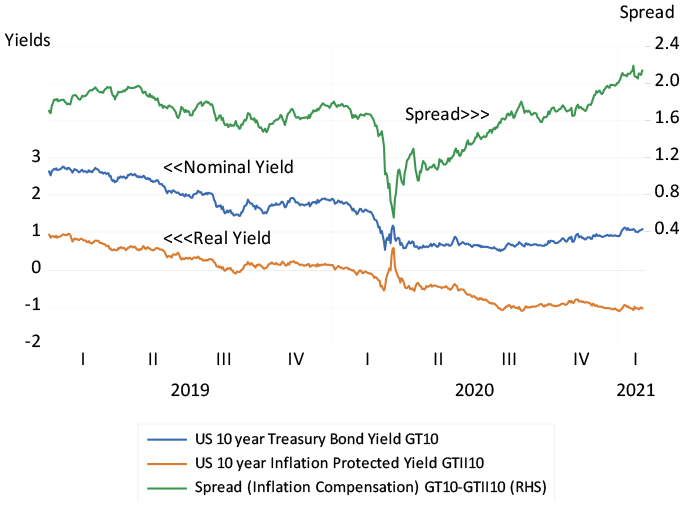

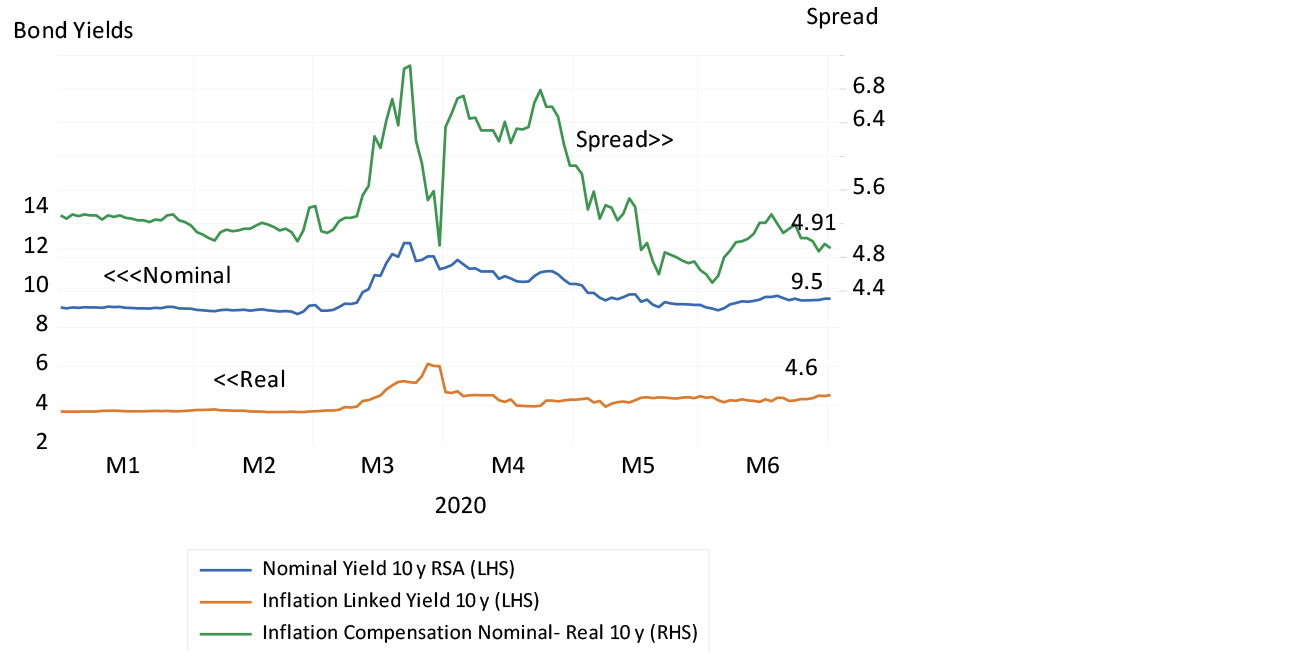

There is a hint of inflation in the frigid northern air. It’s being reflected in the long-end of the bond markets, the part of the yield curve that is vulnerable to signals of high inflation and the higher interest rates and lower bond values that follow. The compensation offered for bearing the risk that inflation may surprise on the upside is reflected in the spread between nominal and inflation-linked bond yields. These spreads have been widening in the US, and in low inflation countries like Germany and Japan.

This spread for 10-year bonds in the US was as little as 0.80% at the height of the Covid-19 crisis, was 1.63% at the end of September, and at the time of writing is at 2.14%. It has averaged 1.97% since 2010. The spread has widened because investors have forced the real yield lower, to -1.03%, further than they have pushed the nominal yield higher now, to 1.15%. This is still well below the post 2010 daily average of 2.25% (see figure below).

US 10-year nominal and inflation-protected bond yields

Source: Bloomberg and Investec Wealth & Investment, 11 February 2021

Investors are paying up to insure themselves against higher inflation by buying inflation linkers and forcing real yields ever more negative. Clearly, the nominal yields continue to be repressed by Fed Bond buying (currently at a $120 billion monthly rate). One might think it’s easier to fight the Fed with inflation linkers, than via higher long bond yields, to which the currently low mortgage rates and a buoyant housing market are linked.

The Fed is insistent that it is not even thinking yet of tapering its bond purchases. The Treasury, now led by Janet Yellen, previously in charge of the Fed, insists that a new stimulus package of US$1.9 trillion is still needed for a US recovery.

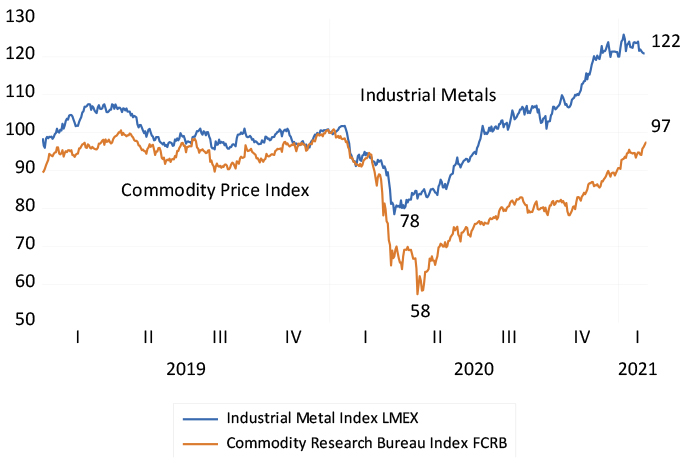

Metal and commodity prices, grains and oil are all rising sharply off depressed levels. Industrial metals are 45% up on the lows of last year, while a broader commodity price index that includes oil is up 51% off its lows of 2020.

Industrial metals and commodity prices (January 2020=100)

Source: Bloomberg and Investec Wealth & Investment, 11 February 2021

These higher input prices will not automatically lead to higher prices at the factory gate or at the supermarket. Manufacturers and retailers might prefer to pass on higher input costs. But they know better than to ignore the state of demand for their goods and services. They can only charge what their markets will bear, which will depend on demand that in turn will reflect policy settings.

Higher inflation rates cannot be sustained without consistent support from the demand side of the economy. Yet supply side-driven price shocks that depress spending on other goods and services can become inflationary, if accommodated by consistently easier monetary and fiscal policy. In the 1970s, it was not the oil price shocks that were inflationary. They were a severe tax on consumers and producers in the oil importing economies, which in turn depressed demand for all other goods and services. It was the easy monetary policy designed to counter these depressing effects that led to continuous increases in most prices. That was until Fed chief Paul Volker decided otherwise and was able to shut down demand with high interest rates and a contraction in money supply growth that reversed the inflation trends for some 40 years.

The financial markets will be alert to the prospects that demand for goods and services will prove excessive and inflationary in the years to come – and that they may not be dialed back quickly enough to hold back inflation.

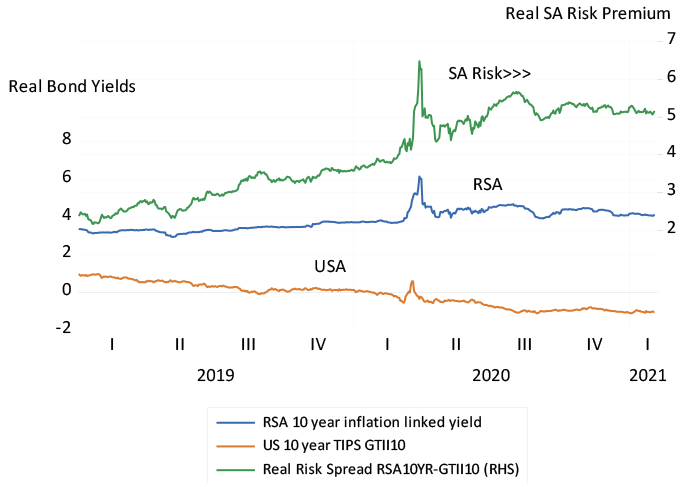

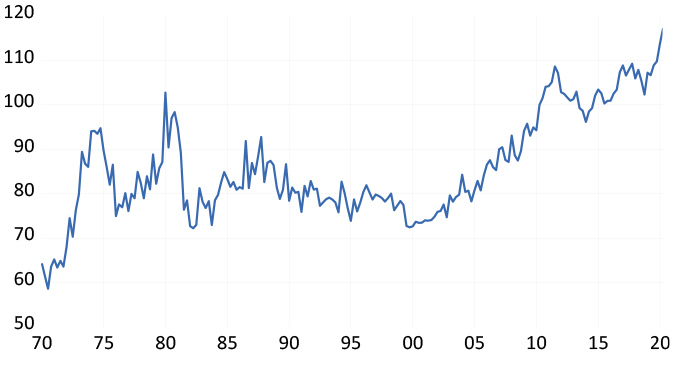

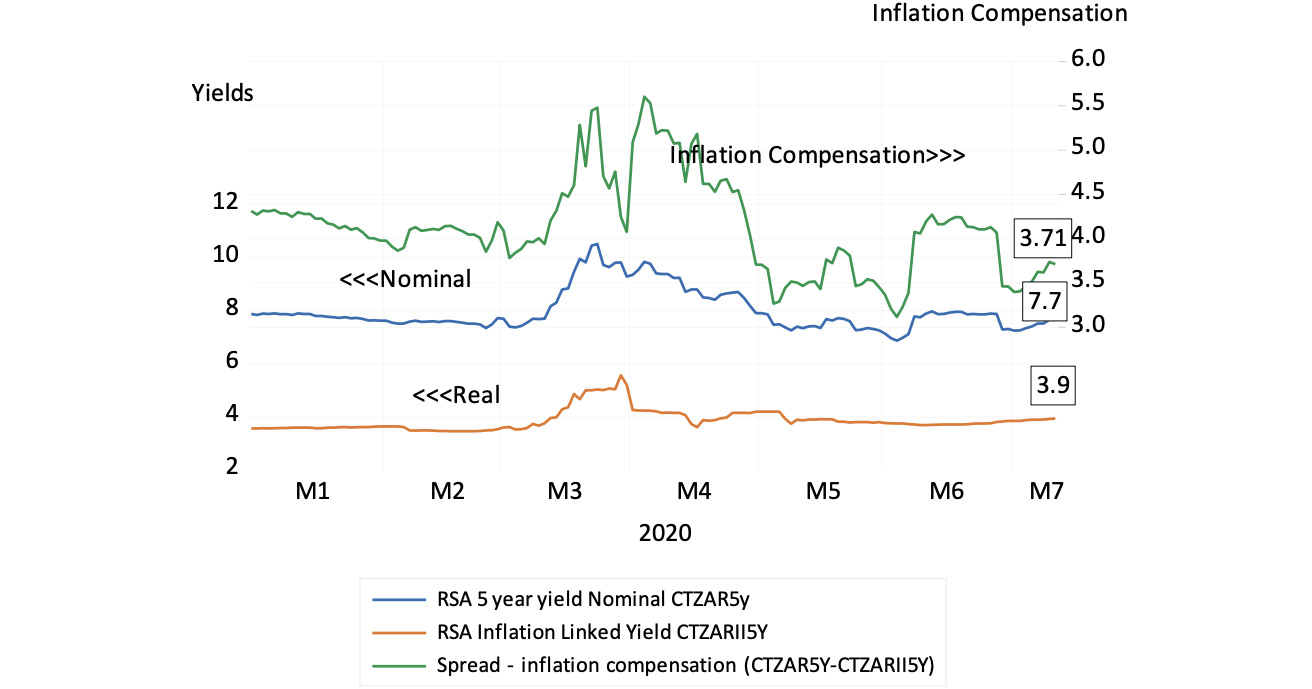

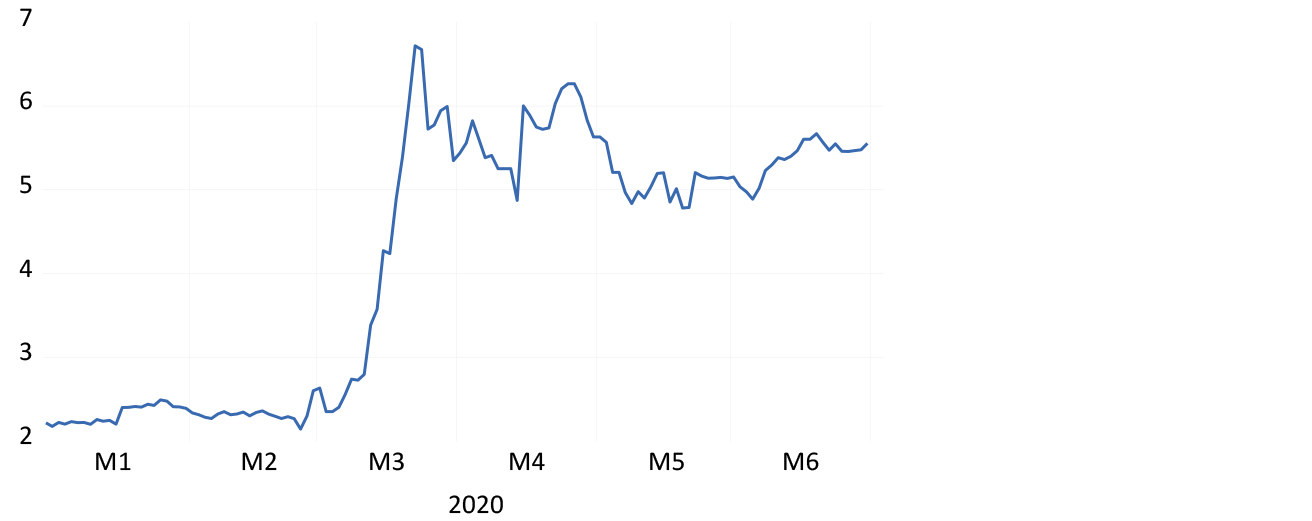

There is consolation for South Africa should global inflation accelerate. It will be accompanied by higher metal prices and perhaps bring a stronger rand to dampen our own inflation. It may also help reduce the large South Africa risk premium that so weakens the incentive to undertake capital expenditure as well as the value of South African business. Our inflation-linked 10-year bonds now yield a real 4.13%, a near record 5.15 percentage points more than US inflation linkers of the same duration. Any reduction in South African risk would thus be welcome.

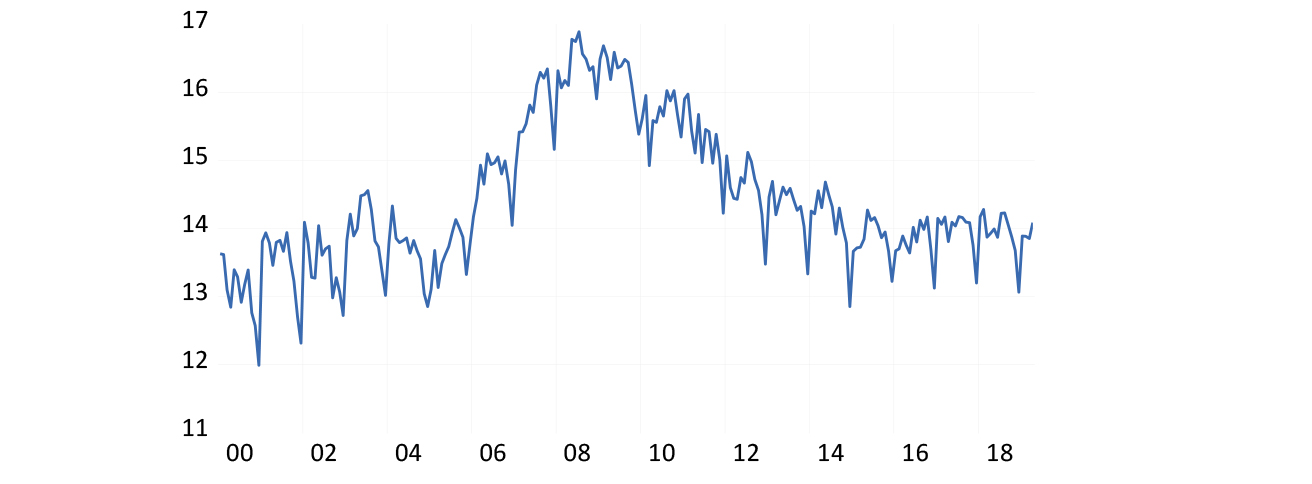

The real South African risk premium

Source: Bloomberg and Investec Wealth & Investment, 11 February 2021

25 January 2021

Vaccines and vacuity – the true costs of not securing vaccine supplies

The failure to secure a large supply of vaccines to help South Africa to reach herd immunity quickly, reveals a vacuity in thinking about the cost to the economy.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

The fiasco over the supply of vaccines reveals fully the vacuity of South Africa’s approach to Covid-19. The deposit of R283m to secure a supply of vaccines was not budgeted for because we didn’t have the money for it – even though money for much else was found in the adjusted Budget.

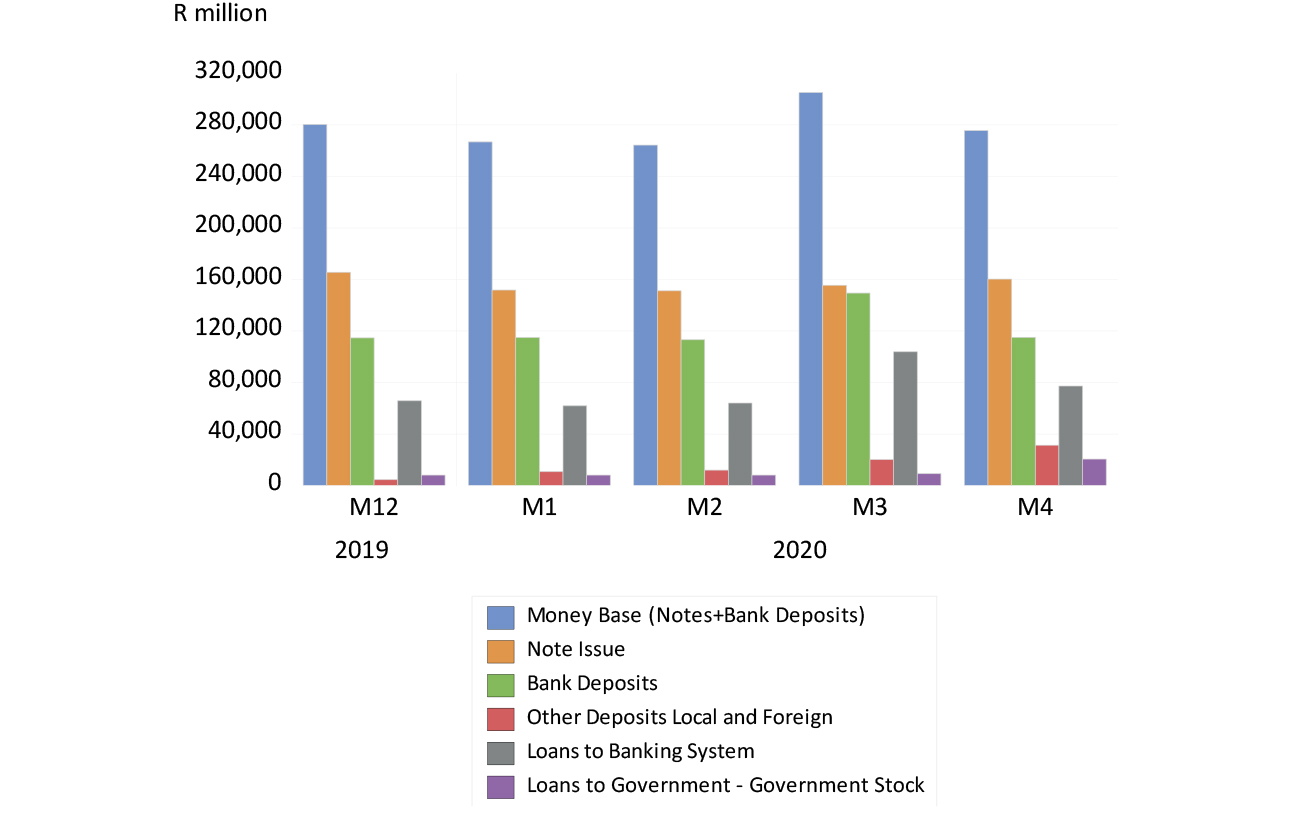

In this context, I observe that the Treasury deposits at the Reserve Bank amounted to R160bn in October, boosted by loans from the IMF and other agencies with anti-pandemic action front of their minds. Has anyone in the Treasury or government attempted to calculate how much additional income will be lost for want of the vaccine – and how much tax revenue the Treasury will not be able to collect?

It will be many times more than the R20bn to be spent on the vaccine. Bear in mind too, that R7bn of this is to be funded by members of medical schemes, which in effect makes it a tax increase or expropriation by any other name, unhelpful given the state of the economy.

Yet a supply of additional money could have been made available by the Reserve Bank, in the same way that money is being created on a large scale by central banks all over the world to fund the extra spending that the lockdowns have made imperative. And the Bank could still do so, to help the Treasury fund the vaccine and the money cost of rolling it out. The idea of raising taxes to fund the extra spending when the economy is under such pressure makes little sense. A higher tax rate or taxing specific incomes will slow the economy even further and might lead to lower tax revenues of all kinds.

Moreover, there is little prospect of more inflation to come. Should inflation emerge at some point, a reversion to normal funding arrangements would be called for. The danger then is that central banks like our Reserve Bank might not act soon enough and inflation picks up. But it is a danger that pales into insignificance when compared with the present danger posed by the pandemic.

Governments around the world know enough economics to know that spending more to help employ workers (and machines) who would otherwise be idle was a costless exercise – costless in the true opportunity cost sense. But South Africa seemingly cannot bring itself to think through the problem this way. The upshot is that South Africa lacks the essential self-confidence to do what would be right now.

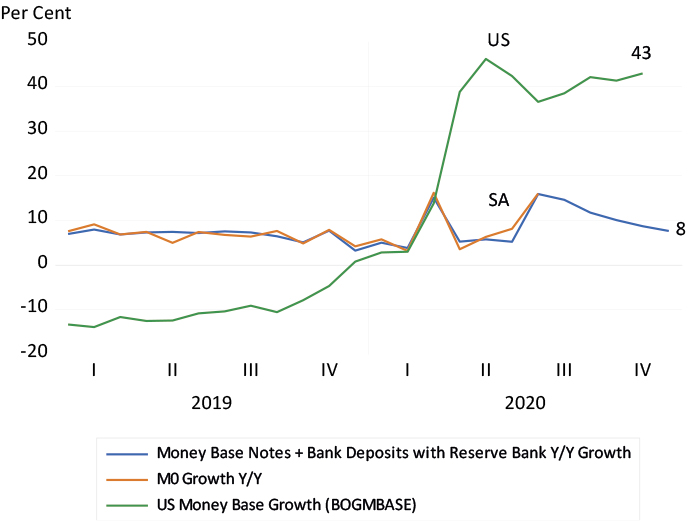

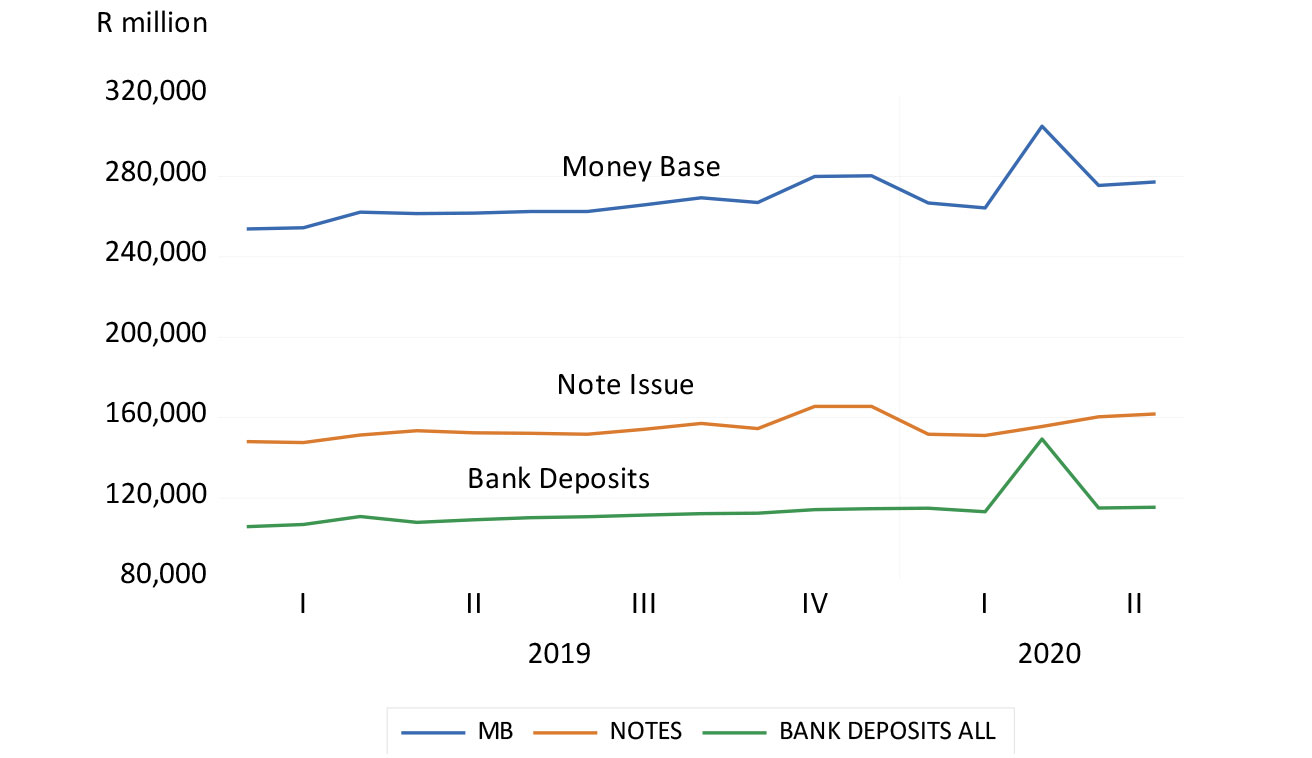

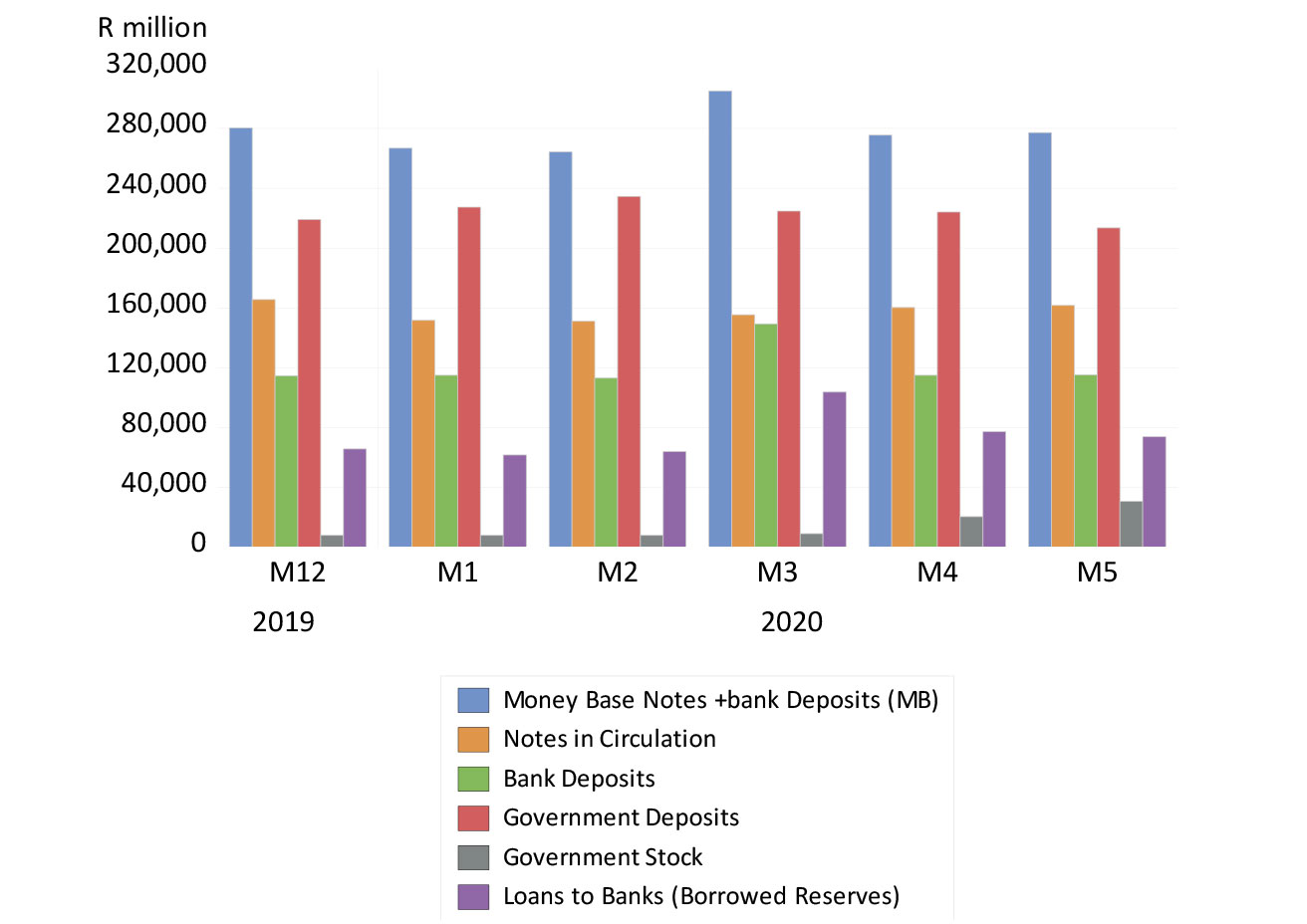

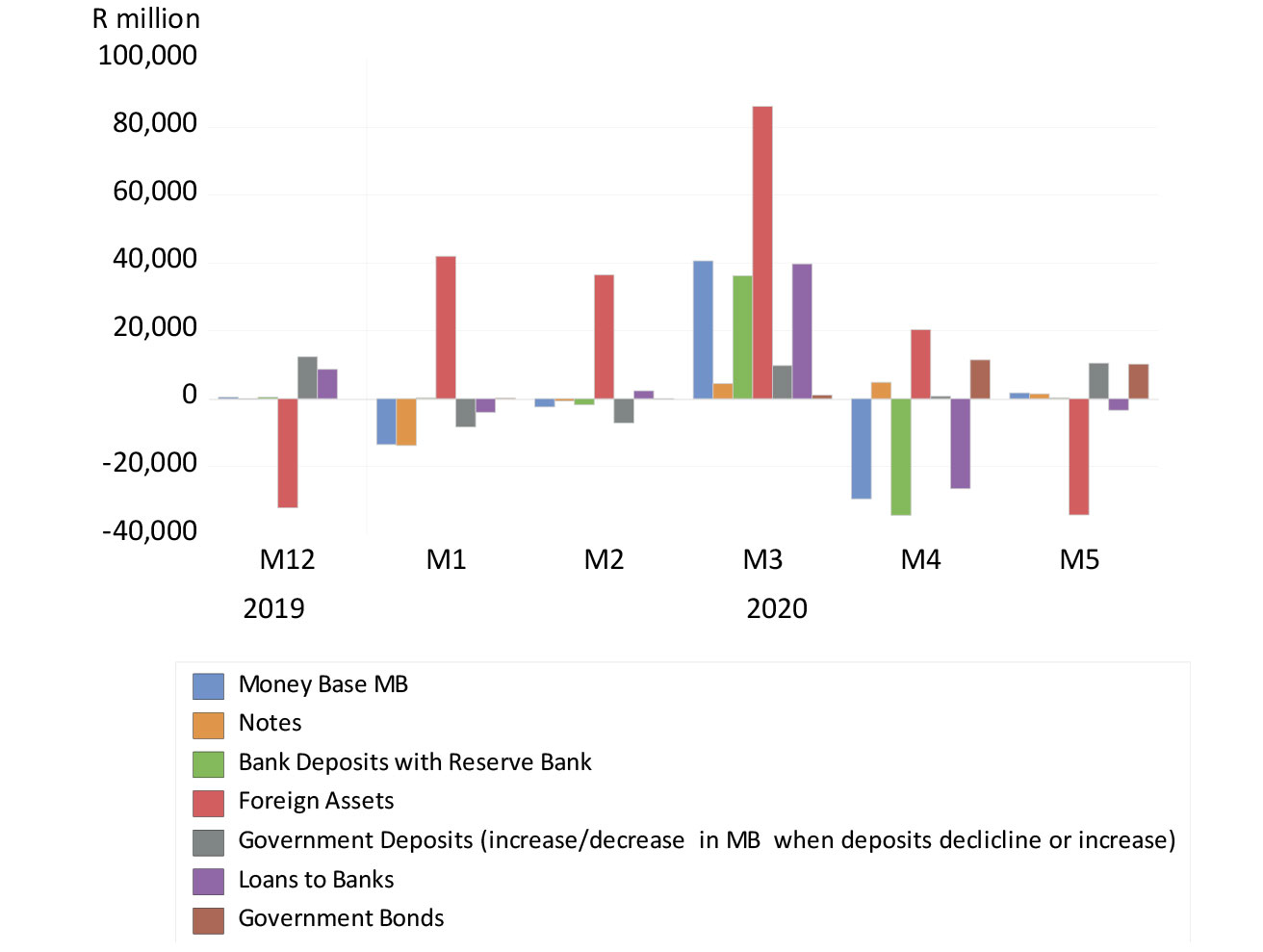

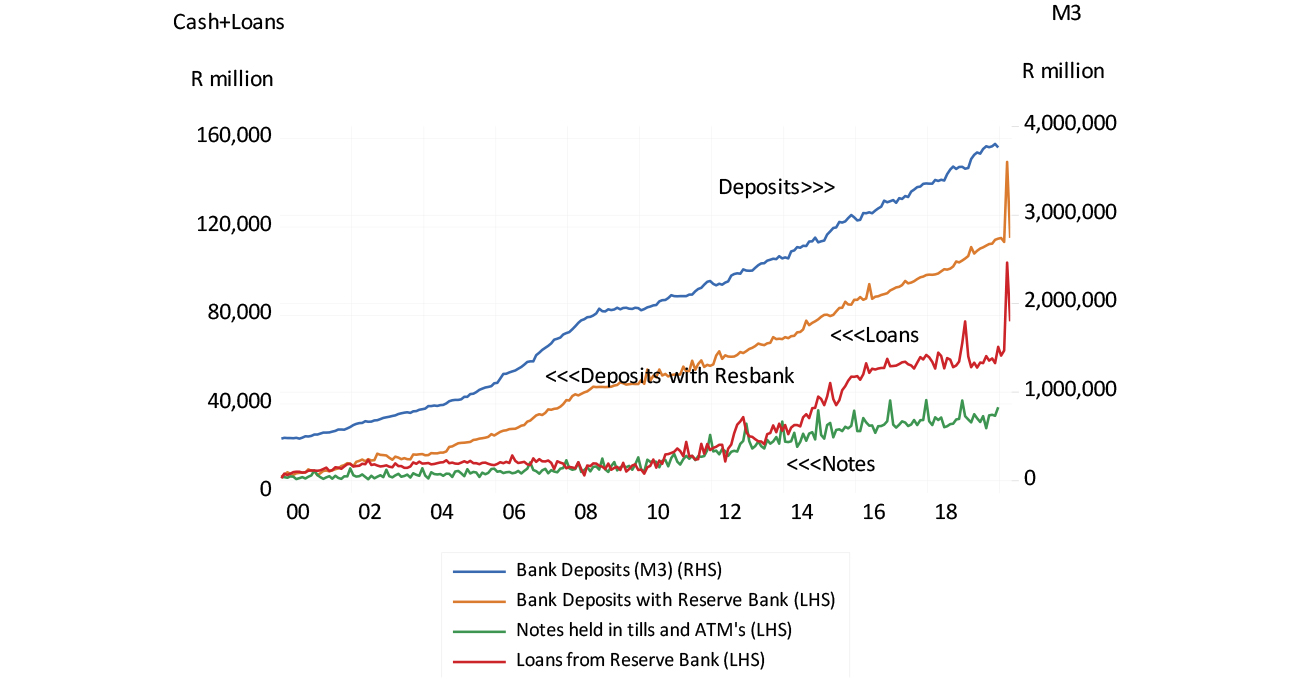

The monetary and financial market statistics tell us how unready the economy is to sustain any recovery of output and employment. The supply of extra Reserve Bank money in the form of notes and deposits by banks with the Reserve Bank, what is described as the money base or M0, rose by 8% in 2020. There was a flurry of extra such money in March and July 2020, since reversed. In the US, the money base is up by 43% (See figure 1).

Figure 1: Annual growth in central bank money, SA and US

Source: SA Reserve Bank, Federal Reserve Bank of St. Louis and Investec Wealth & Investment

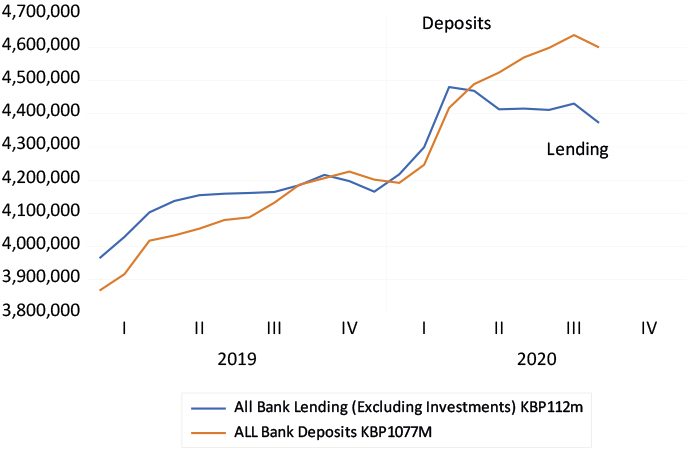

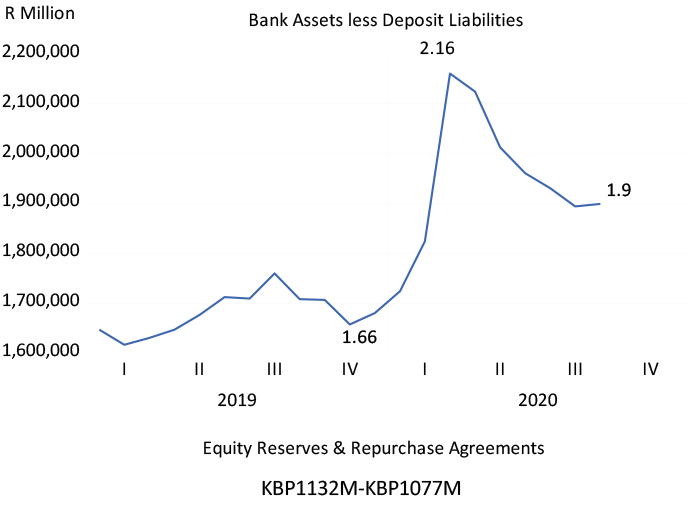

The SA banking system is hunkering down, not gearing up. Bank deposits have been growing at about an 8% rate, while lending to the private sector is up a mere 3%. The banks are building balance sheet strength, raising deposits and are cautious about lending more. They are relying less on repurchase agreements made with the Reserve Bank and other lenders, reserving more against potential bad debts while not paying dividends and hence adding to their reserves of equity capital. All of these act to depress growth.

Figure 2: SA bank deposits and lending (R million)

Source: SA Reserve Bank and Investec Wealth & Investment

Figure 3: SA banks – adding to equity capital

Source: SA Reserve Bank and Investec Wealth & Investment

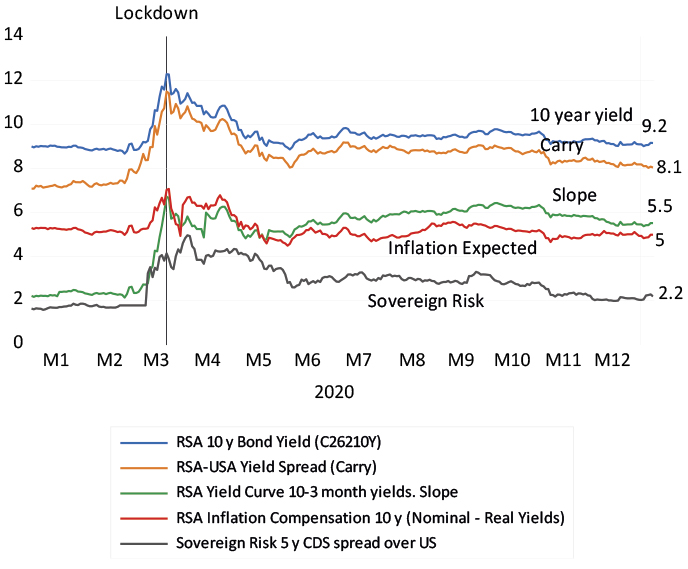

The financial metrics continue to paint a grim picture of the prospects for the SA economy. Long-term interest rates remain above 9%, even as inflation is expected to average 5% over the next 10 years. This makes capital expensive for potential investors who are therefore less likely to add to their plant and equipment. The difference between borrowing long and short remains wide, implying sharp increases in short-term interest rates to come and expensive funding for the government (that is taxpayers) at the long end. The risk of South Africa defaulting on its US dollar debt demands that we pay an extra 2.3% more a year than the US government for dollars over five years.

Figure 4: Key financial metrics in 2020-21

Source: Bloomberg and Invested Wealth & Investment

Poorly judged parsimony and monetary conservatism have brought SA great harm in the fight against Covid-19. They have made the prospects for a recovery in GDP and government revenue appear bleak. It is not too late to change course. We should be funding the extra unavoidable spending on the vaccine and its roll out by drawing on the cash reserves of the government or by raising an overdraft form the Reserve Bank.

17 November 2020

The vaccine and the SA economy – a shot in the arm

The good news on the vaccine front has also been good news for SA markets. To take full advantage, we can help ourselves by making the right policy choices.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

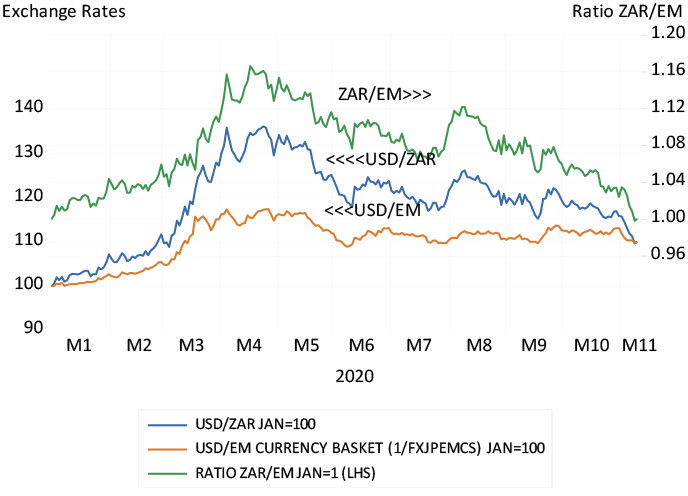

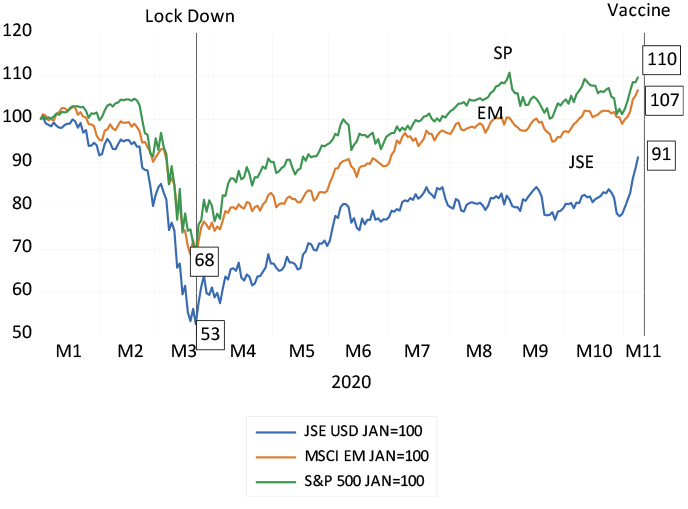

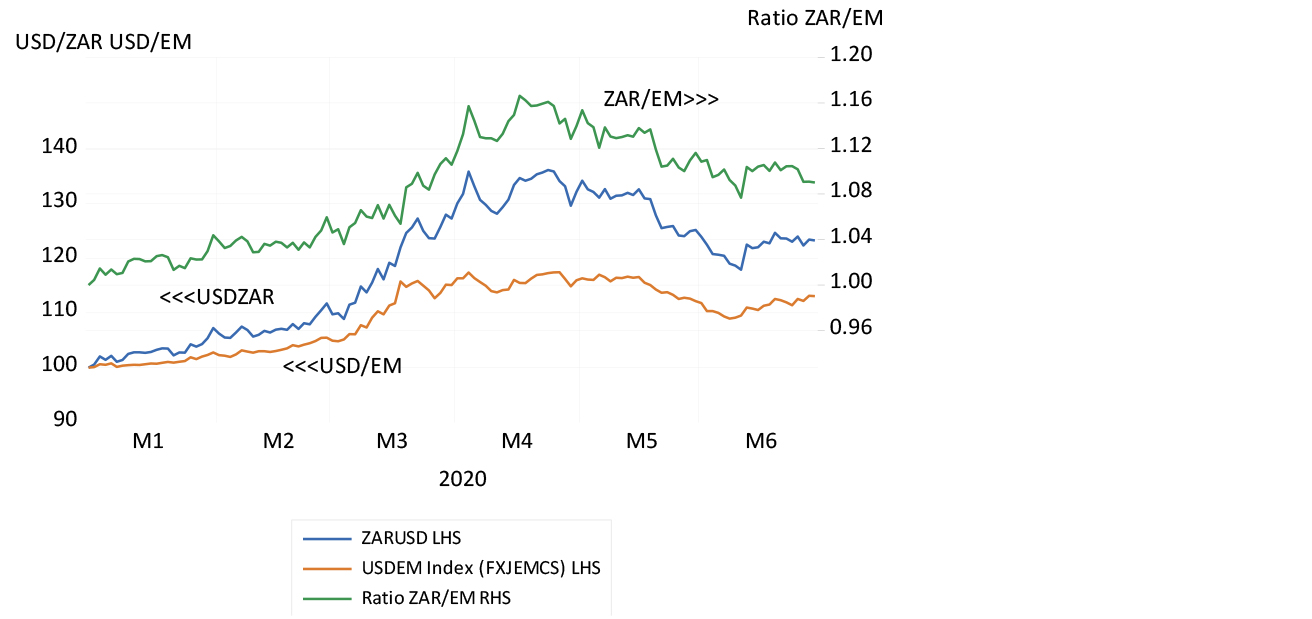

The prospect of an effective vaccine for Covid-19 is good news for investors in SA. The rand has recovered all of the ground it had lost to other emerging market currencies through much of 2020 and is now only about 10% weaker against the US dollar this year. In March, when the uncertainty surrounding Covid-19 was most pronounced, the rand had lost 30% of its US dollar value of January 2020 (see below). The rand has gained about 4% on both the emerging market basket and the US dollar this month.

The rand vs emerging market basket, vs the US dollar and the ratio of the rand to emerging market currencies (higher values indicate dollar strength)

Source: Bloomberg and Investec Wealth & Investment

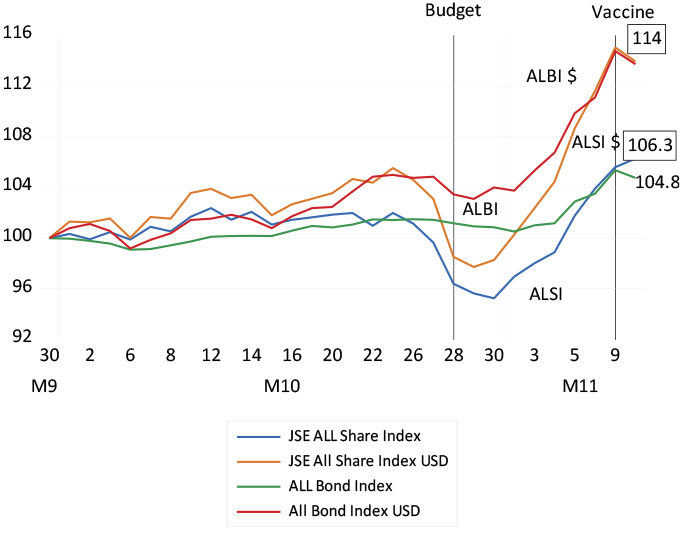

The JSE equity and bond markets consistently also responded well to the good global news, led by the companies that are dependent on the SA economy. The JSE All Share Index since October has gained 14% in USD and the JSE All Bond Index has appreciated by a similar 14% in US dollars. The emerging market index was up by 9.1% over the same period, while the US benchmark the S&P 500 gained 5.4%. The JSE has been a distinct outperformer recently (see below).

The JSE equity and bond indexes

Source: Bloomberg and Investec Wealth & Investment

The JSE, S&P 500 and MSCI EM Indexes (In US dollars)

Source: Bloomberg and Investec Wealth & Investment

These developments should not have come as a complete surprise. Favourable reactions in the SA financial markets to a reduction in global uncertainties, usually accompanied by a weaker US dollar, are predictable. What South Africans lose in the currency and financial markets when the world economy appears less certain, we regain when risk tolerance improves. SA unfortunately is amongst the riskiest of destinations for capital among investors, who always demand higher returns as compensation for the risks they estimate. As taxpayers, we pay out more interest and our companies have to offer higher prospective returns than almost anywhere else where capital flows freely, as it does to and from Johannesburg.

Recent developments in the markets do provide some relief for our beleaguered economy. The yield on long-dated government bonds has declined by more than a half a percent this month. With an unchanged outlook for profits, such a reduction in the discount rate applied to expected income could add 10% to the present value of a SA business or roughly 10% its price-to-earnings ratio (market reactions confirm this). A further reduction in these high required returns – now equivalent to about 9% a year after expected inflation – is much needed to encourage SA businesses to invest more. It’s essential if our economy is to grow faster.

Yet if the economy were expected to grow sustainably faster, the discount rate would come down much further and businesses would be willing to invest more in SA. Foreign investors would willingly supply us with their savings to do so. The SA government would therefore be confidently expected to raise enough revenue to avoid the danger of a debt trap and a much weaker rand – expectations that are fully reflected in our high bond yields.

We can hope for the stars to align, but should not expect them to do so. We can help ourselves by making the right policy choices. Opportunity presents itself in a number of ways. The terms at which we engage in foreign trade have improved consistently in recent years, by 20% since 2015 (think metal prices over oil prices). These relative price trends are even more favourable than they were in the 1970s when the gold price took off. These developments should spur output and investment by business, government policy permitting.

Another, related large opportunity is presented by the discovery of a major energy resource off our southern coast. Bringing the gas ashore can accelerate infrastructure and export led growth, funded by foreign capital, not domestic taxpayers, and led by business not government. It demands the kind of urgency that has brought us a vaccine.

SA’s terms of foreign trade – export prices/import prices (2010=100)

Source: SA Reserve Bank Investec Wealth & Investment

22 September 2020

PSG and Capitec – Shareholders’ (un)bundle of joy

By unbundling Capitec, PSG has done the right thing for shareholders – but shareholders remain sceptical about its prospects.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

PSG shareholders should be pleased. The decision to unbundle PSG’s stake in Capitec has delivered approximately R7.85bn extra to them. This estimated value add for PSG shareholders is calculated by eliminating the discount previously applied to the value of the Capitec shares held indirectly by PSG.

Without the unbundling, the discount applied to the assets of PSG would have been maintained to reduce the value of their Capitec shares. The market value of the 28.1% of all Capitec shares unbundled to PSG shareholders, worth R960 a Capitec share, would have been worth R31.4bn on 16 September. These Capitec shares might have been worth 25% less, or nearly R8bn, to PSG shareholders, had it been kept on the books.

The PSG holding in Capitec had accounted for a very important 70% of the net asset value (NAV) or the sum of parts of PSG. Before the unbundling cautionary was issued in April 2020, the difference between the NAV and market value of PSG, the discount to NAV, had risen to well over 30%. The difference in NAV and market value of PSG was then approximately R20bn in absolute terms. The discount to NAV then narrowed to about 18% when the decision to proceed with the unbundling was confirmed.

Now with the unbundling complete, PSG again trades at a much wider discount of 40% or so to its much-reduced NAV.

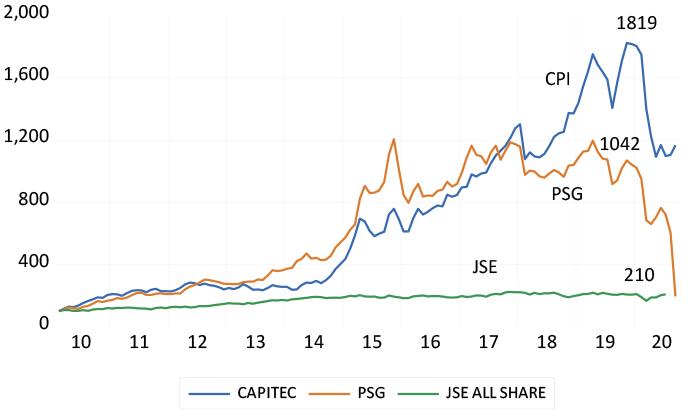

Capitec and PSG delivered well above market returns after 2010. By the end of 2019, the Capitec share price was up over 18 times compared to its 2010 value. By comparison, the PSG share price was then 10 times its 2010 value, and the JSE 2.1 times. The Capitec share price strongly outpaced that of PSG only after 2017.

The Capitec and PSG share prices, compared to the JSE All Share Index (2010 = 100)

Source: Iress and Investec Wealth & Investment

The better the established assets of a holding company perform, as in the case of a Capitec held by PSG or a Tencent held by Naspers, the more valuable will be the holding company. Its NAV and market value will rise together but the gap between them may remain wide. Investors will do more than count the value of the listed and unlisted assets reported by the holding company. They will estimate the future cost of running the head office, including the cost of share options and other benefits provided to managers of the holding company. They will deduct any negative estimate of the present value of head office from its market value. They may attach a lower value to unlisted assets than that reported by the company and included in its NAV.

Investors will also attempt to value the potential pipeline of investments the holding company is expected to undertake. These investments may well be expected to earn less than their cost of capital, in other words, deliver lower returns than shareholders could expect from the wider market. These investments would therefore be expected to diminish the value of the company rather than add to it. They are thus expected to be worth less than the cash allocated to them.

To illustrate this point, assume a company is expected to invest R100 of its cash in a new venture (it may even borrow the cash to be invested or sell shares in its holdings to do so). But the prospects for the investments or acquisitions are not regarded as promising at all. Assume further that the investment programme is expected to realise a rate of return only half of that expected from the market place for similarly risky companies. In that case, an investment that costs R100 can only be worth half as much to its shareholders. Hence half of the cash allocated to the investment programme or R50 would have to be deducted from its current market value.

All that value that is expected to be lost in holding company activity will then be offset by a lower share price and market value for the holding company – low enough to provide competitive returns with the market. This leads to a market value for the company that is less than its NAV. This value loss, the difference between what the holding company is worth to its shareholders and what it would be worth if the company would be unwound, calls for action from the holding company of the sort taken by PSG. It calls for more disciplined allocations of shareholder capital and a much less ambitious investment programme. The company should rather shrink, through share buy backs and dividends, and unbundling its listed assets, rather than attempt to grow. It calls for unbundling and a lean head office and incentives for managers linked directly to adding value for shareholders by narrowing the absolute difference between NAV and market value. Management incentives, for that matter, should not be related to the performance of the shares in successful companies owned by the holding company, to which little or no management contribution is made.

On that score, a final point directed towards Naspers and its management: the gap between your NAV and market value runs into not billions, but trillions of rands. This gap represents an extremely negative judgment by investors. It reflects the likelihood of value-destroying capital allocations that are expected to continue on a gargantuan scale. It also reflects the cost of what is expected to remain an indulgent and expensive head office.

03 September 2020

The case for funding with equity, not debt

Two recent cases of JSE-listed companies reveal the advantages of equity funding over debt funding.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

While issuing debt can be more dangerous than issuing equity, it receives more encouragement from shareholders and the regulators. Debt has more upside potential: if a borrower can return more than the costs of funding the debt (return on equity improves) and there is less to be shared with fellow shareholders.

But this upside comes with the extra risk that shareholders will bear should the transactions funded with debt turn out poorly. Any increase in the risk of default will reduce the value of the equity in the firm – perhaps significantly so.

The accounting model of the firm regards equity finance as incurring no charge against earnings. You might think it would help the argument for raising permanent equity capital rather than temporary debt capital. But this is clearly not the case, with the rules and regulations and laws that govern the capital structure of companies. It is also represented in the attitude of shareholders to the issuing of additional equity. They have come to grant ever less discretion to company boards to issue equity. Less so with risky debt.

(Note: I am grateful to Paul Theodosiou for the following explanation of the different treatment of debt and equity capital raising. Paul was until recently non-executive chairman of JSE-listed REIT, Self Storage (SSS), and previously MD of the now de-listed Accucap of which I was the non-executive chairman).

Typically at the AGM, a company will seek two approvals in respect of shares - a general approval to issue shares for cash (which these days is very limited - 5% of shares in issue is the norm) and an approval to place unissued shares under the control of directors (to be utilised for specific transactions that will require shareholder approval). These need 75% approval. So shareholders keep a fairly tight rein on the issue of shares.

Taking on or issuing debt, on the other hand, leaves management with far more discretion. Debt instruments can be listed on the JSE without shareholder approval, and bank debt can be taken on at management’s discretion. The checks and balances are more broad and general when it comes to debt. Firstly, the memorandum of incorporation will normally have a limit of some kind (for REITs, the loan to value ratio limits the amount of debt relative to the value of the assets). If the company is nominally within its self-imposed limits, shareholders have no say. Secondly, the JSE rules provide for transactions to be categorised, and above a certain size relative to market cap, shareholders must be given the right to approve by way of a circular issued and a meeting called. The circular will spell out how much debt and equity will be used to finance the transaction, and here the shareholders will have discretion to vote for or against the deal. If they don’t approve of the company taking on debt, they can vote at this stage. Thirdly, shareholders can reward or punish management for the way they manage the company’s capital structure - but this is a weak control that involves engaging with management in the first instance to try and persuade, and disinvesting if there isn’t a satisfactory response.)

It is better practice however to separate the investment and financing decisions to be made by a firm.

Perhaps the implicit value of the debt shield – taxes saved by expensing interest payments – without regard to the increase in default risk, confuses the issues for investors and regulators. It is better practice however to separate the investment and financing decisions to be made by a firm. The first step is to establish that an investment can be expected to beat its cost of capital, whatever the source of capital, including internally generated cash that could be given back to shareholders for want of profitable opportunities. When this condition is satisfied, the best (risk adjusted) method of funding the investment can be given attention.

The apparent aversion to issuing equity capital to fund potentially profitable investments seems therefore illogical. Or maybe it represents risk-loving rather than risk-averse behaviour. Debt provides potentially more upside for established shareholders and especially managers, who may benefit most from incentives linked to the upside.

Raising additional equity capital from external sources to supplement internal sources of equity capital is what the true growth companies are able to do. And true growth companies do not pay cash dividends, they reinvest them, earning economic value added (EVA) for their shareholders. A smaller share of a larger cake is clearly worth more to all shareholders.

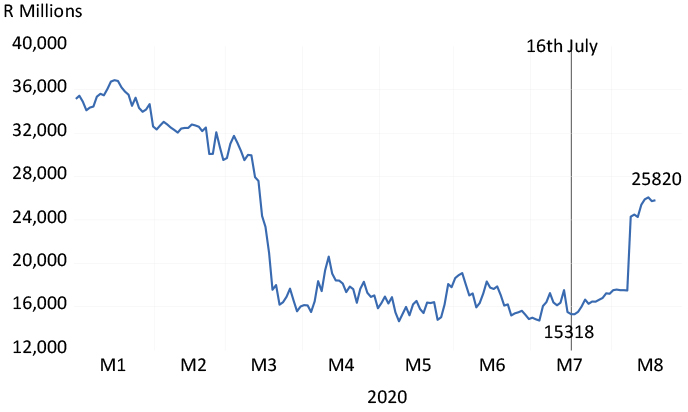

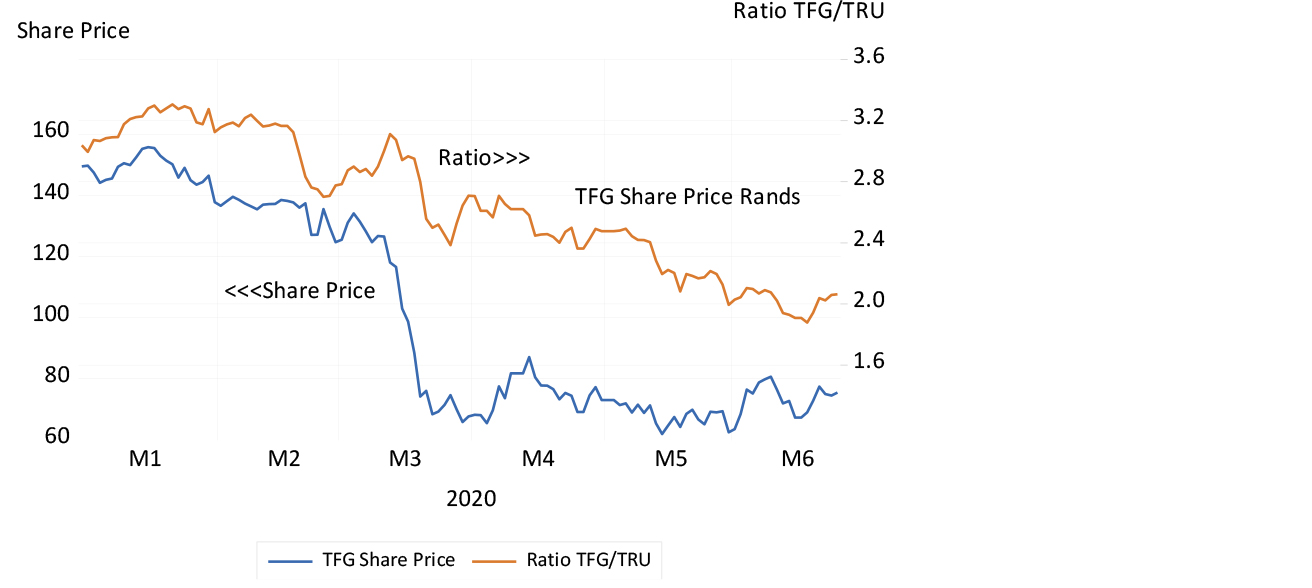

There are two recent JSE cases worthy of notice. Foschini shareholders approved the subscription of an extra R3.95bn of capital on 16 July to add about 20% to the number of shares in issue. By 19 August, the company was worth R25.8bn, or R10.5bn more than its market value on 16 July, or R6.5bn more than the extra capital raised. The higher share price therefore has already more than compensated for the additional shares in issue.

The Foschini Group – market value to 19 August 2020

Source: Bloomberg, Investec Wealth & Investment

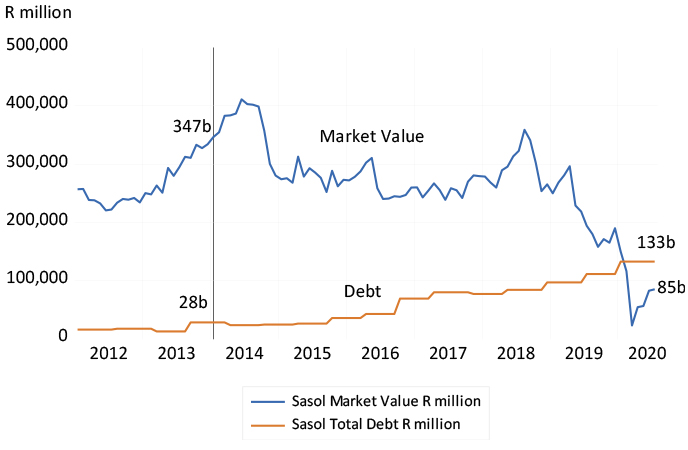

The other example is Sasol, now with a market value of about R87bn, heavily depressed by about R110bn of outstanding debt. The extra debt was mostly incurred funding the Lake Charles refinery that ran far over its planned cost and called for extra debt. Sasol was worth over R400bn in early 2014, with debts then of a mere R28bn. The recent market value, now less than the value of its debts, is clearly being supported by the prospect of asset sales and a potential capital raise.

The company would surely be much stronger had the original investment in Lake Charles been covered more fully by additional equity capital, capital they might have been able to raise with much less dilution. It might also have prevented the new management team from having to sell off what might yet prove to be valuable family silver – assets capable of earning a return above their cost of capital. In this case, a large rights issue could still be justified to bring down the debt to a manageable level and, as with the Foschini increase, the value of its shares by more (proportionately) than the number of extra shares issued.

Sasol – market value and total debt, 2012 to July 2020

Source: Bloomberg, Investec Wealth & Investment

19 August 2020

How to build the confidence needed to borrow and lend

An economic recovery programme for South Africa demands the kind of business and political leadership that now appears to be lacking.

Professor Brian Kantor / Chief economist and strategist, Investec Wealth & Investment

These are truly unprecedented economic times. Never before have large sectors of our own and most other economies been told to stop working. Large numbers of potential participants in the economy are being forced to stay at home. The impact on the supply of goods and services, the demand for them and the incomes normally earned producing and distributing them, has been devastating. Perhaps up to 20% of potential output, or GDP in a normal year, will have been sacrificed globally to the cause. We will know how much has been sacrificed only when we look back and are able to do the calculations.

In South Africa’s case this one fifth of GDP would amount to about R1 trillion of income permanently lost. These are extraordinary declines in output and income. Ordinary recessions, when GDP declines by 2% or 3% in a quarter or a year, are much less severe than this.

Compensation however can be paid to the households and business owners who, through no fault of their own, have lost income and wealth. It is being provided on different scales of generosity across the globe. The richer countries are noticeably more generous than their poorer cousins. South Africa, alas, is among the more parsimonious, at least to date in practice.

There is however no way to recover what has been lost in production. All that can be hoped for is a speedy recovery of the economy when businesses and their employees are allowed to get back to normal. But getting back to producing as much as before the lockdowns means not only more output and jobs becoming available. Any recovery in output will have to be accompanied by more demand for the goods and services that the surviving business enterprises can supply. Without additional spending during the recovery process, there will not be additional supplies of goods, services, jobs and incomes.

In the US, every household received a cheque in the post of over $1000 and temporary unemployment benefits of $600 per week were more than many would have earned. The average US household will come out of the crisis with more cash than they had before.

Providing unemployment benefits and other benefits paid in cash to the victims of the lockdowns will help to stimulate spending. In the US, every household received a cheque in the post of over $1000 and temporary unemployment benefits of $600 per week were more than many would have earned. The average US household will come out of the crisis with more cash than they had before. And more may be on the way. Spending the cash will help the pace of recovery.

The US and many other countries will be doing what it takes to get back to normal. They will also be learning along the way just how much spending by governments it will take before they can take their feet off the accelerators. They are not being constrained by the monetary cost of such spending programmes. The cheapest way for a government to fund spending is by printing money and redeeming the money issued with more money.

The central banks of developed economies are supplying large extra amounts of cash to their economies in a process of money creation also known as quantitative easing or bond purchasing programmes. The supply of central bank cash in the largest economies has grown 30% this year. Central banks have been buying financial securities, mostly issued by their governments in exchange for their cash that is so willingly accepted in exchange. By so doing, they have helped force down the interest rates their governments pay lenders to very low levels – sometimes even below zero for all government debt, short and long dated. This is an outcome that has made issuing government debt even for 10 years or more even cheaper than issuing money.

These governments have also arranged on an even larger scale (relative to GDP) loan guarantee schemes for their banks to encourage bank lending that will enable businesses that have bled cash during the lockdowns to recapitalise, on favourable terms. Central banks, secured by funds committed by their governments, are covering up to 95% of any losses the banks might suffer if the loans are not repaid. The take-up of such loans by businesses in the US has been very brisk.

South Africa, as mentioned, has not adopted any do-what-it-takes approach to our crisis of perhaps larger relative dimensions. I have argued that we should practise the same logic as the developed economies and rely in the same way on our central bank to create money to hold down the interest cost of funding higher government spending and the accompanying debt. This would be a similarly temporary exercise in economic relief – one well-explained and understood as such – for only as long as it takes.

Leadership should want large and small businesses to believe in their prospects after the lockdown and to act accordingly.