Get Focus insights straight to your inbox

From 1995 to 2015, South African GDP growth averaged at the 38th percentile across the globe (i.e. each year typically 62% of countries had a higher GDP growth rate than SA). While this in itself was weak for a developing country, there has been a major deterioration still since then.

There is a material chance that South African growth remains in the 20th to 30th percentile over the foreseeable future (The IMF expects much worse – for growth to average at the 13th percentile for the next three years, in other words, to be lower than 87% of countries).

There’s no shortage of blockages for growth, some of which we detail below. The purpose of this note is to identify the South African-listed stocks that are likely to do well even in an environment of stagnation. The list of stocks that will do well should South African growth beat expectations is intuitively obvious (retailers, banks and midcaps), as is the list of stocks that will protect against the scenario the IMF forecasts (rand hedges). What is less obvious is which companies are likely to thrive in an environment where the status quo of gradual structural decline continues.

Obstacles

Other than SA’s national roads, the deterioration and failure of SA’s state infrastructure are widespread and accelerating. There are many reasons for this, including a lack of policy coordination across ministerial portfolios, corruption, poor management, lack of maintenance capex, and inertia in new capacity planning – let alone delivery.

The culture of non-payment for utility services is exacerbated by poor billing and collection efforts. Administrative failures at the municipal level often result in national grants being returned to Treasury, because they are linked to new infrastructure projects and not necessarily to maintenance capex.

The breakdown of state bulk infrastructure and the dearth of expansion is essentially resulting in privatisation by stealth. The void left by the public sector will therefore be filled by the private sector to some extent.

In addition to renewable and alternative energy generation projects, electricity transmission, rail, ports, and water infrastructure all require large amounts of capex investment.

Transnet’s volumes are 30% lower than in 2018, and, according to Stellenbosch University, this has resulted in a 2% loss in GDP.

Africa’s Rail Industry Association estimates that R100bn alone is required to restore our railway track integrity.

Drinking water and wastewater management is an issue in three-quarters of South Africa’s metros. The SA government has allocated R40bn a year to the municipalities to address this but this is unlikely to be sufficient since, for instance, Johannesburg alone has stated that it requires R60bn a year over 10 years, against its allocation of R40bn a year over five years.

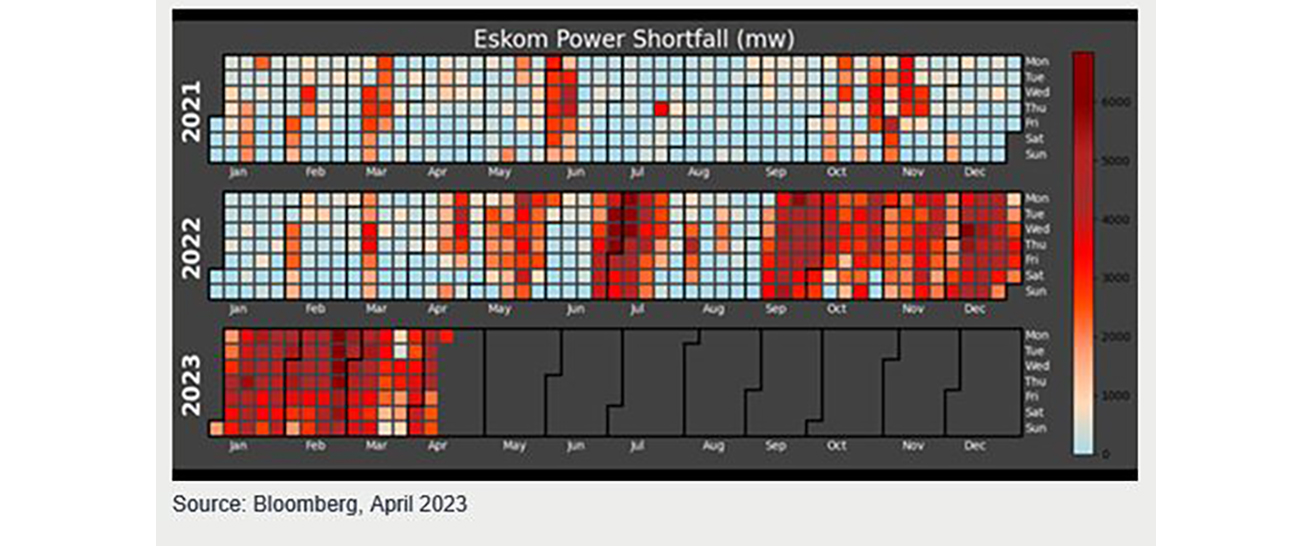

Now in our 15th year of load shedding, the situation has deteriorated, particularly since September last year (see graphic below). We expect at least another two years of intense load shedding.

Electricity generation requires large amounts of investment from the private sector while Eskom relinquishes its monopoly on generation, and is now prohibited from new generation capex as a condition of Treasury’s restructuring of its debt. The major challenge in electricity, however, is transmission and requires at least R50bn of investment to increase capacity to connect the various private sector producers to the grid.

Increasingly, the state requires the assistance and involvement of the private sector to either operate or deliver on bulk infrastructure, through deregulation of energy generation, tenders to operate certain ports and concessions on railway lines.

Competition from the private sector in education, health and security is understandable and offers users a choice, at a cost. However, competition from the private sector in bulk infrastructure delivery is an embarrassing outcome for a ruling party that espouses socialist principles; nonetheless, it provides a significant growth opportunity for the private sector, in our view.

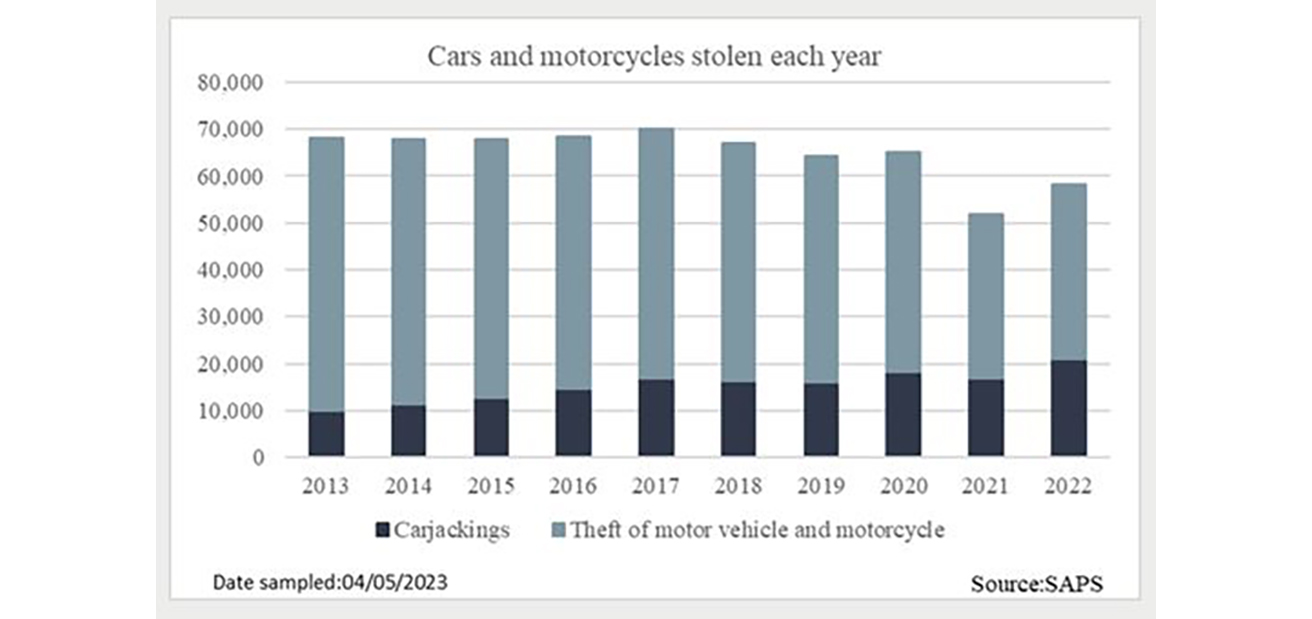

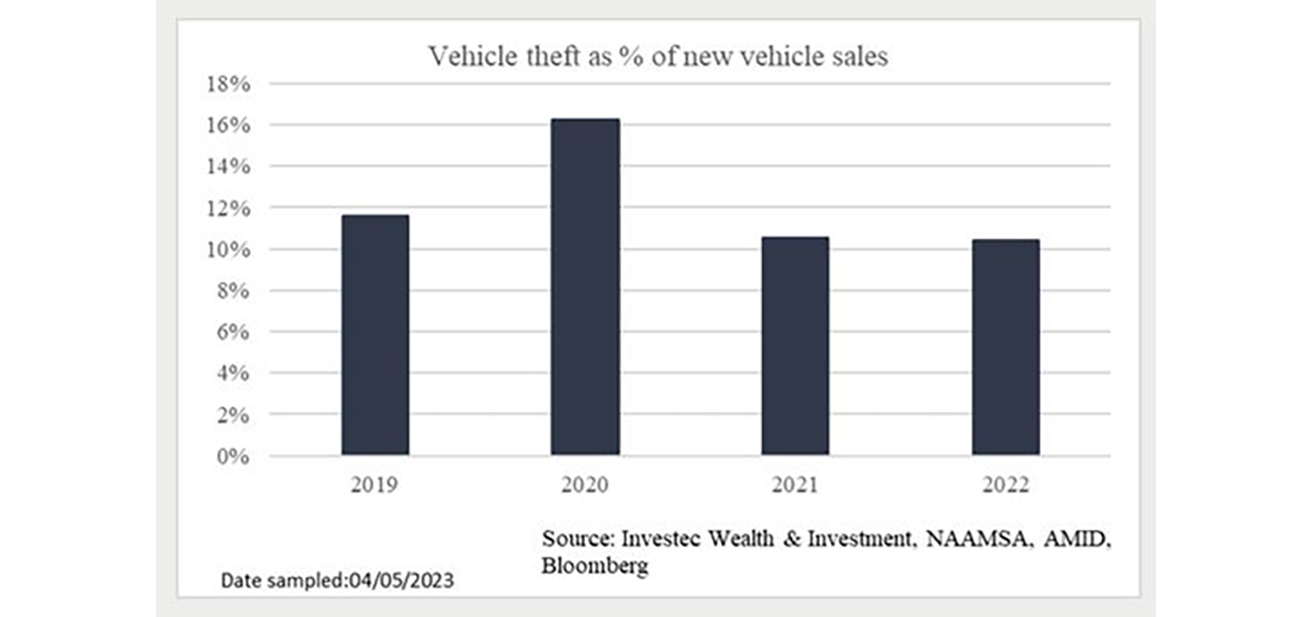

State failure is also evident in the crime statistics. For example, 60,000 cars and motorcycles are either stolen or hijacked each year, a number not materially below the level a decade ago.

To put that into context, roughly 10% of new vehicle sales are replacing stolen/highjacked cars and motorbikes.

A coordinated effort and a national framework, including regulation, will be key to solving South Africa’s SOE/state/infrastructure failures.

In the next section, we try to highlight some JSE-listed companies that can benefit from opportunities arising from the deteriorating condition of infrastructure, beyond the obvious rand hedges and commodity companies.

Macro Monday

Bookmark this page for weekly insights

A weekly macroeconomic overview from Investec Wealth & Investment's chief investment strategist, Chris Holdsworth.

Likely beneficiaries of state infrastructure failure

According to the SA Reserve Bank, the sectors hardest hit by load shedding are food retailers and the related agriculture supply chain (irrigation, poultry, dairy, abattoirs, millers, food processors) followed by manufacturing, mining, transport, storage, and communication. The least hard hit are personal services, general government, finance, insurance, real estate, and business services.

Let’s take a closer look at some of the potential beneficiaries. This is not an exhaustive list, but represents a cross-section of the companies we look at.

Bidvest

Although the company has recently diversified into the UK and Australia, South Africa still represents about 80% of profits. Despite this, we believe that the company is well placed to benefit from private sector opportunities offered by state-owned enterprises.

Bidvest touches many aspects of the local economy. Management sees Eskom’s power supply issues as a business continuity risk and not just a load-shedding risk. That said, it adopts a glass-half-full approach and it is optimistic about the future despite the challenging economy. We believe Bidvest will continue to grow its market share in South Africa.

Load shedding is negatively impacting operational costs, particularly in factories and manufacturing, and is severely impacting electrical appliance sales. According to management, renewables and the Voltex division are growing sales at double that for the market, even though renewables remain small within the broader group. We understand that renewables will represent less than 1% of group turnover for the 2023 financial year. Load shedding is increasing the demand for security services, but this is offset to some extent by lower demand for air cargo because of softer economic activity.

Freight had a strong first half of the financial year as cargo has been redirected from rail to road and different ports in southern Africa. Clearing, forwarding, and warehousing were strong. Demand for bulk commodities is supporting terminal activity. Liquids and liquid petroleum gas (LPG) volumes increased. The division faces a tough base due to the above, in our view. Investment in the Gauteng LPG terminal is subject to the lack of certainty about rail capacity.

Bidvest is likely to benefit from public sector opportunities by participating in the concessions and tenders that are part of Transnet’s Port Master Plan. Capex and public-private partnerships (PPPs) offer growth opportunities in freight operations. It is in discussion with Transnet to move its bulk commodity facility from Durban to Richards Bay.

The Natcor (Natal corridor railway line) container line is out to tender on a 10-year concession. We await the announcement of the preferred bidder for the planned build of the liquified natural gas (LNG) import terminal, which includes gas-fired power plants of 3GW each, storage facilities and transmission pipelines.

Hudaco

Despite its clients being negatively impacted by government’s malaise, Hudaco has delivered solid growth over the last two years. Its decentralised entrepreneurial model places it in a strong position to overcome the challenges and benefit from the opportunities arising from the collapse in local and bulk infrastructure.

Load shedding is improving the prospects for its security and communications businesses. Automotive replacement parts demand is healthy due to the growing and aging second-hand carpool. Alternative energy supplier Hudaco Energy is growing strongly and adds to the energy cluster (diesel generators, batteries, and electrical businesses).

The group’s engineering consumer cluster supplies parts that wear and require regular replacement.

In addition to distribution, many of its businesses have a large element of technical value-added services.

Bidcorp

To a large extent Bidcorp is unaffected by South Africa’s state infrastructure challenges since only around 10% of group trading profit is from South Africa. Within the country, its food manufacturing operations have been worst impacted. Its food service operations benefit to some extent from at-home meals shifting to restaurants and hotels.

Shoprite

In our view, Shoprite remains a quality food retailer – of strategy, execution, operations, and management. Through capital investment, we believe that the group is well placed to absorb operational challenges from an unstable electricity supply and to be able to ensure an uninterrupted shopping experience for consumers while keeping selling price inflation under control. We are impressed with the group’s continued execution of its brand proposition and believe that it should continue to exercise its dominance as consumers trade down. The group is well positioned through different income ranges and is agile enough to pivot to any end of the market as economic circumstances change. The inclusion of the former Masscash assets could help short-term earnings growth although the impact of rising trading expenses reverses potential gains from expansions and acquisitions.

There is probably a case for a re-rating in Pick ‘n Pay following the recent sell-off and the incremental gains that could be achieved through the Ekuseni strategy, its long-term strategy for the next phase of growth, including the accelerated growth in its Boxer, clothing and online formats. However, Shoprite remains dominant in the local food retail sector with leading market share, lower operational gearing and better margins than Pick ‘n Pay. On the premise that South Africa experiences weak economic growth and consumer spending remains under pressure, Shoprite's ability to trade through the income spectrum and it being the obvious choice for consumers during times of trading down, Shoprite maintains a competitive edge over its local peers.

Clicks

Failing government healthcare could move to private care dispensaries.

Clicks is a highly rated quality company, having historically delivered greater than 100% cash conversion on healthy operating margins with a large market share.

As the best available option for dispensary services and basic healthcare provision, the retail pharmacy groups are beneficiaries of government’s failure to provide healthcare services in our view. This is evidenced by the sector’s additional sales due to its ability to administer the Covid-19 vaccine during the pandemic.

We understand that Clicks and Dis-Chem are dispensing additional medicines for government, thereby providing an opportunity to recapture part of the additional footfall enjoyed during the vaccine rollout. Clicks already receives the majority of the current state-provided dispensary services. We believe that Clicks will continue to assert its presence in the market. Although the store rollout opportunity for Dis-Chem is higher due to its smaller footprint, Clicks’ store network ranges from affluent areas to those with higher population densities, providing the group with a wider reach.

Naspers

One of the most obvious South African-listed candidates is Naspers. More than 99% of its earnings exposure is via Prosus, with less than 1% coming from Media 24, Takealot, Mr. D, Superbalist and the Naspers Foundry Venture Capital entity. Prosus does have some South African exposure via OLX and AutoTrader, PayU and a few of the EdTech companies. In aggregate, therefore, we estimate that South Africa is less than 5% of Naspers’ exposure, with Tencent, by some margin, the material driver of net asset value (NAV) and earnings fortunes.

In addition, the discount (tracking around 45% currently) is in somewhat of a self-help period, underpinned by an open-ended, NAV-accretive share buyback programme. The group has pledged breakeven/profitability, in aggregate, by its consolidated operations, and any positive trajectory in that direction over the next reporting periods, should, in my opinion, be discount supportive.

Moreover, management continues to earnestly explore a more optimal corporate structure, with Naspers, if all chips fall as we hope, the likely material beneficiary.

Assuming Tencent remains supported around current share price levels, then Naspers remains a good place to seek load-shedding investment shelter.

Remgro

Remgro is seen as a quintessential South African play, with exposure to a large number of economic sectors. Furthermore, due to its size (market cap c. R75bn) and liquidity, Remgro tends to see marginal buying and selling by foreigners, depending on how they view the “temperature” in South Africa – along with company fundamentals, of course.

We estimate that some 90% of Remgro’s earnings are South African-derived, with the remaining 10% coming from Mediclinic Switzerland and UAE and from Distell’s exports/international businesses.

Remgro is therefore highly reliant on local infrastructure for the bulk of its investee operations. For its subsidiary companies, e.g. Distell, Siqalo Foods, and RCL Foods, many measures have already been put in place to mitigate Eskom deficiencies in the form of renewable energy initiatives. For something like Mediclinic South Africa, its hospitals run off several massive generators (with the negative attendant cost of diesel/fuel). However, to our understanding, none of its investees have yet been able to get off-grid.

For this reason, we assess current Eskom/infrastructure woes as negative for Remgro. There will be elevated capex by investees as they scramble to secure electricity.

Moreover, a protracted, muted GDP growth environment also presents challenges for its investee companies.

There is some mitigation in the form of a highly diversified source of earnings/cash flows (it is not reliant on one segment). In addition, a wide net asset value (NAV) discount may provide some cushion, while pending deals (Heineken and the fibre business CIV’s transaction with Vodacom) could provide some NAV uplift.

The valuation that Vodacom placed on the CIV assets, including a direct cash contribution to current CIV shareholders, could see as much as a R4bn uplift to the value that Remgro currently places on its stake in CIV.

Reunert

Reunert is well placed to benefit from increasing alternative energy demand and government’s attempts to address the power crises. According to the Budget Review 2023, the public sector is to invest R903bn in infrastructure over the next three years. Over 78% of this will be used to expand power generation capacity, upgrade and expand the transport network, and improve sanitation and water services.

The Health Ministry will invest R350m over the next year to install power cables at about 50 government hospitals that will exempt them from load-shedding. The renewable energy opportunity is going to require additional transmission capacity and will increase demand for high-voltage power cables.

For the SA banks, renewable energy presents a significant opportunity in the form of new loans over the next four years. This will benefit Terra Firma, Reunert’s turnkey energy engineering business (the primary market is 250kw up to 30MW) and its Alternative Energy Solutions division within Nashua (addresses market below 250kw).

As a local manufacturer of high- and medium-voltage power cables, Reunert will benefit from capacity upgrades to the transmission grid. The company’s renewable energy offering comprises four elements across the ecosystem: embedded energy generation; renewable energy storage; energy control; and more recently, wheeling.

As demand for alternative energy has gone off the scale and government is increasing efforts to address the energy crises, Reunert is well placed to benefit as the dominant player in the power cables industry.

Looking ahead

In conclusion, ideally, South Africa’s growth relative to the rest of the globe recovers to the 1995-2015 mean over the next few years, but should stagnation persist, we think the above counters could thrive or at least offer a degree of protection.

*The company-specific commentary in this article was written by the analyst team at Investec Wealth & Investment SA

Investec products you may be interested in

Wealth management

Offshore investments

Investments

Wealth management

Offshore investments

Investments

Browse further in